This week, the US government announced new tariffs on a range of countries – including the Philippines, Algeria and Sri Lanka. But it was potential tariffs on specific sectors that caught our attention. President Donald Trump announced that imports of copper would face a 50% tariff, while foreign pharmaceutical products could face a 200% tariff – potentially delayed by a year to allow the industry to respond.

At this point, we think investors have learned not to react to the initial tariff headlines and expect some rounds of negotiations. Global pharmaceutical stocks didn’t really react to the latest announcement, although they have been in the cross-hairs for some time. But we think the focus on strategic sectors is likely driven by a desire for increasing self-sufficiency by encouraging domestic production of key products.

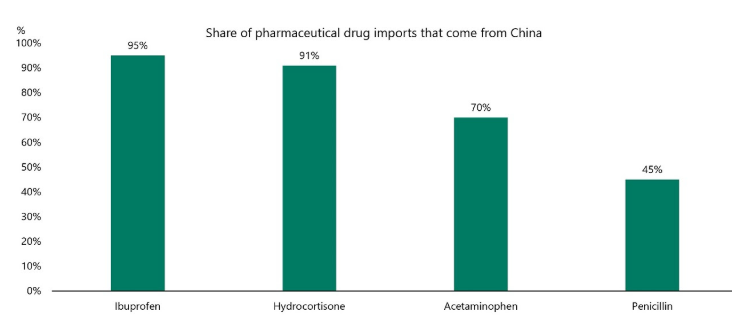

The chart below from Torsten Slok at Apollo illustrates the point. It shows the percentage of drug imports into the US from China.

Similarly, it’s estimated that around half of US copper consumption is imported, mostly from Chile and Canada. Copper is a key input in construction and electrics. Recent, short-lived, restrictions on rare-earth exports from China to the US were a reminder of potential vulnerabilities.

Even if the timing and scope of any new tariffs remains unclear, we would expect to see continued focus on encouraging more domestic production in the US. And with the US taking the lead, we could also see so-called onshoring in other regions around the world.

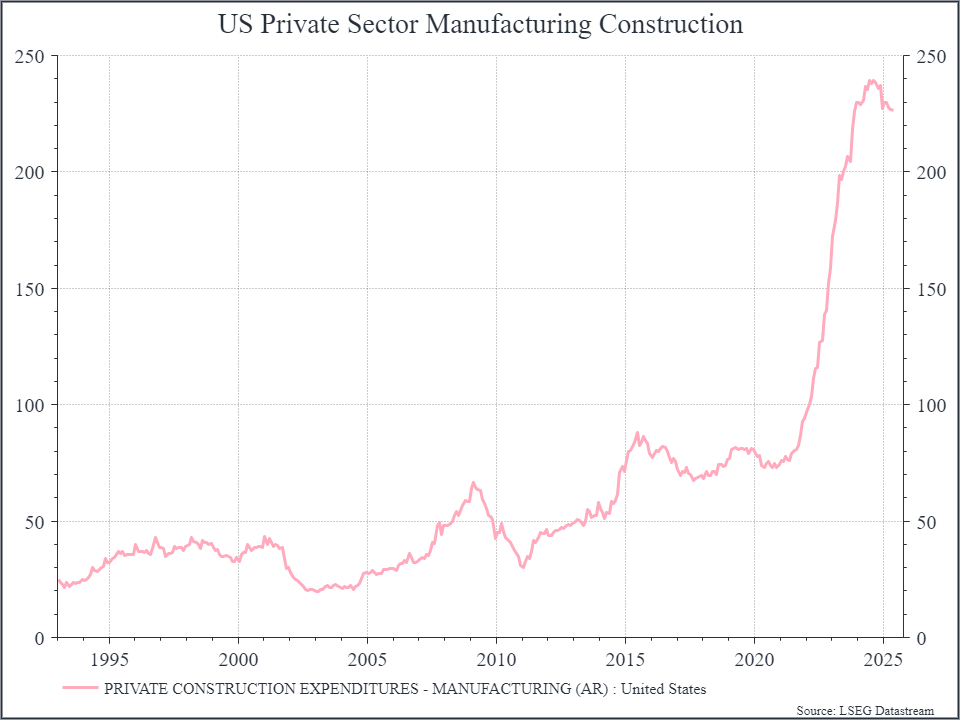

We’ve already seen US companies react to incentives in the recent past. The chart below shows a measure of US manufacturing construction. It shows a sharp increase thanks in part to the impact of legislation from the Biden administration.

The current administration might have a different approach and focus on different sectors, but the underlying desire to increase domestic production seems pretty consistent.

What does that mean for markets and investors? We think there are a few points to make.

First, we think that the process could take years – even if there is a framework of incentives in place. Building new copper mines and smelters, or new drug manufacturing plants, takes time. These have historically been quite highly regulated industries, requiring extensive permitting and licenses.

Second, it’s difficult for businesses to plan for long-term capital investment based on government policies that could potentially change. We’ve already seen commodity CEOs pushing for greater certainty around pricing – essentially asking for governments to commit to contracts – as an incentive to invest. If governments believe that’s priority then we could see it reflected in increased government spending.

Third, it’s another reminder that government policy can drive financial markets – perhaps even more so than in the past. It’s not just about central banks and interest rates, but increasingly industrial policy. We’ve seen it most notably with defence stocks so far this year, as they’ve reacted positively to commitments for greater defence spending in Europe.

Finally, if we see a shift in priorities from low-cost production to onshore production, we could see higher prices as a consequence. But governments around the world might decide that higher prices in strategic industries could be a price worth paying for greater security. And that might allow domestic producers to earn a higher return.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.