The S&P 500 reached a new all-time high this week (at least in dollar terms), and markets are looking far more resilient than many feared in the immediate aftermath of Liberation Day. It feels like the right moment to take stock of where we stand.

First, as we’ve noted before, the recovery from the recent lows in early April has been very swift, with the S&P 500 rallying around 25%. At least some of the move reflects de-escalation on trade policy. Investors seem optimistic that we’ll avoid the worst case scenarios for tariffs. We may not get a clear resolution by 9 July – the end of the 90-day pause on certain tariffs announced by President Trump – but we think there’ll be enough progress on negotiations between the US and most of its trading partners for the pause to be extended.

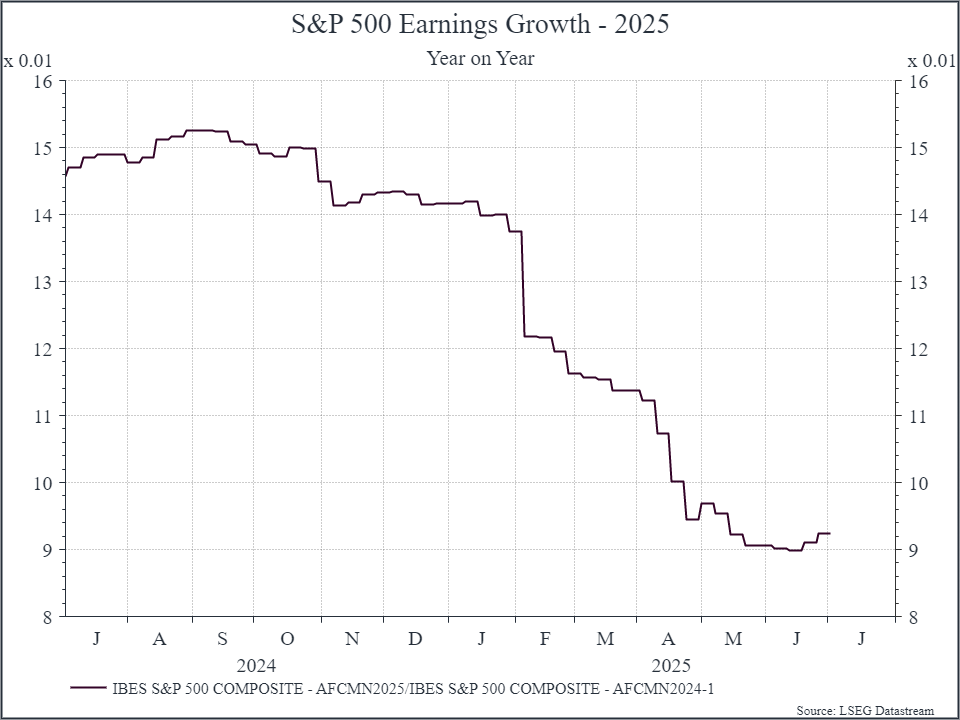

Second, we’ve seen forecasts for earnings growth in 2025 begin to stabilise. The chart below illustrates the point. It shows the forecast for 2025 earnings growth over time. At the start of the year, analysts expected earnings to grow around 14% this year. With increasing uncertainty around tariffs and economic growth, we saw analysts cut their estimates bringing expected growth to around 9% – still a decent expected growth rate.

Over the past month, those forecasts have stabilised. We’d argue this stability reflects a bit more comfort on the economic outlook, as projected tariff rates have come down, and renewed optimism that Artificial Intelligence will continue to drive investment spending among large tech businesses, and many others, in the coming quarters.

In terms of macro data, the most recent labour market report, reported early ahead of the July 4th holiday, showed a better than expected performance. The chart below shows the growth in monthly jobs compared to a consensus of economists. This is the third consecutive month with better than expected figures.

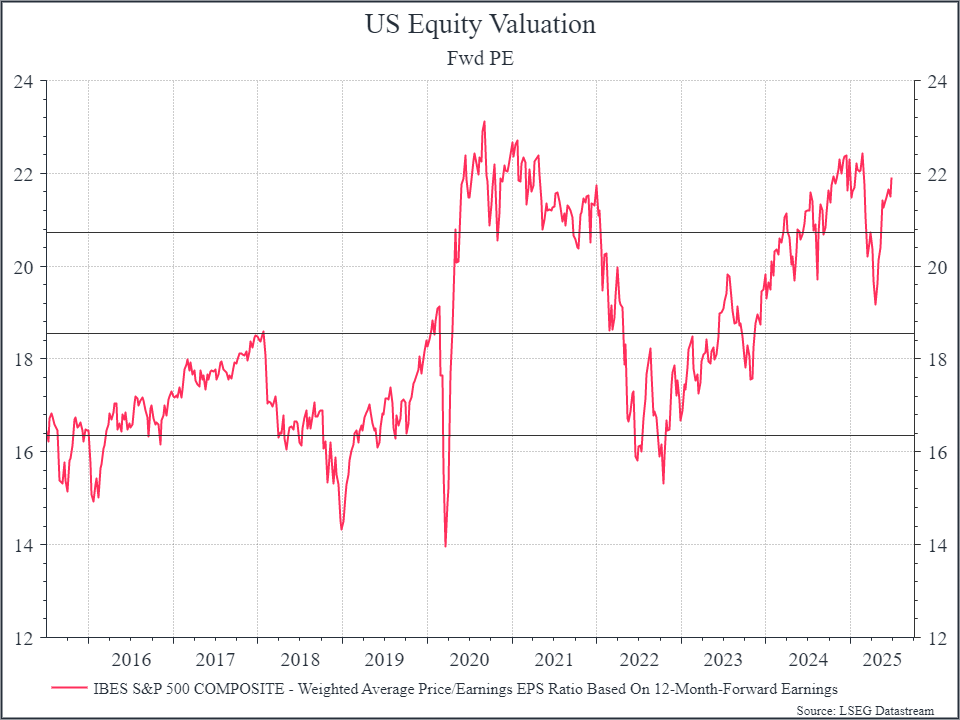

So, AI spending seems solid, tariff fears have diminished, macro data looks reasonable. What else should we consider? US equity valuations are back in focus. The chart below shows the 12-month forward Price/Earnings ratio for the S&P 500. It’s not quite as high as it was at the end of 2024 or during Covid, but we’ve clearly seen a re-rating over the past month.

It’s also worth remembering that tariffs haven’t disappeared. If the blended tariff into the US settles at around 10-15%, that would still be a significant increase on the 2-3% blended tariff in place at the end of 2024. It’s much easier to digest than the figures being thrown around in April, but we’d still expect to see some impact in the coming quarters, even if it might prove quite mild.

Then there’s the US budget that has now been passed by Congress. It implies that the budget deficit will remain pretty high (estimated to be in the order of 6% of GDP) in the coming years. Equity investors are currently more focused on the prospect of lower corporate tax rates – that should improve corporate earnings going forward – rather than the increasing government debt. There are still questions about the long-term sustainability of US government spending, investors seem willing to finance it for now. That will likely be helped by some regulatory changes that will allow US banks to hold more Treasuries on their balance sheets.

In some ways it’s quite a familiar story for US equities. We’ve seen strong recent equity performance, driven some decent macro data and a continued tailwind of tech spending. At the same time, starting valuations are above their long-term average and some of the policy concerns, on tariffs and geopolitics, are still with us. For now, the more negative scenarios we had considered in April and May seem less likely, and that’s good news. But after a strong recovery in the past couple of months the outlook for US equities for the rest of the year remains quite finely balanced.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.