We’ve recently announced that we are going to launch a 100% equity portfolio. It’s something that many clients have requested and we think that for some clients it makes a lot of sense.

In practical terms, it means that the portfolio will generally hold only equity ETFs and a small amount of cash. Historically that would have, over time, meant higher returns and higher volatility for investors when compared to a portfolio with less equities and more bonds. That’s an important point because we think a purely equity portfolio makes most sense for clients with a long time horizon and a high capacity to take risk. Why do we think that?

The chart below illustrates the point. It shows an index of global equities compared to global bonds since 1989. Equities (the lighter line) have performed far better, but there have been more ups and downs along the way. Government bonds, by contrast, have performed much more steadily, but with lower returns.

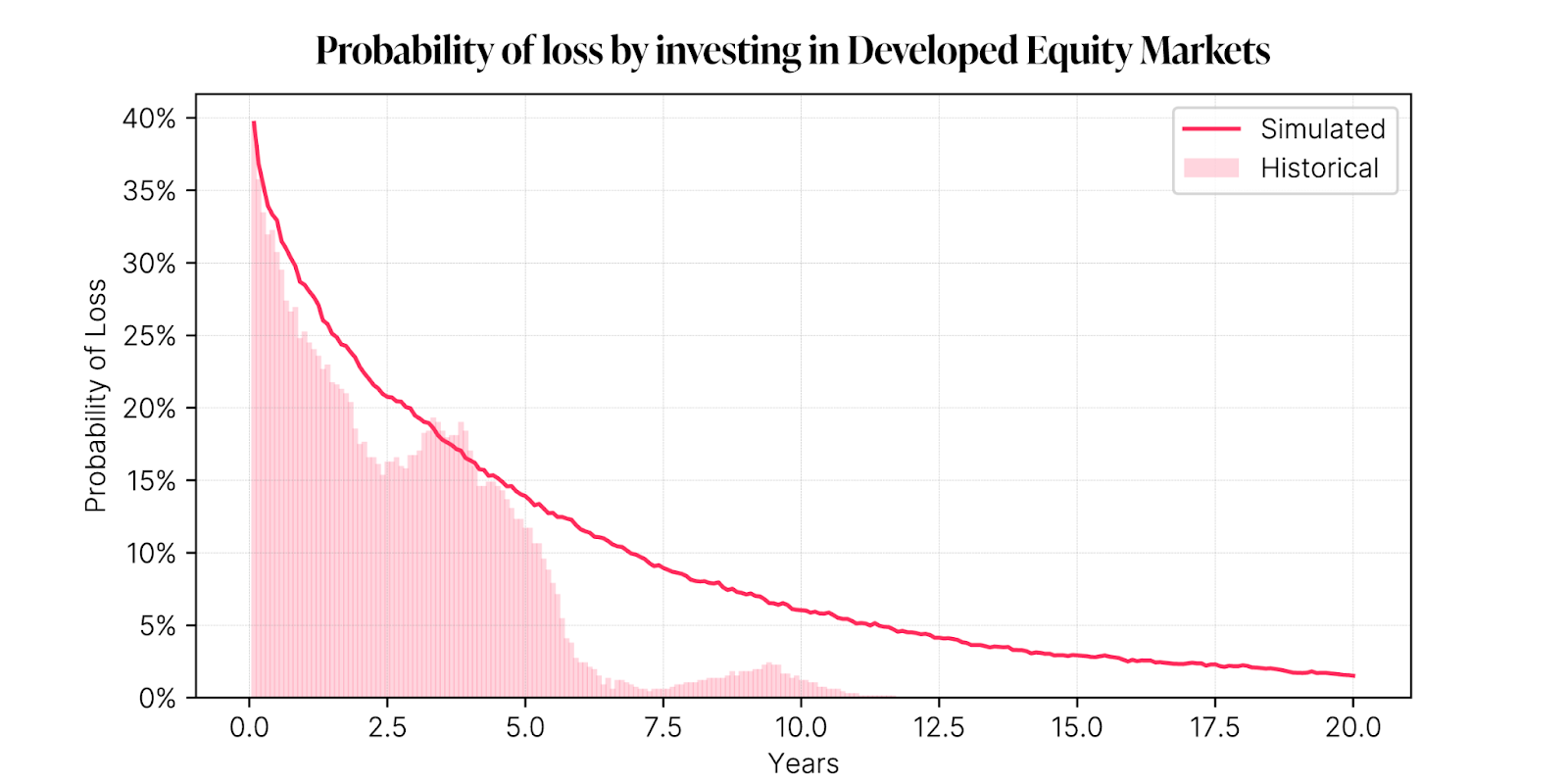

There’s another way of thinking about this. How likely are you to have lost money by investing in Developed Market equities over the past fifty years? The chart below tries to answer that. Since 1970, over most time periods you’d have likely made money investing in Developed market equities. But the probability of losing money is higher over shorter time periods, as you’d expect. But, once you have more than a ten year time horizon, that probability fell to virtually zero. However, you should note that past performance is not a reliable indicator of future results.

There are a couple of conclusions here. Stocks have been reasonably a good bet over the long term. Timing might matter in the short-term, but over a longer time horizon, it becomes less relevant.

To go a bit deeper, we ran a simulation comparing different combinations of bonds and equities. As you might expect, adding bonds to the portfolio reduces the likelihood of a loss in the simulation, and that’s more relevant over shorter or medium time periods.

Along with creating a purely equity portfolio, we’ve also taken the opportunity to review our product offering. Over the past couple of years, we’ve added a range of new products – thematic baskets and Liquidity+ to name just two. But we think it’s also important not just to add new products, but to ensure that they are all still relevant for customers. It’s been five years since we launched the risk level 7 in its current form, so it felt like a good time to review.

We’ve seen that the P6 and the P7 have performed in quite a similar fashion. The P7 has generated around 1% more per year in returns over the past five years, with slightly higher volatility. With that mind, we think it makes sense to merge the two, by moving the current P6 allocation in line with P7.

Overall, we’re excited about the changes we’re making here. We think we’re providing a great solution for customers with a long time horizon and a high capacity for risk. At the same time, we’re simplifying our offering so that customers continue to get the best portfolio for their circumstances.

What does it mean for clients?

In general we are adding a bit more equity risk to these portfolios. We’ll likely fund that by reducing our exposure to government bonds. Over time, we believe that will result in higher returns, but with some higher volatility. We believe that’s appropriate for clients with a longer time horizon.

Clients in a P7 should see their equity weight move higher from around 83% to above 95%. This will take place over some months.

Clients who choose to remain in their current P7 portfolio won’t see any change. We’ll continue to manage this line as we have done – with an equity weight that has typically been in a range from the mid-70%s to the mid-80%s.

Clients in a P6 today should see their equity weight increase by around 7%. We think that should increase the long-term returns for this portfolio, with slightly higher volatility, which is what we’ve seen when we compare P6 and P7 over the past five years.

What would the difference have been historically?

The first thing to note is that past performance is not an indicator of future performance. Crucially, we are coming from a period where interest rates have been very low and then have risen quickly – a real negative for bonds – into a world of higher and falling interest rates. So the results have to be taken with a pinch of salt.

However many people will want to know how the different portfolios will have performed over our history. First let’s look at the year by year breakdown, which takes in the positive market years, with the negative ones:

This is for the classic portfolios, before any management fees. The portfolio 7 performance is back-tested before May 2019 and the 100% equity is a back-testing of the new allocation. These figures refer to simulated past performance and past performance is not a reliable indicator of future performance.

However hopefully it gives a sense that there will be positive years and negative years. In the positive years, you would expect a higher risk portfolio to perform better – as above.

Interestingly, the negative years in this period have not shown what you expect in terms of being lower for higher risk portfolios. However, that is a function of 2 things, the interest rate environment described above – which has been negative for bonds (differently from today), but also that within the years we have seen swift falls and swift recoveries (faster for higher risk) which understates the downturns of the higher risk options somewhat.

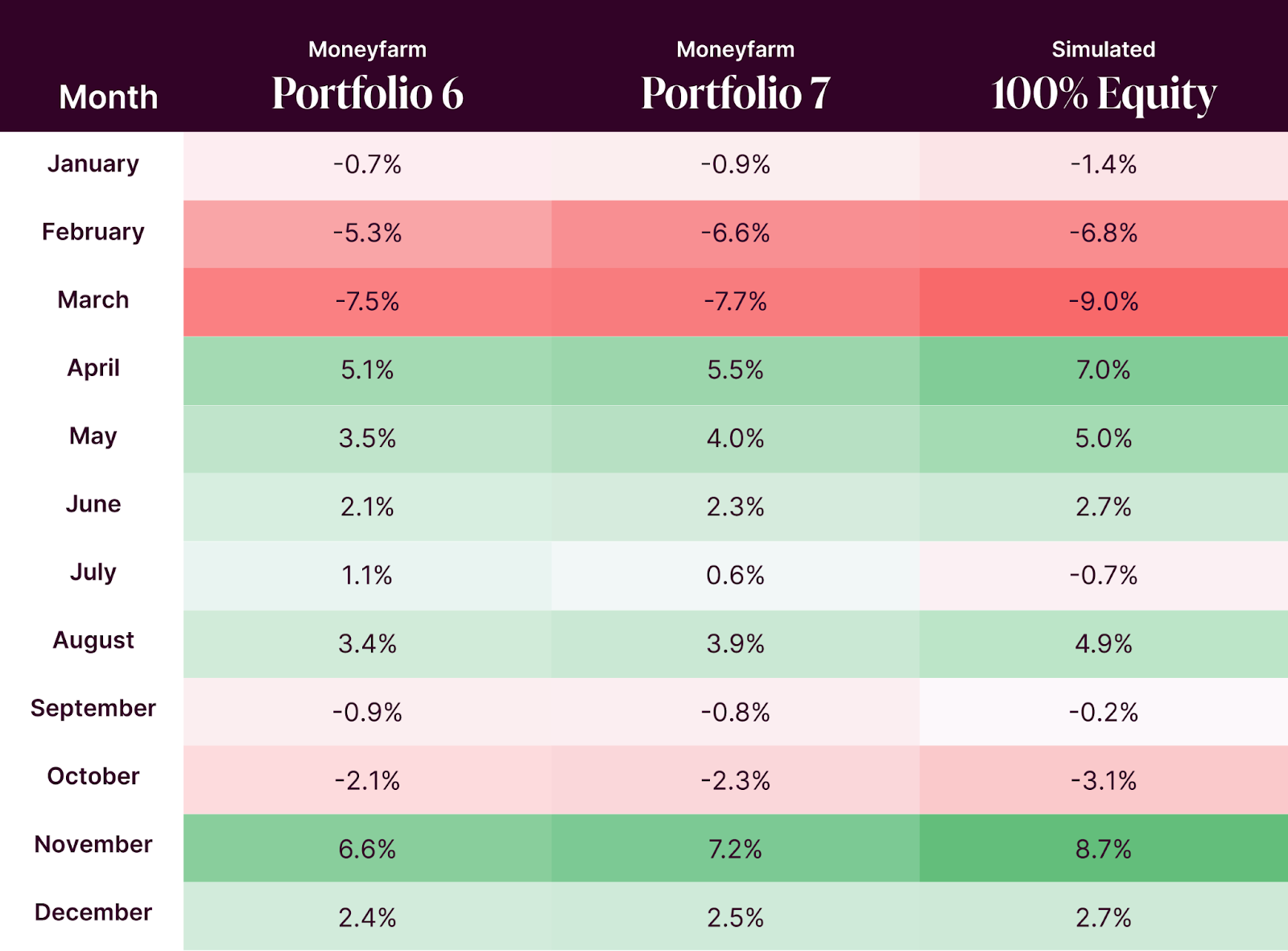

To give a sense of this, let’s look at the year of 2020, month by month, to see the effect of the increased risk:

Here we can see much more the effects of a higher volatility in the short run. In the really difficult months, you see a bigger sell off in the 100% equity vs the other portfolios, however in the recovery periods we saw a larger bounceback. This is a perfect example of our expectations.

So to summarise, we firmly believe that in the long run, the higher risk portfolios should offer a greater expected return, however this will come with some greater volatility, as shown by the 2020 intra-year sell-offs. Please bear in mind that this was an abnormally quick recovery and in the future the down-side may be more prolonged.

How will we do this?

We will use our existing level 7 portfolio to offer the 100% equity portfolio. So we will be gradually rebalancing that portfolio to add equity over the next 6 months or so.

This will allow us to manage the transition of clients going to the 100% equity portfolio in a staggered way. This should help us to mitigate the impact of short term volatility on client portfolios and ensure a smooth progression.

Clients in the current level 7 portfolio, who feel their current portfolio perfectly suits their goals and so don’t want to take part in the move, can opt-out (please see the link in the emails we have sent) and will keep their existing investments – which will now be labelled as our level 6 portfolio. This will continue to be managed in the same way as it currently is now.

Clients in our level 6 portfolio will see a marginal increase in their equity allocation to bring their portfolio in line with the current level 7 portfolio – as part of the alignment highlighted above. This should then give them a more positive outcome in the long run.

Please note, the opt out will be treated on an account level. So if you have more than one level 7 portfolio and would like to make a different decision with each – please speak to us.

It’s also important to state that there will be no changes in the fee structure and there will be no trading fees incurred for clients.

When will this happen?

We first announced this move on the 7th of October and we will give clients 30 days in order to opt out of the shift. Then from that point onwards we will begin to adjust the portfolios.

Further details on how to remain in the current allocation are available in the email received on that date. Alternatively, please contact us if you would like to opt out, or you can also reach us by calling 0800 433 4574.

We won’t stick to a strict schedule, or necessarily start on day 1 for that matter, but the transition will be managed as and when the portfolio management team sees fit.

This could be as a process of lots of small and regular increases (pound cost averaging) or if we see a drop in markets, we may capitalise to add more, should we deem it prudent.

We believe the process will take up to 6 months to reach 100% equity, however this will depend on market conditions.

Ensuring the best transition for our clients is vitally important to us.

Please note, any new portfolios created from the 7th of October will have the new allocations already in place.

Why now?

We have seen strong equity market performance over the last couple of years and there are some questions about the effect that the upcoming US election will have on markets and US economic growth in general, so this may lead some people to question the timing.

The first, and actually less relevant point, is that we still have a reasonably positive outlook for the medium term. With interest rates coming down, if the global economy can avoid recession this should be a positive combination for global equity markets. If this isn’t the case, our team will still tactically manage the portfolios as we always have done to manage these situations.

However the key reason is that, simply, these portfolios are appropriate for those with a long time horizon and as the charts in the first section show, market timing matters less in the long run.

So if the next equity market sell off is in 3 months or 3 years, it doesn’t matter. What is more important is that our clients are in the right asset allocation for their needs. For those with the appropriate risk level and, say, 20 years left on their pension portfolio, we believe there is no time like the present to get them into a portfolio that can maximise their long term potential.

We will still make sure we do everything that we can to make this a smooth experience in the short term though. However, if you would like to switch your portfolio straight away, please speak to us.

Speak to us

We understand that is no small change, particularly for our clients with level 7 portfolios. If you would like to understand more about what this would mean for you, or you would like to know more about the exciting opportunities of a new 100% equity portfolio – please speak to our friendly team. We would be more than happy to take the time to help you make the decisions that are best for your future.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.