With the strong performance of equity markets over the past six months, the tariff announcements from early April aren’t quite as big a focus for investors as they were. But that doesn’t mean the economic impact has gone away. We can already see shifts in the dynamics of global trade, and that’s likely to continue.

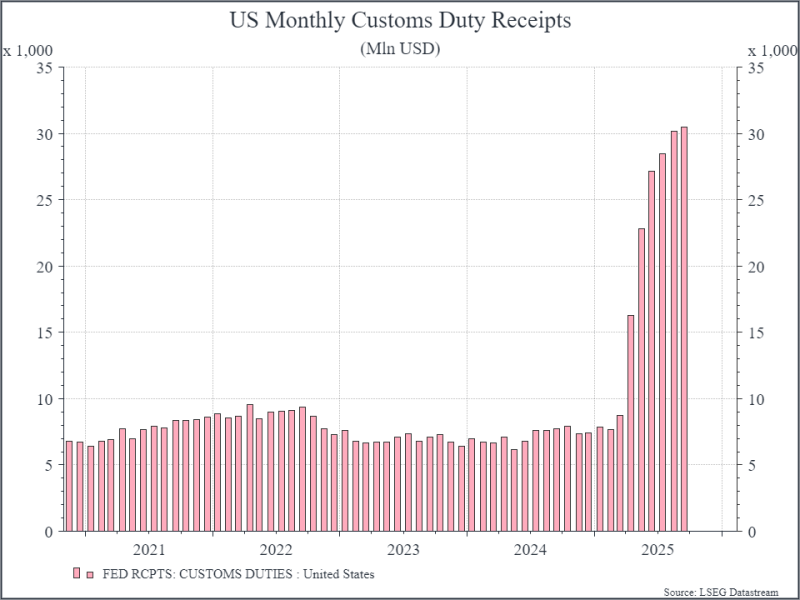

Even if the headlines have moved on, it’s worth remembering that there has been a significant shift in US tariffs. In 2022, for instance, the blended US import tariff was estimated at around 1.5%. Today, the estimate is around 17%. We can see the practical impact of this in US customs data.

The chart below shows monthly customs duties paid on goods imported into the US: these are now running at around US$30 billion per month. You can debate who is really paying for it – is the exporter cutting their prices? Is it the importer taking the hit? Or is it the final consumer paying higher prices? Those are important questions, but it’s clear that someone, most likely the importer, is paying today.

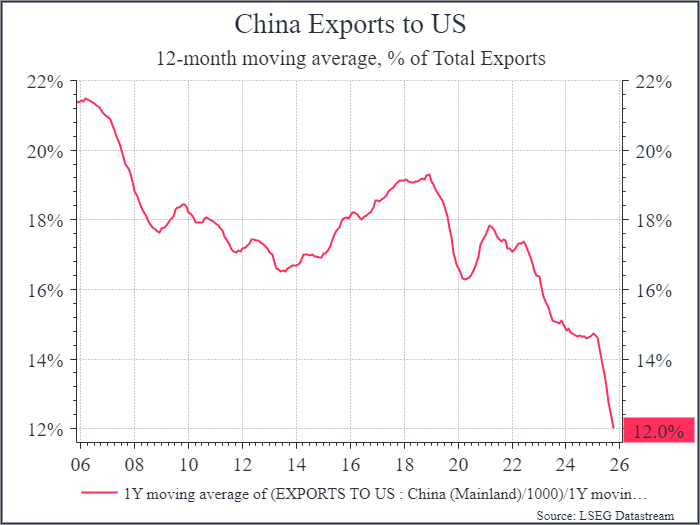

You’d expect that US trade barriers would cause a shift in behaviour, and we’re already seeing that in the numbers. The chart below shows Chinese exports to the US as a percentage of total Chinese exports.

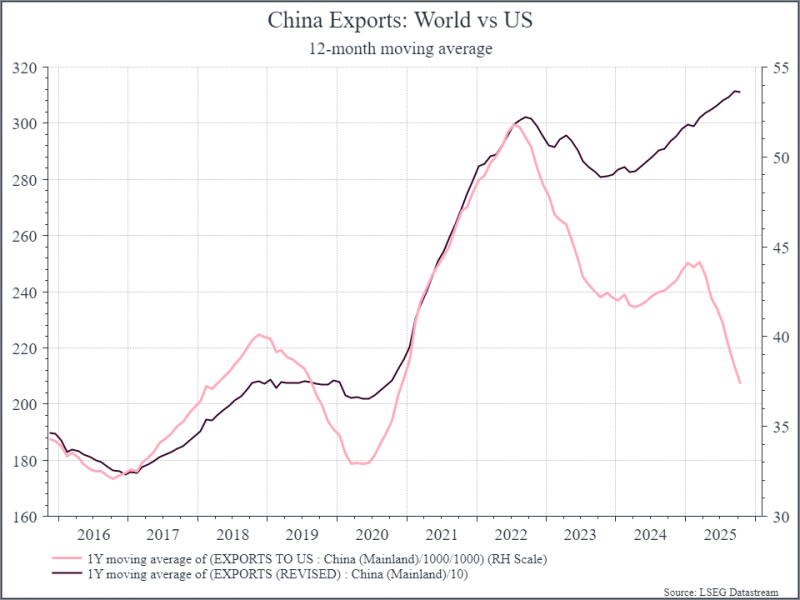

Digging into that a bit more, we can see an interesting trend. The chart below breaks out total Chinese exports (12-month moving average) compared to exports to the US. Overall, Chinese exports have continued to expand, (although the latest data for October was slightly negative year-on-year), even as exports to the US have fallen. Chinese companies have found other markets to fill the gap – and increasingly that’s other Emerging Markets.

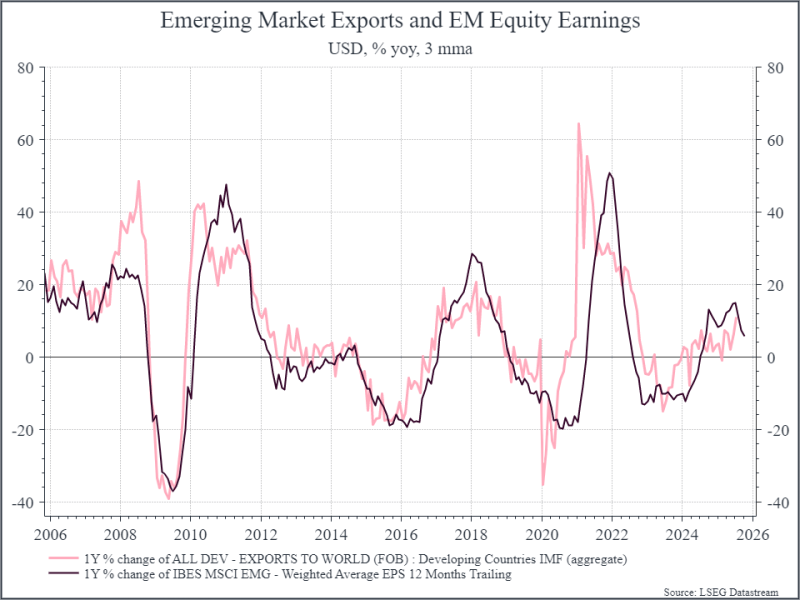

We care about this for a few reasons. First, we generally think that trade should help drive global growth, even if there will be winners and losers below the headline level. Second, we think export growth in Emerging Markets has been correlated with earnings growth for EM equities (see chart below EM export growth vs EM earnings growth), and China is an important part of that. Higher tariffs could stifle export growth in EM going forward, but so far, it seems that EM corporates have held up ok.

Where does this get us? Tariffs may be less of a headline focus, but they haven’t gone away. The long-term implications for growth and inflation are still to emerge particularly in the US, where AI spending has really helped to support growth.

We are beginning to see a rewiring of global trade linkages, notably between China and the US. And that’s something that will take years, rather than months, to feed through and it’s tough to say ultimately who wins and loses. So far, Emerging Markets in aggregate seem to have held up, whereas perhaps Europe – think European autos – may have struggled a little more.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.