Saving for the future is often seen as difficult, time-consuming, and a distraction from enjoying the present. It’s time to flip that idea on its head. Saving doesn’t have to be hard, and when it comes to saving for your children, there are powerful forces working in your favour that go almost entirely unnoticed.

This article looks at why saving for your child’s future is one of the simplest, most effective things you can do as a parent, and how a small amount set aside today can grow into a meaningful sum by the time they reach adulthood, giving them a genuine helping hand into the big wide world.

Where to start

A good place to begin is deciding where to save for your children. Many parents set aside a small amount from their monthly pay, say £10, £25 or £50, earmarked for their child’s future. Once this savings amount is established, the question then becomes, what should you actually do with it?

The first port of call for most parents is the Junior ISA, or JISA as it is more commonly known. This is a tax-free wrapper that allows parents to contribute up to £9,000 per tax year on behalf of their child, with any growth or interest completely free of tax. Every child can have their own JISA, and each one comes with its own separate £9,000 annual allowance.

For a monthly saving amount of, say, £25, a JISA is an excellent home for those funds. It’s also flexible in who can contribute: grandparents, aunts, uncles, or family friends can pay directly into the JISA, and their contributions count towards the same £9,000 limit, making it a natural focal point for family gifting on birthdays or at Christmas for example.

One further benefit is that the money is locked away specifically for the child. Parents act as custodians of the account, but the funds cannot be touched for anything other than the child’s benefit, and the child gains access only once they turn 18. This makes a JISA a genuinely protected, purpose-built savings vehicle, not just another pot of money that can be dipped into.

Cash or stocks and shares?

JISAs come in two forms, a Cash JISA, which pays an interest rate broadly in line with the Bank of England base rate, or a Stocks and Shares JISA, which invests the money into the market. Which to choose, and which is best for you and your child is an age-old question, and the right answer depends on several factors such as attitude to risk, capacity for loss, and time horizon, so there’s no single “correct” choice for everyone.

At Moneyfarm, we only offer a Stocks and Shares JISA. This is where the real power of the story lies. Over the longer term, stocks and shares have far greater potential for growth than cash, although past performance is not an indicator of the future. And with an investment horizon that, by definition, runs until a child’s 18th birthday, that time is exactly what a JISA has on its side. Of course, investing comes with its own risks, but having a long term timeframe for investment goes hand in hand with a Stocks and Shares approach.

The magic of compound growth

Compound interest has been described by Albert Einstein as the eighth wonder of the world, and for good reason. The principle is simple: each year, your investment grows. That growth is then reinvested, and it goes on to generate growth of its own. It’s growth on growth, and given enough time, this creates a snowball effect, where eventually the returns generated by the investment outweigh the money you originally put in.

Putting it into numbers

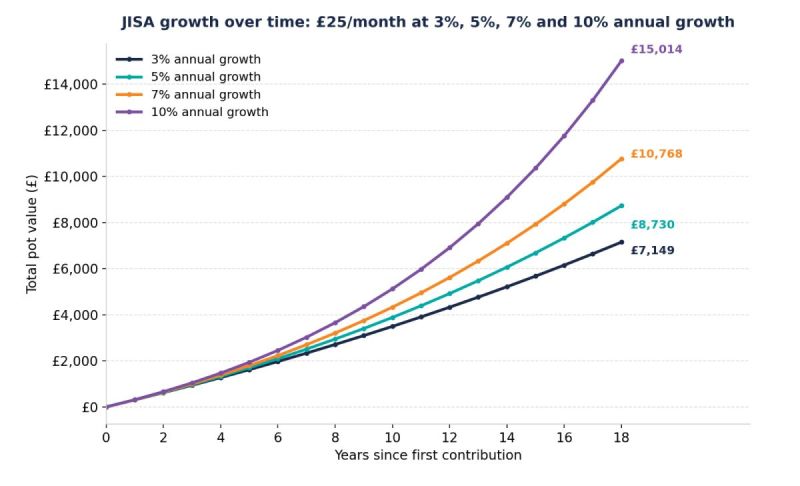

Let’s take our £25-a-month example and apply it to a newborn child. If a parent contributes £25 per month into a Stocks and Shares JISA from birth, here’s how the pot builds over time at a range of different annual growth rates, 3%, 5%, 7% and 10%:

At 3% annual growth

| Time horizon | Total contributed | Growth generated | Total pot value |

| 5 years | £1,500 | £116 | £1,616 |

| 10 years | £3,000 | £494 | £3,494 |

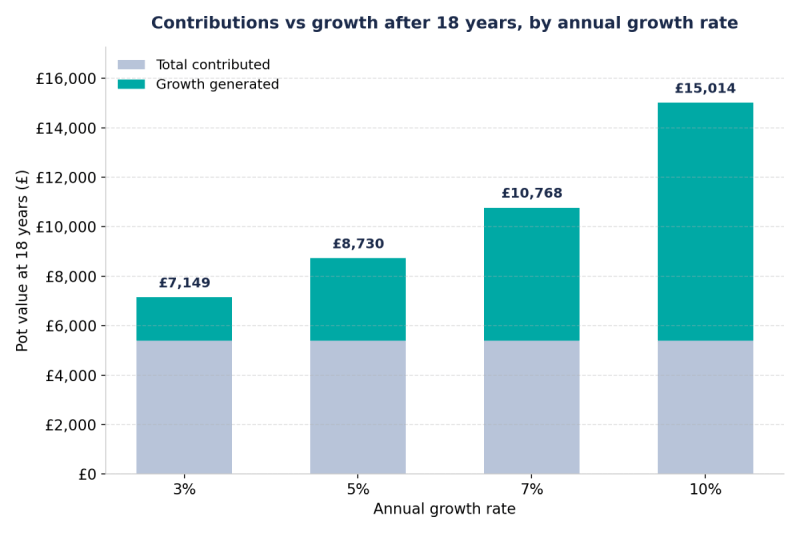

| 18 years | £5,400 | £1,749 | £7,149 |

At 5% annual growth

| Time horizon | Total contributed | Growth generated | Total pot value |

| 5 years | £1,500 | £200 | £1,700 |

| 10 years | £3,000 | £882 | £3,882 |

| 18 years | £5,400 | £3,330 | £8,730 |

At 7% annual growth

| Time horizon | Total contributed | Growth generated | Total pot value |

| 5 years | £1,500 | £290 | £1,790 |

| 10 years | £3,000 | £1,327 | £4,327 |

| 18 years | £5,400 | £5,368 | £10,768 |

At 10% annual growth

| Time horizon | Total contributed | Growth generated | Total pot value |

| 5 years | £1,500 | £436 | £1,936 |

| 10 years | £3,000 | £2,121 | £5,121 |

| 18 years | £5,400 | £9,614 | £15,014 |

The pattern across all four scenarios is the same, in the early years, the differences are barely noticeable. By year five, the gap between 3% growth (£1,616) and 10% growth (£1,936) is only around £320. But by year 18, that same gap has widened to almost £7,900, nearly the entire value of the 3% pot again. The parents have contributed exactly the same £5,400 in every scenario. The only thing that changes is the rate of growth applied to that money, and the impact of compounding over 18 years.

It’s also worth pausing on the 10% example specifically: by year 18, the growth generated (£9,614) is nearly double the amount the parents actually contributed (£5,400). At that point, compounding isn’t just supplementing the family’s saving effort, it’s doing more of the work than the saving itself.

A small difference in annual growth, sustained over a long enough period, produces an outsized difference in the end result. It’s not about predicting markets or timing them perfectly, it’s about giving your money as much time as possible to work, and staying consistent with the contributions, however big or small.

The case for starting early, and staying invested

This is what makes the JISA, paired with a long-term investment approach, such a compelling proposition. Yes, stocks and shares come with more short-term ups and downs than cash. But paired with an 18-year runway, one that’s built into the very structure of the product, short-term volatility becomes far less important than the long-term direction of travel.

The real lesson here isn’t about finding the right amount to save, or timing the market perfectly. It’s that starting early, staying consistent, and giving your money time in the market does more of the heavy lifting than almost anything else you could do. Doing less, simply setting up a regular contribution and letting compounding take its course, can, over time, lead to more.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.