The Chinese government announced a package of stimulus measures over the past couple of weeks.

What’s the context? Over the past year or so, the Chinese economy has generally been weaker than many had expected. The reopening of the economy post-Covid didn’t produce much of a bounce to economic activity.

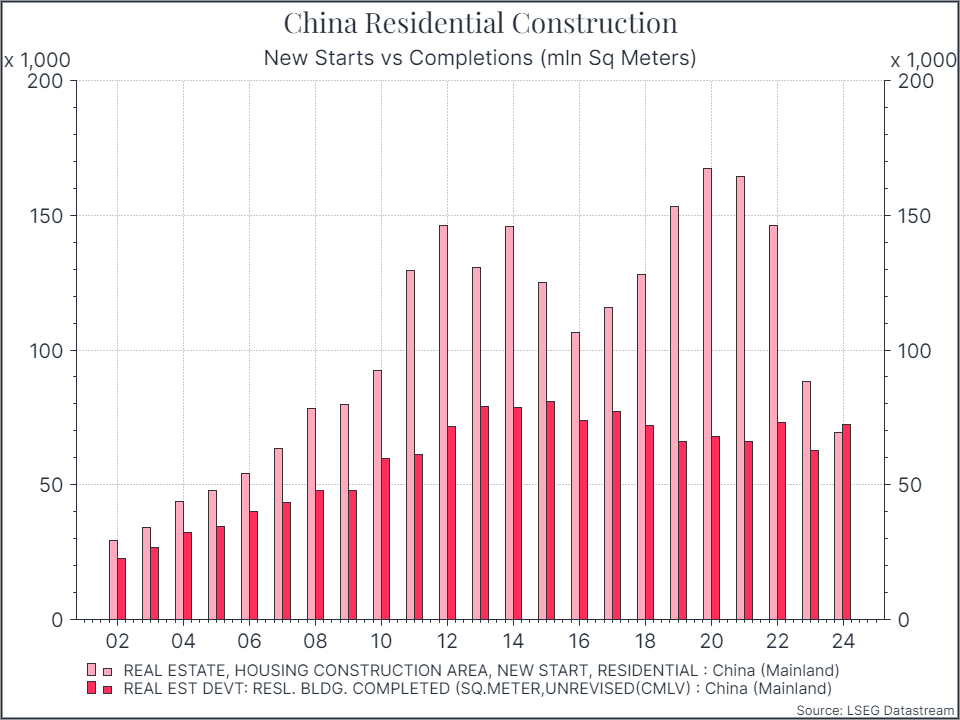

The housing market has played an important role here. We’ve seen a number of property developers in financial difficulties and, as the chart below shows, that’s had an impact on activity in the sector, with new starts in construction falling sharply.

We see the impact of that in monetary aggregates, where M2 growth is quite negative.

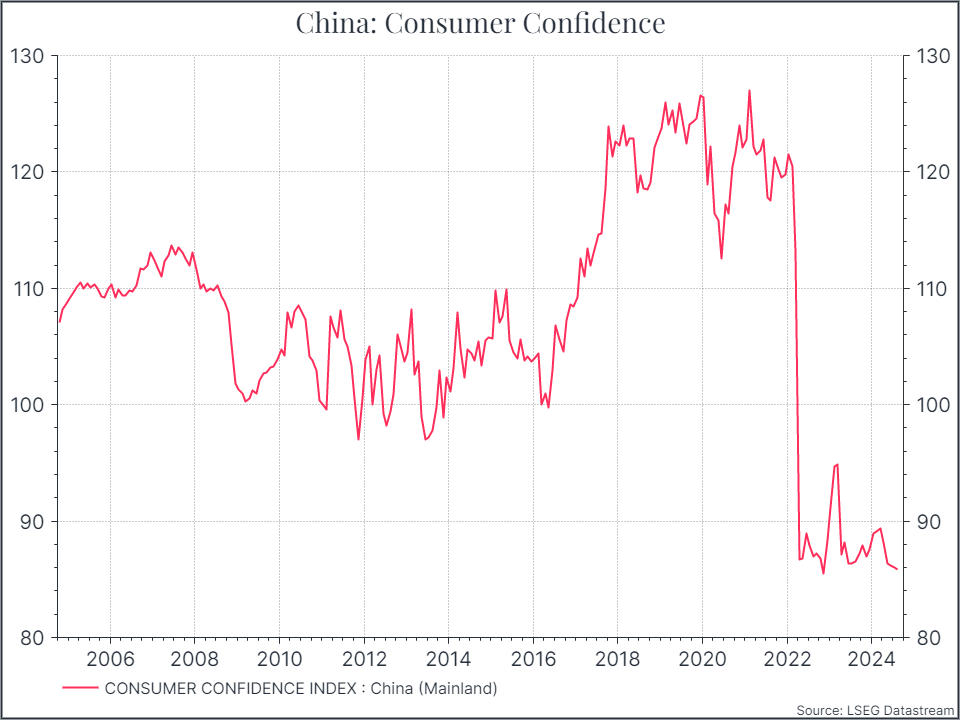

We also see a similar story in consumer confidence, which hasn’t really recovered from the Covid hit.

And, perhaps not surprisingly, in retail sales growth, which has been quite pedestrian.

What was the response? In some ways, it was perhaps surprising that the Chinese authorities didn’t react sooner to the slowdown in demand. Various commentators have been calling for a policy response for some time and it’s something that we’ve seen in the past from the Chinese government (and many others).

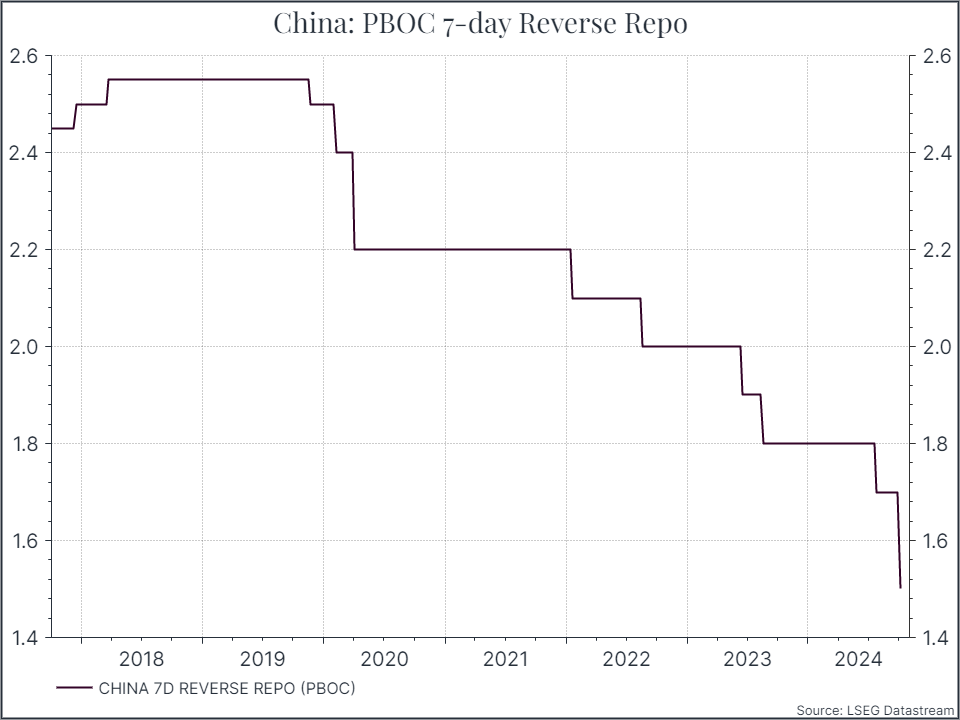

Now, we have seen a more meaningful reaction from the authorities – another sharp cut to one of the main interest rates (see chart below), but also some support for the housing market and some direct intervention in the equity market.

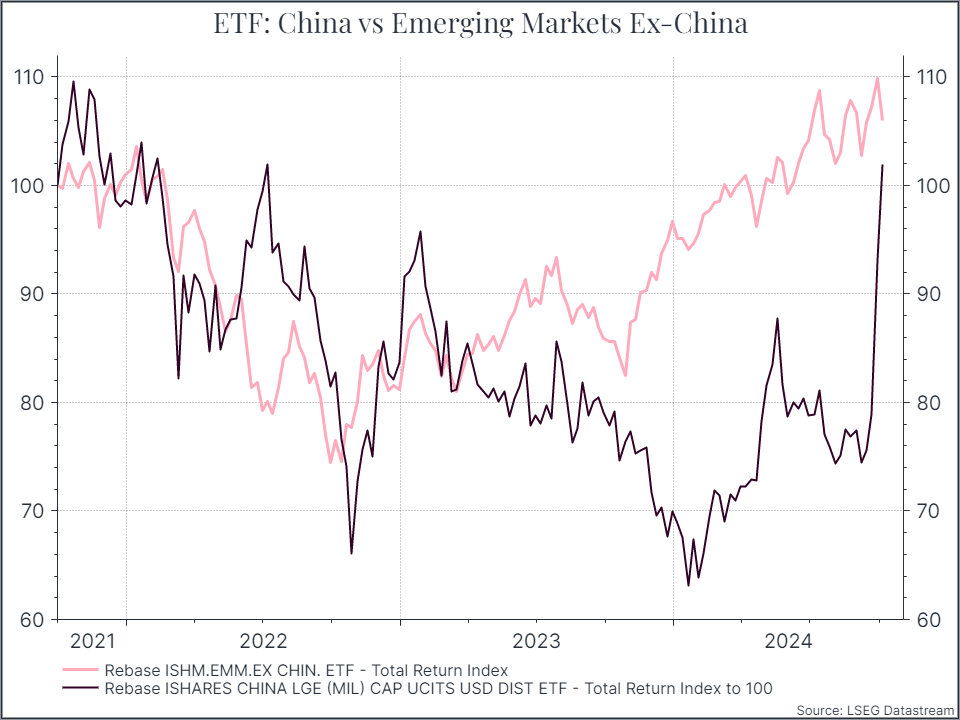

As you might imagine, the reaction from the equity market has been quite vigorous. It’s a reminder how much government policy can impact investor returns, and not just in China.

The chart below shows the performance of a China equity ETF compared to an ETF investing in Emerging Markets outside China.

Chinese equities underperformed significantly from the early part of 2023, as the re-opening post Covid had less of an impact than many had hoped. Equity markets have reacted strongly to the recent policy announcements, closing much of that performance gap.

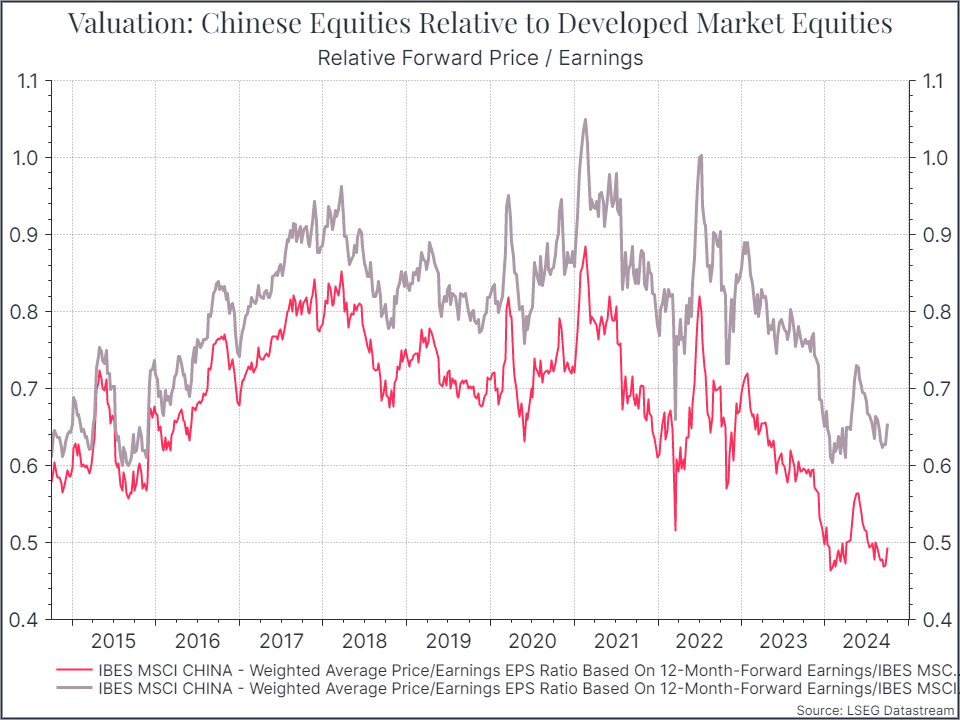

The chart below shows the relative valuation of Chinese equities compared to Developed Market equities and Non-US equities prior to the announcements. In both cases, we can see the pretty consistent de-rating of Chinese equities over the past couple of years.

Is this move sustainable? These policy moves don’t solve all the challenges facing the Chinese economy. The property sector still faces significant headwinds, and the knock-on effect on consumer confidence won’t dissipate soon.

Also, announcements like these obviously don’t address long-term demographic questions that China, and other countries, face. But policymakers are signalling that they’re focused on addressing some of these concerns and improving investor sentiment more broadly. That should be enough to sustain the move in Chinese equities for a while longer.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.