Last week the Bank of England (BoE) cut its policy rate by 25 bps – from 4.75% to 4.5% – in a move that was widely anticipated.

At the same time, it released its quarterly monetary policy report, which provided some insight into how UK central bankers view the economy.

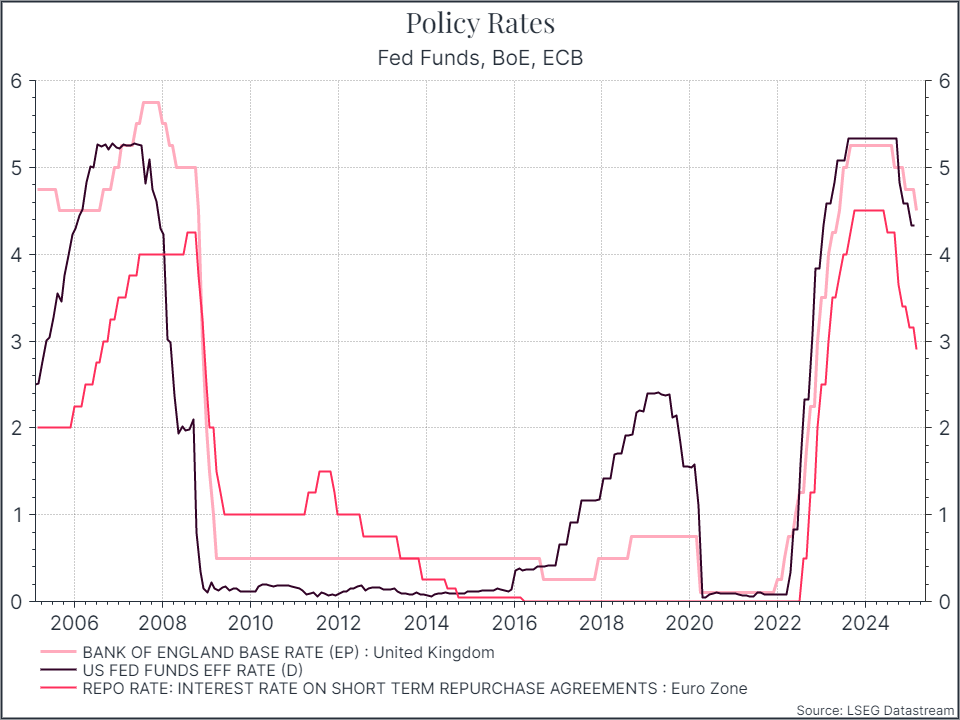

In terms of policy rates, the UK is following a similar downward trend to the US and the Eurozone, as you can see in the chart below.

UK and US policy rates are moving closely, while the European Central Bank (Ecb) has moved a bit faster.

At the same time, growth in the UK is lagging behind the US, even if the gap has actually begun to close a bit.

That brings us to the Bank’s latest monetary policy report. The report highlighted some familiar challenges, for households and policymakers.

It’s usually helpful to look at how the Bank’s forecasts have changed over time. And here the message was pretty downbeat: for 2025 and 2026, the Banks economists expect lower growth, higher inflation and higher unemployment than they did in their last report in November. The Bank also noted weakening business confidence, a result of tax changes and global uncertainty.

It doesn’t bode well for the government accounts. We’ll see the latest official forecasts from the Office of Budget Responsibility next month, but it’s likely that the Chancellor will have, at best, less headroom than she expected a few months ago.

At the same time, there is some cause for optimism. Inflation does look fairly well-contained for now, albeit above where the Bank would like it to be. Annual GDP growth, as reflected in the chart above, has been picking up, albeit against a low base. And, while forecasts for unemployment may have moved up, the labour market still looks in decent shape.

What does it mean for portfolios? There are a few points to make here.

First, our portfolios remain globally diversified with a wide range of exposures in both fixed income and equities.

Second, a lot of what we’ve described is well understood and should be reflected in financial asset prices.

UK government bond yields are relatively high versus history and, in our view, can generate useful income in the coming quarters.

UK equities look attractively valued versus their history and also provide a lot of global exposure, rather than just being focused on the UK domestic economy.

There are clear challenges but, with relatively attractive starting valuations, we think there’s merit in maintaining some UK exposure.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.