It’s been a noisy time in financial markets, between the US elections, central bank decisions and ongoing geopolitical turmoil. But we wanted to take a step back and look at how companies are performing in some of our key markets.

First, let’s start with the US, where most listed companies have now reported their third quarter earnings. According to Factset, earnings for the S&P 500 grew around 5.4% in the three months to September compared to the same period last year. Around 75% of companies reported better earnings than analysts had expected and 61% reported better than expected revenues. That sounds pretty solid, although the average percentage of companies that “beat” expectations over the past five years has been higher than that.

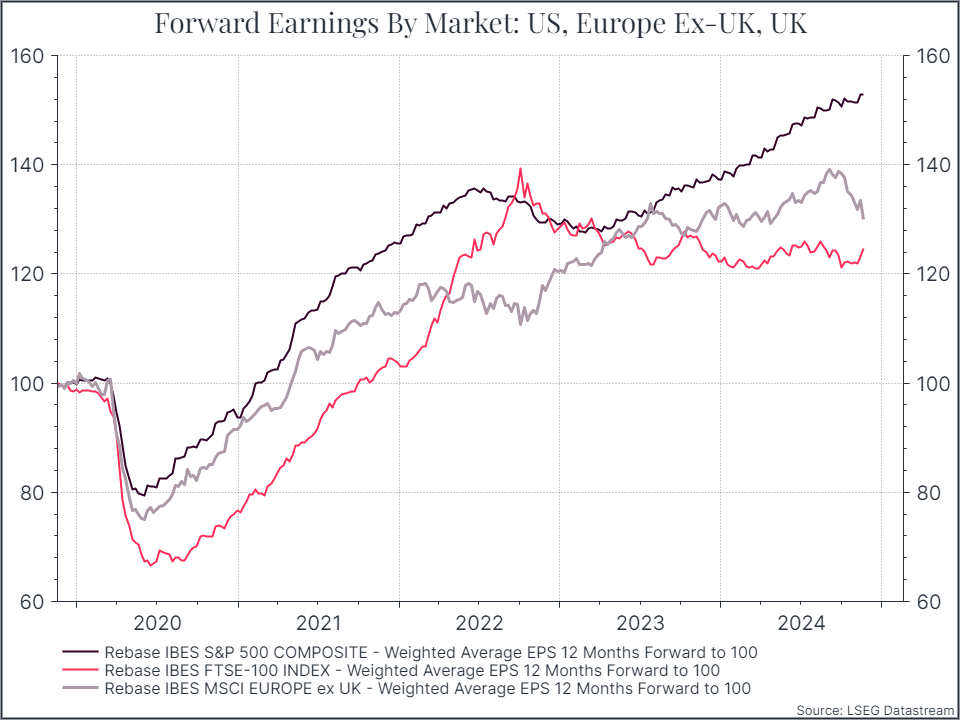

Let’s compare the US with what we see in the UK and Europe (excluding the UK). The chart below shows forward earnings estimates over the past five years. It shows steady progress in the US, relatively little movement in the UK and a deterioration in Europe.

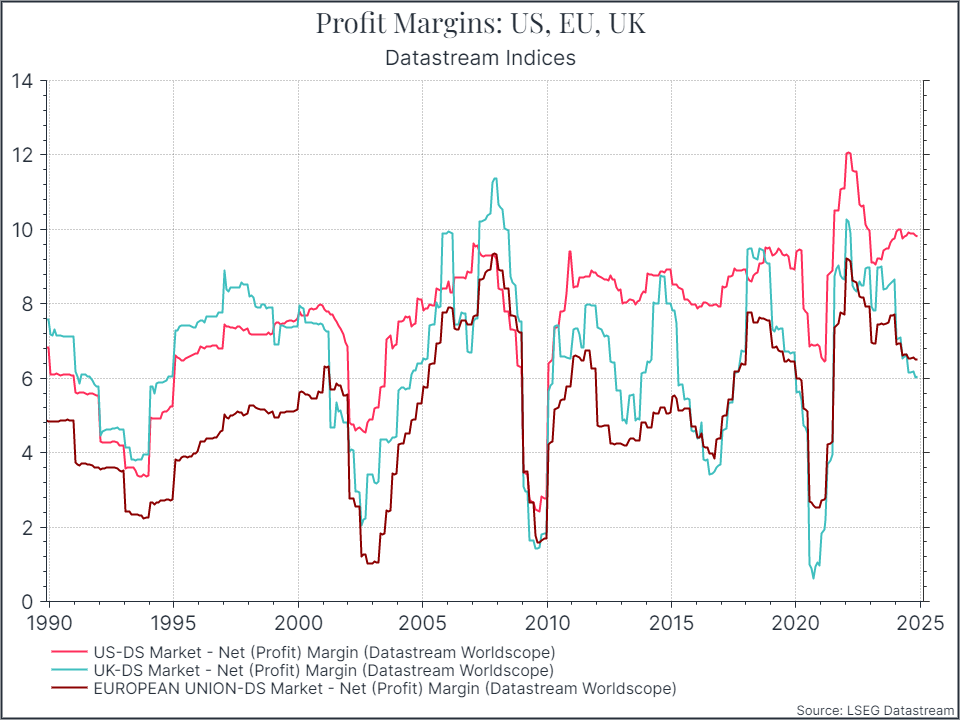

Corporate profit margins explain a lot of the difference. The chart below shows net margins over time for the US, the EU and the UK. There are a few points to note. First, margins are generally cyclical, when there’s a recession (see 2008-2009 or 2020) margins fall – which is what you’d expect. Second, as we’ve noted before, US margins in aggregate have generally drifted higher over the past thirty years. Margins in Europe however, haven’t really shown much of a secular improvement. Third, looking at the recent past, we can see that US corporate profitability has held up pretty well recently, while margins in the EU and the UK have come under pressure. We think that some of that is a function of stronger growth in the US supporting margins there and pressure on the auto sector in Europe, which is a relevant part of European profits.

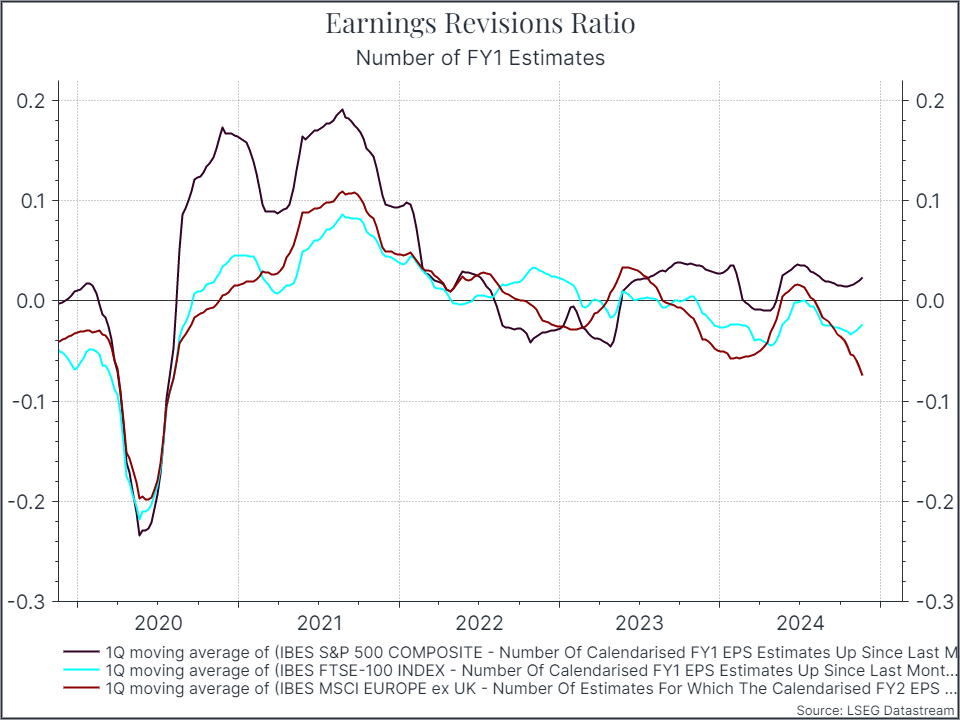

Thinking about earnings forecasts, the chart below shows how analyst expectations have changed for this year (or what’s left of it). We’ll only see how accurate these estimates are towards the end of February. Earnings expectations in the US have held up fairly well, while we’ve seen quite a few analysts downgrading their forecasts for European earnings.

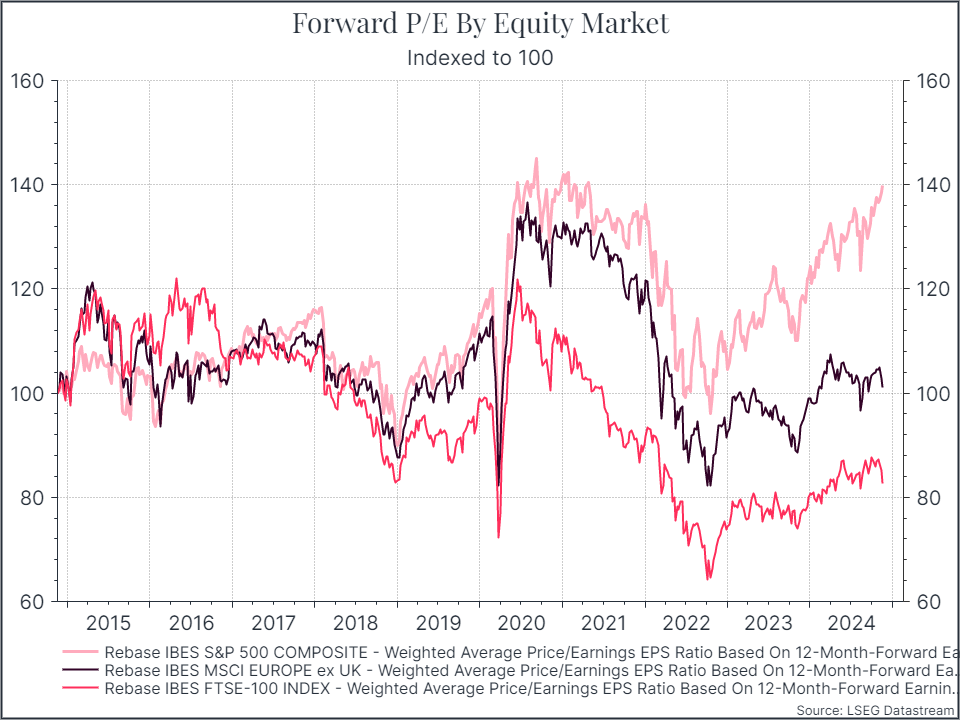

Finally, a word on valuations. The chart below shows the path of the forward price/earnings ratio, a standard valuation measure, for the US, Europe and the UK. We can see the steady rise in US valuations over the past couple of years, especially relative to Europe and the UK. A lot of that reflects the impact of the large tech companies listed in the US, and the expectations for an AI-related boom. The combination of rising valuations and stronger earnings have helped drive the outperformance of US equities.

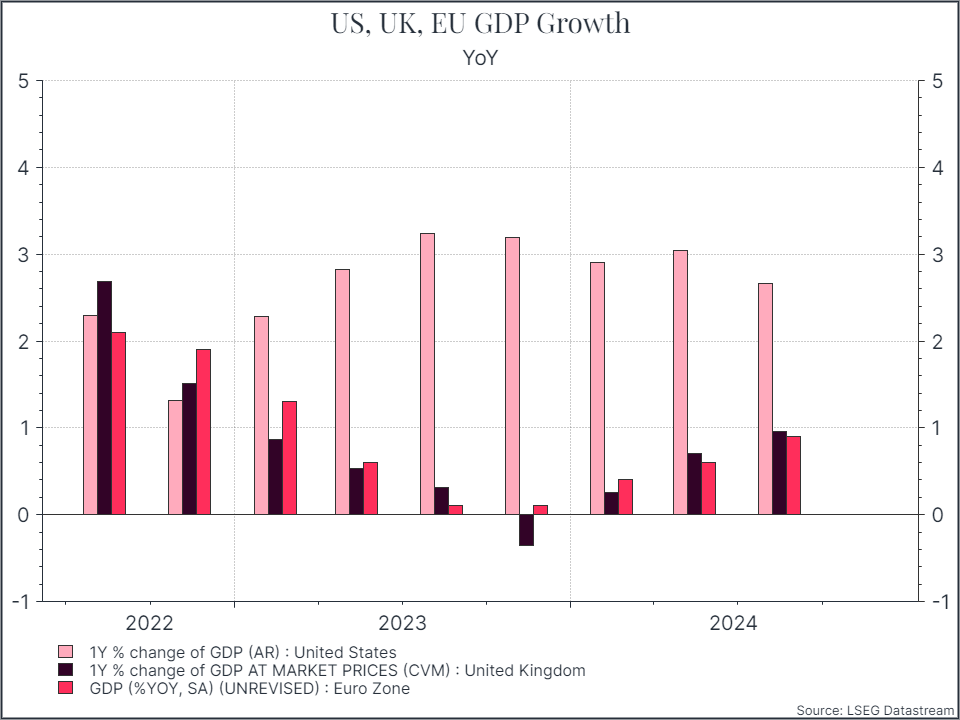

Where does this get us? We can see the divergence in the performance of European and US businesses. US margins have held up pretty well, while we’ve seen corporate profitability come under some pressure in Europe. We think some of that reflects the difference in economic growth, as the chart below illustrates.

Analysts seem to be downgrading their forecasts for European companies at a faster pace than in the US.

But, as we’ve seen for a while, US equity valuations are some way higher than their European peers. That would still be true (although less pronounced) if we adjusted for the much larger weight of technology companies in the US.

So, it’s a familiar dilemma. Do you buy the businesses that are performing well but are more highly priced? Or do you focus on the value alternatives – cheaper businesses that are facing tougher times operationally? In general, we’ve been biassed towards the former, holding a meaningful exposure to US equities. And while we’re mindful of all the uncertainties in the world, positive and negative, we still think that’s a decent place to be.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.