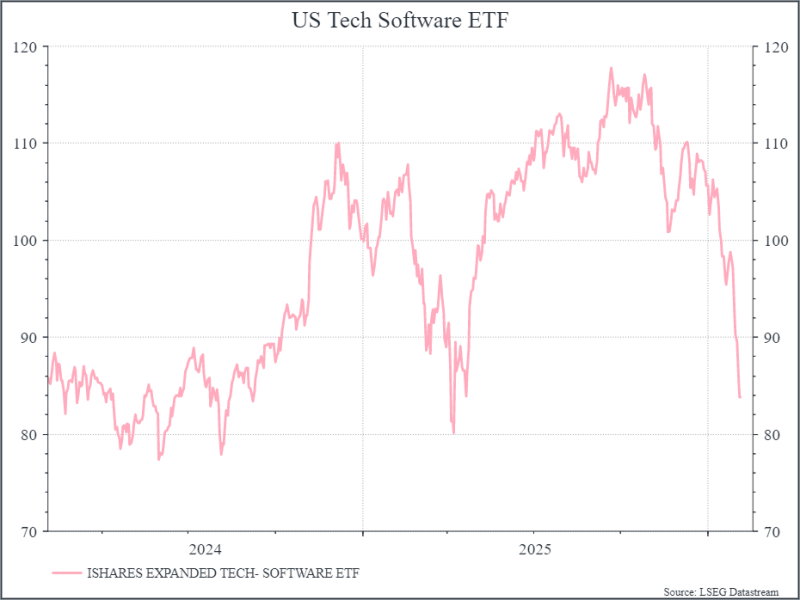

Last week Anthropic, the Artificial Intelligence (AI) business, released a range of tools for its Claude Cowork platform that, among other things, can automate legal services. This prompted a sharp sell-off across a range of software businesses (so-called Software-as-a-Service, or SaaS), as investors feared significant potential disruption in those businesses. The chart below shows the progression of an ETF made up of these types of companies.

This ongoing incident highlights the potential disruption across industries, as AI businesses continue to innovate at a rapid rate. We wanted to explore some of that in a bit more detail.

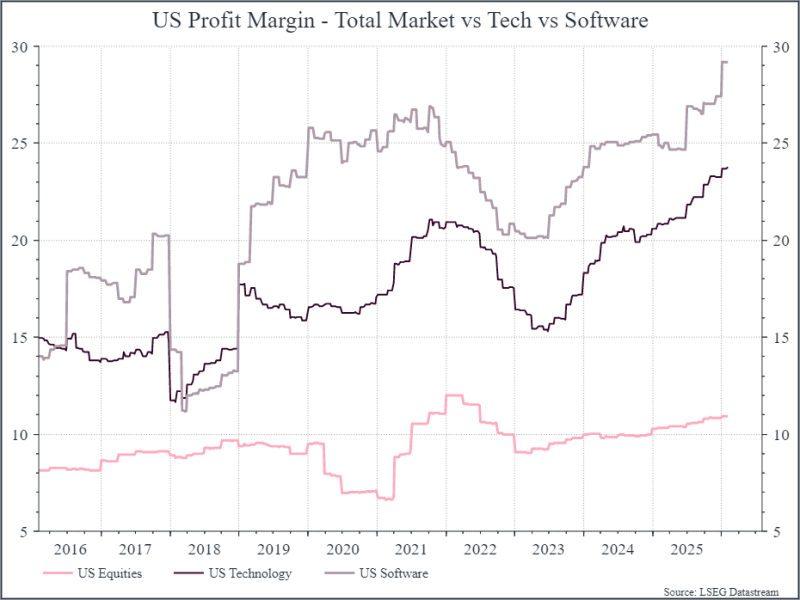

First, it’s worth pointing out that US software businesses have been a good place to be in recent years. The chart below shows the net margins for US software, US tech and the overall US market. We can see that profitability in US software businesses has risen steadily over the past three years and exceeded even the overall tech universe. Both are well ahead of the overall US market (the bottom line). Looking at those margins and you might guess that software is a sector ripe for disruption.

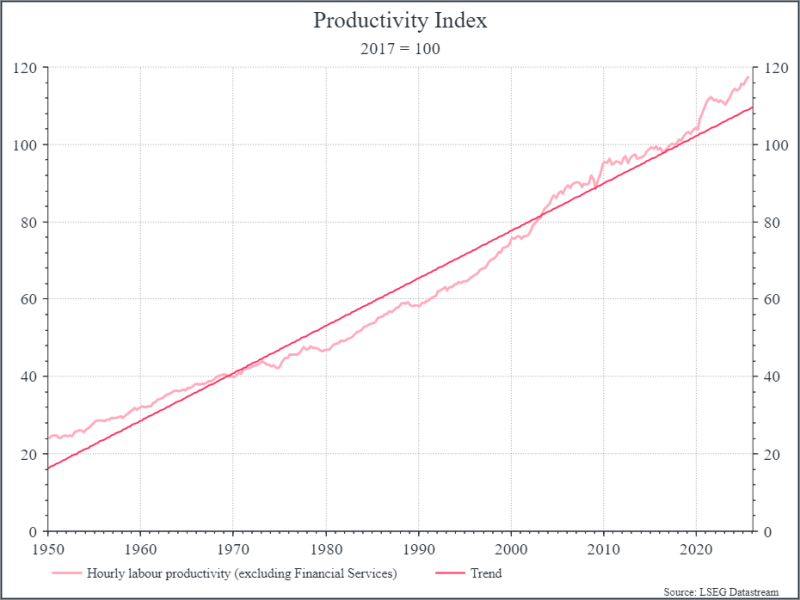

Second, we think it’s important to stay focused on the macro potential of AI – specifically the possibility of sustainably stronger productivity growth. We think there are signs that this is underway. The chart below shows hourly labour productivity over time, along with the long-term trend line. We think the chart shows a couple of distinct periods – first, a period of relative stagnation from the early 1970s to the mid 1990s; second, a pick-up from the early 2000s that seems to be gaining momentum in recent years. If you’re a tech optimist, you’d argue that this second period coincides neatly both with the internet adoption and the incipient AI expansion.

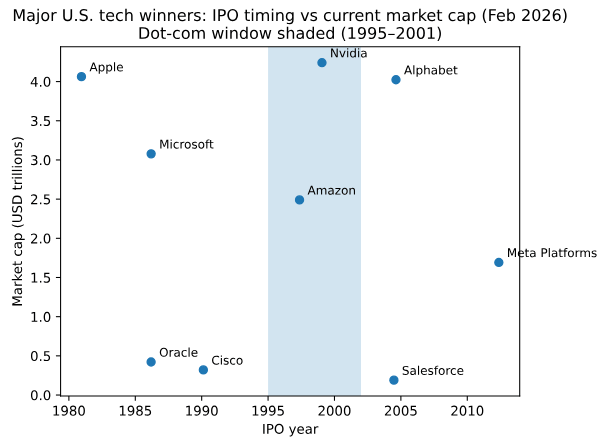

Moreover, we should remember that it’s tough to identify the likely winners and losers in AI. The chart below considers some of the biggest tech companies and looks at when they IPOed. The period of greatest hype didn’t generate the most winners. Of all the companies that listed during the dot-com boom (and there were hundreds), only Amazon and Nvidia have really come to dominate in their categories. And you could argue that Nvidia wasn’t really part of the internet hype. Apple, Microsoft and Oracle predated the internet boom, while Google, Meta and Salesforce came later. The biggest winners from the current AI enthusiasm may not yet have been founded or listed.

Finally, with all the focus on AI investment, perhaps the real winners won’t be in tech at all but actually their customers, who may find themselves able to build tools far more easily and cheaply than they could before. You’d guess that the tech infrastructure providers are working hard to ensure that they are gatekeepers in this new ecosystem, but there’ll likely be some losers along the way. The recent volatility in SAAS stocks doesn’t mean that moment has arrived, but it’s something we should certainly focus on.

What does it mean for portfolios?

If AI really delivers on even some of its promise, we can see the potential for higher productivity and sustainably stronger economic growth (if they can solve some of their environmental challenges). That could bode well for businesses across the world.

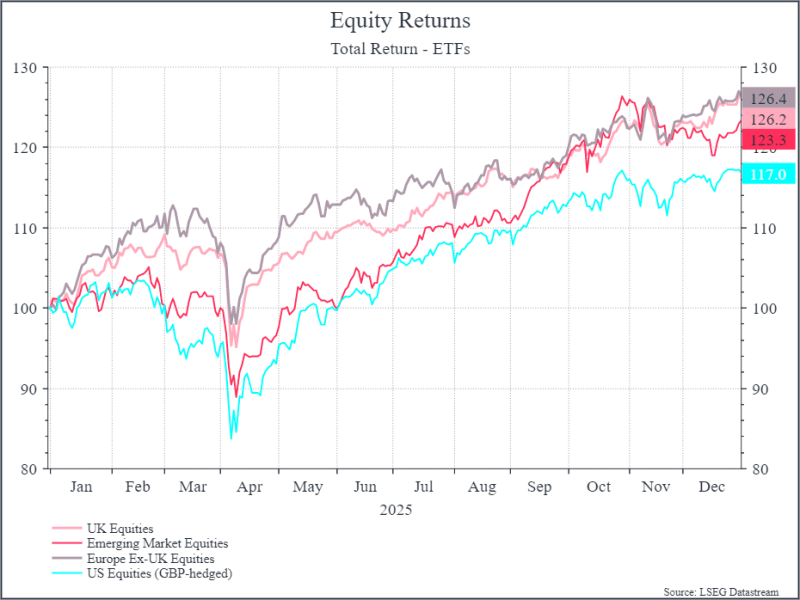

At the same time, the past week raises the question of winners and losers. Will tech effectively eat itself – providing both the biggest winners and losers from AI? Does faster global growth argue for greater diversification, as AI investments help their customers become more efficient. As the chart below shows, 2025 saw non-US equities outperform the US (even considering the currency), even as AI dominated the investment debate.

If global businesses really begin to harness AI, we think this could potentially continue in 2026. The case for global diversification still looks strong. The case for global diversification still looks strong. This principle underpins our approach at Moneyfarm: constructing diversified portfolios across geographies and asset classes, designed to adapt to structural market shifts. In an environment where innovation and volatility often coexist, diversification remains the most effective way to pursue long-term growth with consistency and discipline.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.