The notion of American exceptionalism is deeply ingrained in US culture. It traces back to the writings of Alexis de Tocqueville, the French political scientist and historian who, after traveling through the United States in 1831, described the nation as “exceptional”. His reflections focused largely on America’s unique social fabric, democratic ideals, and political institutions, which set it apart from Europe at the time.

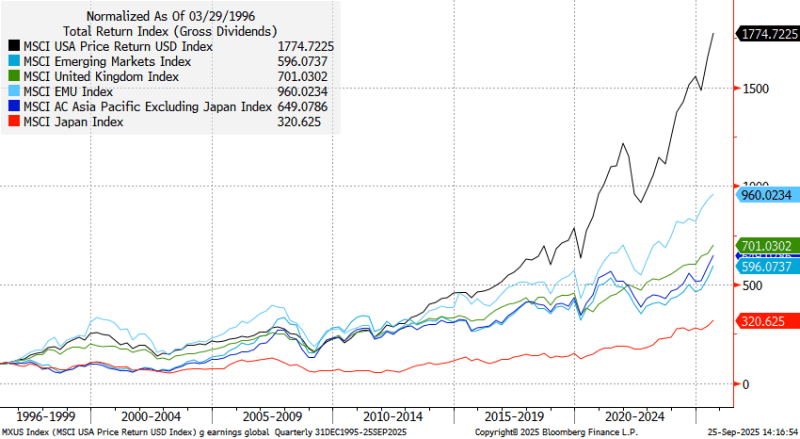

In recent years, the term has increasingly been applied beyond culture and politics – extending into financial markets. For investors, the past decade and a half has been a rewarding period for US equities. As the chart below illustrates, American stocks began to pull ahead decisively in the years following 2016–2017, leaving other major global equity indices trailing behind, although this can’t be relied upon for future performances.

Despite repeated calls for an imminent reversal from seasoned analysts and investors, the US equity market has continued to defy expectations. Supremacy has not only endured, it has strengthened, leaving market observers searching for explanations.

Just as America’s cultural exceptionalism is rooted in a unique set of social and institutional characteristics, the exceptional performance of US equities reflects a distinct combination of economic and corporate strengths. These factors have consistently delivered superior results for investors and help explain why the US market has increasingly “decoupled” from its global peers.

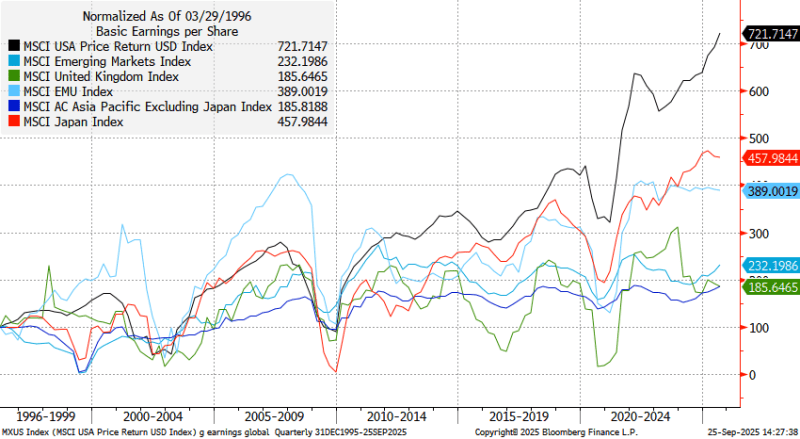

As the chart below illustrates, historically earnings growth in the US has significantly outpaced that of other major economies, reinforcing the market’s long-term leadership and resilience.

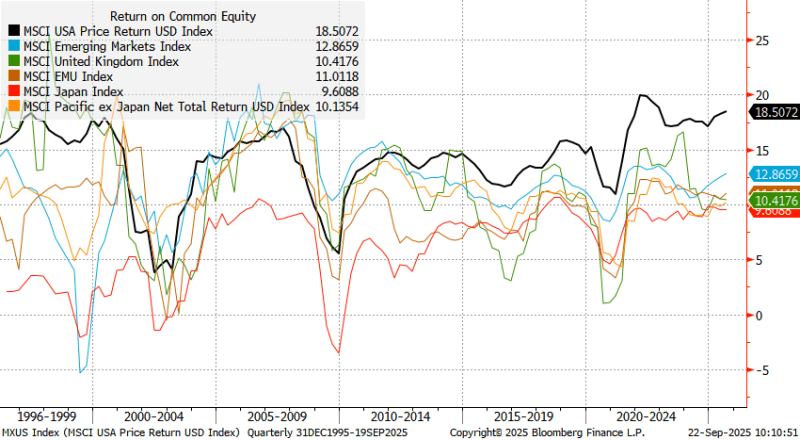

Another way to understand the exceptionalism of US equities is through the lens of Return on Equity (ROE). ROE measures how efficiently companies generate profits from the capital invested by shareholders. In other words, it reflects the ability of corporate management to deploy resources in a way that maximizes shareholder value.

As the chart below shows, US companies have consistently delivered higher ROE than their global peers – with a notable acceleration after 2015. This step-change underscored the superior profitability and efficiency of US corporates, particularly in sectors such as technology and healthcare that dominate US equity indices.

Why does this matter for investors? A sustainably high ROE is more than just a reflection of past performance, it is often an indicator of enduring competitive advantage. Companies with higher ROE typically have stronger business models, better pricing power, and more efficient capital allocation. For equity investors, this translates into more resilient earnings and, ultimately, stronger long-term returns.

This structural profitability edge has been a critical driver of US equities’ long-standing outperformance and remains a cornerstone of their investment appeal today.

Although not an indicator of future returns, US companies have consistently proven more profitable than their international counterparts, sustaining higher net profit margins over time. This profitability has translated into stronger earnings performance, a key driver of US equities’ superior returns. Nowhere is this more evident than in the technology sector, where today’s leading firms regularly achieve margins of around 20% – far surpassing the 5–10% levels seen during the dot-com era.

A more dynamic economic engine

The US economy benefits from several structural advantages that reinforce its exceptional performance:

- Productivity – US productivity growth has outpaced that of other G7 nations and is expected to maintain this lead, supporting durable economic strength.

- Demographics – Unlike Western Europe and Japan, the US enjoys more favorable demographic trends, with a working-age population that is still expanding.

- Growth – Forecasts for US economic growth remain comfortably ahead of most developed market peers, providing a supportive backdrop for corporate earnings.

The composition of the US equity market further distinguishes it. A small group of dominant technology leaders, often referred to as the “Magnificent Seven” (Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia e Tesla), has driven a disproportionate share of performance in recent years. These companies combine exceptional profitability with strong balance sheets and substantial cash reserves, giving them both resilience and market power. As a result, the US market today is more concentrated in high-quality, high-growth businesses than either its own past or most other global indices.

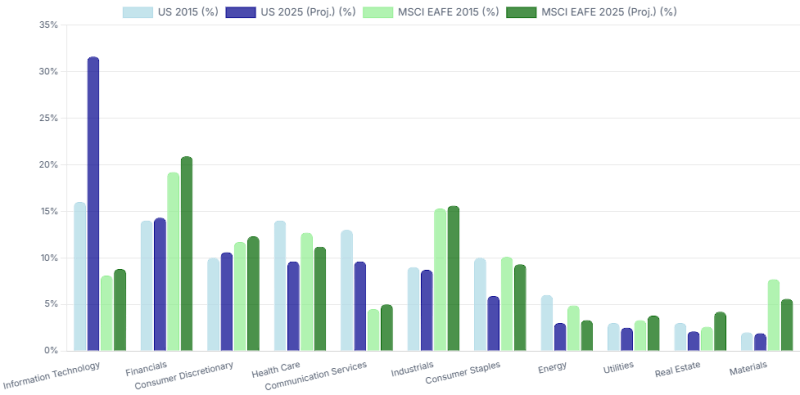

This dramatic shift in its sector composition has been the fundamental driver of US equity market supremacy over the past two decades. Historically, the US market was heavily weighted toward more cyclical sectors whose fortunes tend to rise and fall with the overall economy, such as energy, industrials, and financials. Today, it is dominated by higher-margin, innovation-driven industries – particularly technology, communication services, and healthcare. The chart below tracks how sector weights have shifted over the past decade in US stocks and the MSCI EAFE index (covering large- and mid-cap stocks across 21 developed markets).

This pivot has been transformative. Technology and digital platforms are not only structurally more profitable but also enjoy secular growth tailwinds that extend well beyond traditional economic cycles. As these sectors grew to represent an outsized share of US indices, they elevated the overall profitability, growth profile, and resilience of the market itself.

By contrast, many international equity markets remain more concentrated in lower-growth, capital-intensive industries, limiting their ability to match the US in terms of earnings power and shareholder returns. The US sector evolution has therefore been a critical foundation of its long-term outperformance.

The outcome of these structural advantages is visible in today’s global equity landscape. US equities now account for more than 60% of total developed market capitalization – a level not seen in modern history. This dominance reflects not just the scale of the US economy, but also the exceptional profitability, growth, and resilience of its corporate sector.

While the rest of the world continues to offer important diversification opportunities, the sheer weight and influence of the US market underscore its central role in global portfolios. For investors, American exceptionalism is not just a historical notion – it is a present reality in financial markets.

US shares: why now?

The US market’s recent narrative has been dominated by a small handful of transformative companies. Although not without its risks, the performance of the “Magnificent Seven” has been so extraordinary – posting a 71% gain in 2023 – that without them, the S&P 500 (the stock market index tracking the performance of 500 leading companies listed on stock exchanges in the United States) would have had a return of mere 6% instead of 25.9%.

These seven firms now account for around one-third of the entire S&P 500 market capitalization, a level of concentration roughly double that seen during the dot-com peak, and they are just one click away. The Magnificent Seven are immensely profitable, with profit margins around 20% (compared to 5-10% for IT firms in the late 1990s), vast cash reserves, and formidable barriers to entry that protect their market power. For investors seeking exposure to the most powerful themes of our time, these companies are indispensable.

Yet, for the disciplined “Warren Buffett” archetype, the US market offers equally compelling opportunities beyond the mega-cap tech darlings. The intense focus on the Magnificent Seven has created significant valuation disparities.

Finally, if you know better, understand the risks and have done your homework properly, small-cap stocks now trade at a historic discount to their large-cap counterparts. These smaller, domestically-focused firms are even more geared to benefit from the strength of the US economy than the large-cap multinationals. For value-oriented investors, this presents a fertile ground for uncovering quality businesses at attractive prices, far from the froth of the market leaders.

The true strength of the US market today is this very breadth: the ability to pivot from disruptive innovation to durable value, all within one ecosystem.

Invest in US shares with Moneyfarm

Ready to tap the US market? US equities can offer exposure to some of the world’s most innovative companies, while also coming with risks such as higher valuations, potential volatility and sensitivity to economic or political events.

With Moneyfarm DIY Investing you can do it via your Stocks & Shares ISA or GIA – simple pricing, integrated analytics, hassle-free tax admin (we handle the W-8BEN; inside an ISA your returns are tax-free), transparent GBP↔USD conversion, and everything in one place (shares, ETFs and managed funds). Or go curated with our Special Collections – Tech Titans, The AI Revolution, California Dreaming, Electric Mobility, and Latest IPOs – designed and monitored by our Asset Allocation team to help you explore opportunities with confidence. But remember that themed investments are more concentrated and may carry higher risk than a diversified portfolio.

Important Information: The value of investments can go down as well as up, and you may get back less than you invest. Past performance is not a reliable indicator of future results. Thematic investments (such as technology or AI-focused portfolios) may be more volatile and concentrated than a diversified portfolio. Returns from US investments may be affected by currency fluctuations. Nothing in this article should be taken as investment advice or a personal recommendation. Any views expressed are for information only and may change without notice. Tax treatment depends on your individual circumstances and may change in future. If you are unsure about the suitability of an investment, please seek independent financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.