In recent months, China watchers have frequently discussed neijuan – “involution”: growth without evolution, or, as one Chinese news outlet put it, “fierce competition among companies for limited resources.” It’s something that Chinese officials have been increasingly concerned about and appear keen to address. We wanted to dig into this in a bit more detail.

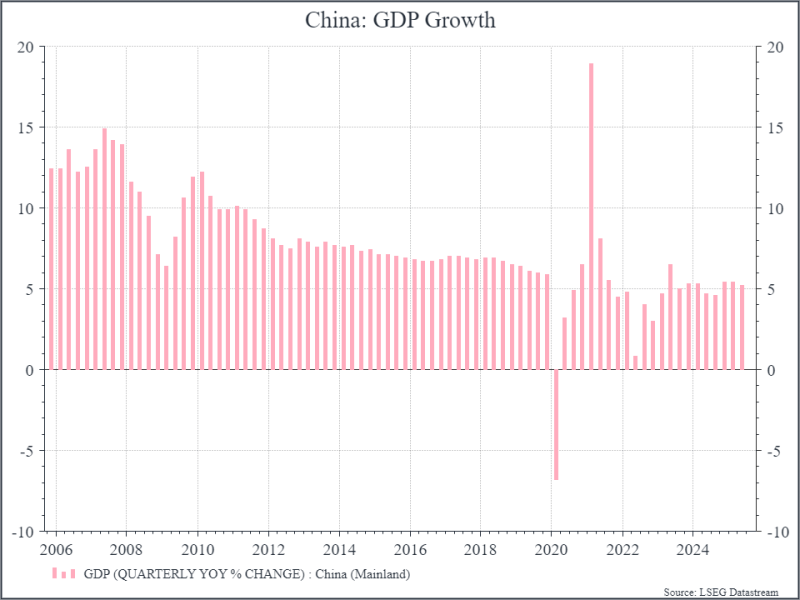

First, it’s well known that the Chinese economy has grown significantly for an extended period of time. The chart below shows official statistics for annual GDP growth over the past twenty years. Even though growth has been slowing in recent years, we’re still seeing the overall economy growing at around 5% per year.

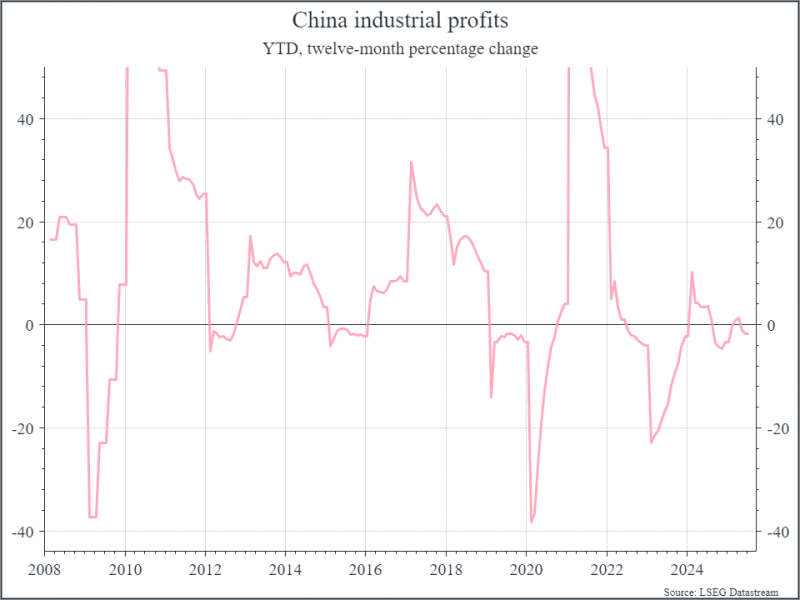

But despite this growth, it’s not clear how much Chinese companies have benefited. As an example, the chart below shows the growth in industrial profits. Barring a couple of periods of sharp recovery following the Global Financial Crisis and Covid, industrial profit growth has been fairly muted, particularly in recent years, despite significant economic growth and investment.

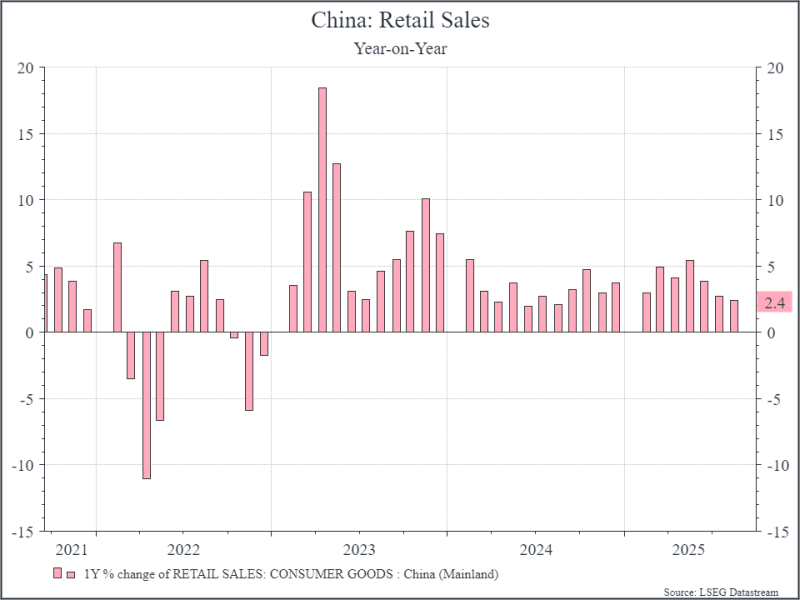

Analysts often argue that weak industrial profit growth reflects excess investment in new plants and equipment. We’ve seen that China’s investment spending, as a percentage of GDP, is far higher than its global peers – while its consumption spending is lower. We can also see that the growth in retail sales has been fairly pedestrian in recent years, as shown in the chart below.

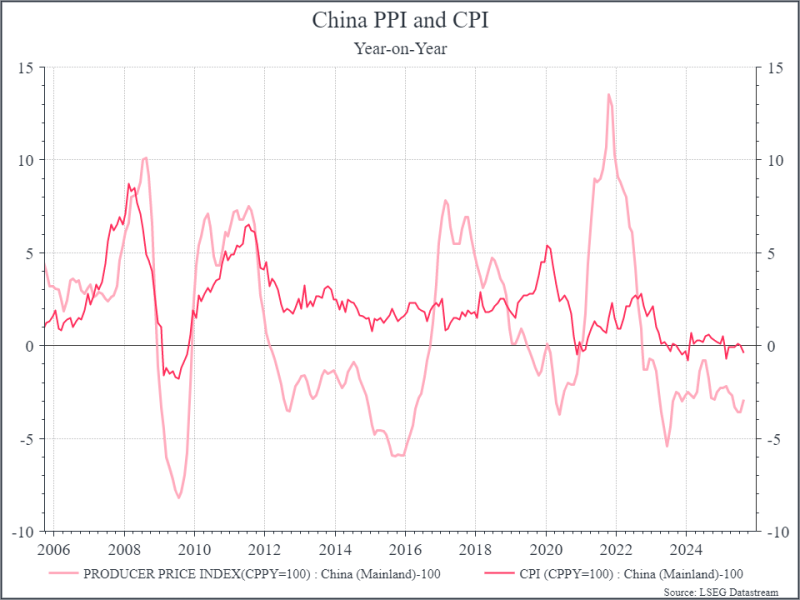

Finally, we can see this excess capacity reflected in inflation data. The chart below shows annual consumer and producer price inflation. Consumer prices are basically flat, while producer prices are declining. That might be good news for consumers outside of China, who might benefit from lower prices for Chinese goods, but it doesn’t help Chinese companies, or the global companies competing against them.

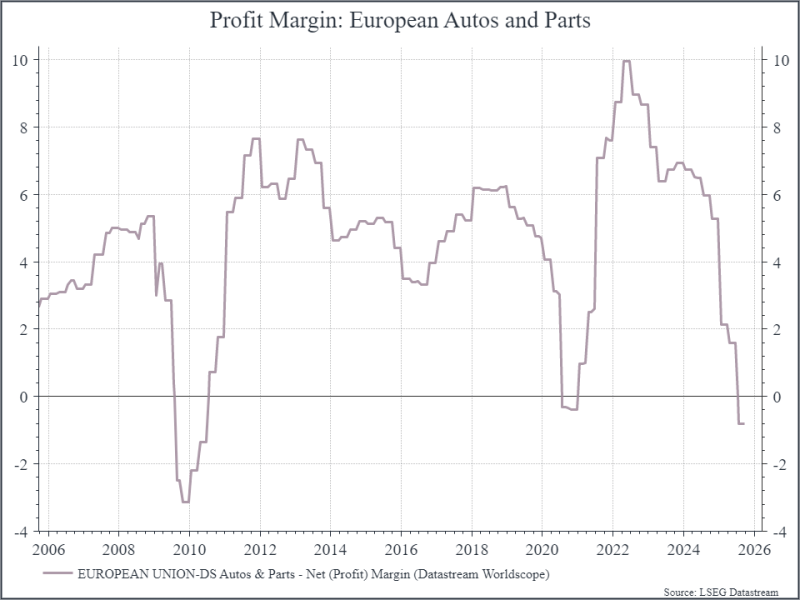

The electric vehicle industry is a particularly relevant example, with a large number of Chinese manufacturers gaining share in their domestic market and increasingly exporting their cars overseas. The chart below shows the profit margin for the European auto sector. We think that the sharp declines we’ve seen over the past couple of years reflects the increased pressure from Chinese competitors.

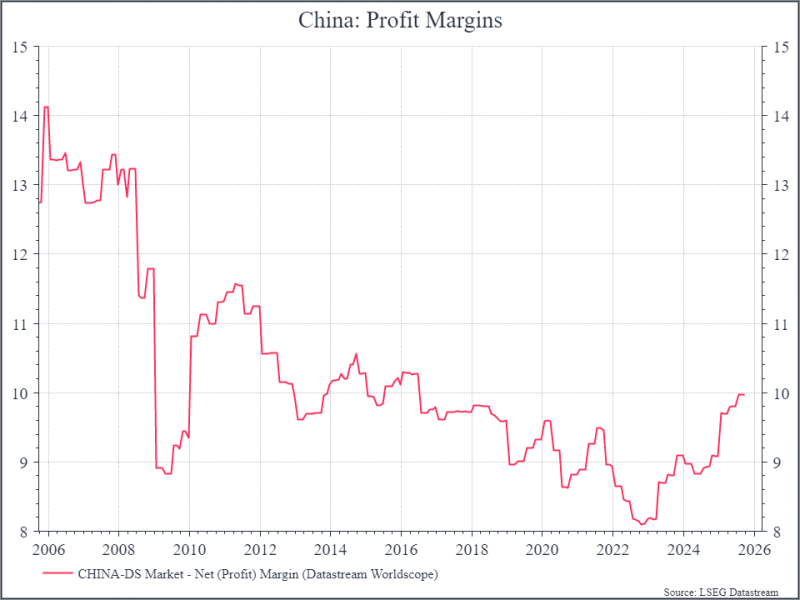

For some time, Chinese officials have tried to encourage domestic consumers to spend more, but so far without much success. Now we see that officials are also focusing on managing the supply side, potentially to improve profitability across a range of sectors and avoid deflation in the domestic economy. It’s probably too soon to say what the impact will be – Chinese officials have done this in the past. But we think the chart below is worth highlighting. It shows profit margins for Chinese businesses, as measured by Datastream. We can see a steady drift down in margins from 2011 onwards, at a time when US profit margins, for instance, were steadily rising. From 2024, however, we’ve seen overall profit margins in China move higher, perhaps helped by a shift in policy.

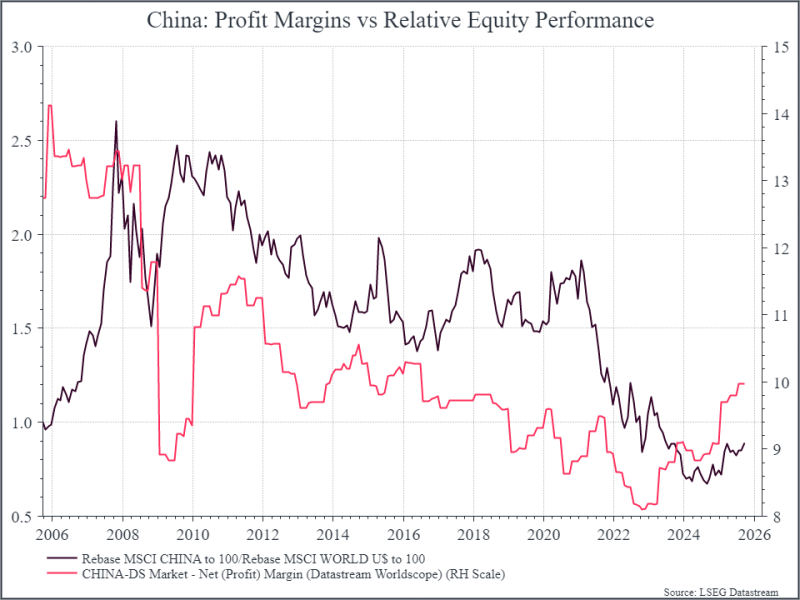

A better profit outlook for Chinese businesses could have a positive effect on Chinese equities. The chart below compares the relative performance of Chinese equities to developed market equities (the black line). We can see that China has underperformed developed markets over the past decade, particularly in the post-Covid period.

But in recent quarters we’ve begun to see some signs that the Chinese equity market is recovering, at least compared to developed market equities, perhaps coinciding with improved profit growth.

If Chinese officials are successful, and profit margins move higher, we could see Chinese equities continue to perform well. We continue to maintain exposure to Emerging Market equities, including China, across most of our equity and multi-asset portfolios.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.