2025 was an extraordinarily eventful year for financial markets. The year began with widespread uncertainty around equity valuations and the likely policies of the new Trump administration. This culminated in April with the so-called Liberation Day: the administration announced a long list of trade tariffs, effectively marking the start of a new global trade regime.

The immediate result was striking: the VIX index of market stress surged, while many equity indices flirted with a 20% drawdown. It was a moment of genuine uncertainty for markets and, according to some commentators, even the beginning of the end of American exceptionalism. With little recent history to fall back on, investors worked to construct scenarios for a fairly radical policy shift, trying to calibrate the potential impact on growth and inflation.

As is often the case in markets, however, this spike in geopolitical volatility proved temporary. From the April peak – both in terms of rhetoric and market stress – a more optimistic and constructive interpretation began to take hold.

Investors began to view the tariff announcement as the start of a prolonged tripartite negotiation between the US administration, foreign governments and financial markets, particularly focused on the cost of US government debt. These negotiations proved at times noisy and distracting, but ultimately led to a more benign scenario than we might have feared at the start of April.

Many of the key macroeconomic factors have evolved more favourably than initially expected. Growth held up, and Congress swiftly approved a very expansionary fiscal package. The plan made large tax cuts for businesses and households permanent, while adding substantial government subsidies for technology and defence. This unprecedented liquidity injection supported markets and consumption, allowing the US economy to continue growing despite elevated interest rates. Concerns remain over rising US government debt but so far investors appear willing to finance those deficits.

At the same time, the labour market showed some – not overly alarming – signs of strain, allowing the Federal Reserve to remain “dovish”, maintaining a more accommodative stance on interest rates while keeping recession fears contained.

Finally, the DOGE plan to cut public spending remained largely symbolic. Despite bold claims about eliminating trillions of dollars of waste, the department ran into political and bureaucratic reality: much of US public spending is legally ring-fenced – such as healthcare and social security – and cannot be cut by decree. As a result, while the plan delivered meaningful deregulation and some visible but limited cuts to smaller agencies, its overall impact on the federal budget fell far short of initial promises.

As the icing on the cake, the theme of Artificial Intelligence (AI) brought market attention squarely back to the US, with AI-related data centre investment alone estimated to add around 1% to GDP.

In summary, what emerges is a picture of a more pragmatic government than initially expected, significant delays or scaling-back of proposed tariffs, broadly supportive fiscal and monetary policies, and, above all, the powerful tailwind provided by the AI revolution.

Tariffs did have an impact, but a relatively contained one, effectively acting like a tax and being more than offset by the surge in AI-related investment. From the April lows, the Nasdaq – the technology-heavy index – rose by around 44%, while the S&P 500 – which tracks the largest US-listed companies – gained 35% (in dollars, as of 15 December 2025), marking one of the strongest cumulative rallies ever recorded over such a short period.

Pragmatism prevailed, American exceptionalism remains intact for now, and the AI theme continues to divide opinion between those who see a boom and those who fear a bubble. With 2026 now approaching, we wanted to pause and reflect on the key lessons from the year, with an eye on the next 12 months.

1. Markets remain the ultimate arbiter of political decisions

During the weeks of tension in April in the US, markets once again demonstrated their ability to act as an impartial judge of political choices. As seen during the UK debt crisis in 2022 or Italy’s sovereign spread crisis in 2011–2012, the Trump administration also ran into market scepticism – a factor that may have contributed to the softening of rhetoric and the announcement of a 90-day tariff pause on 9 April.

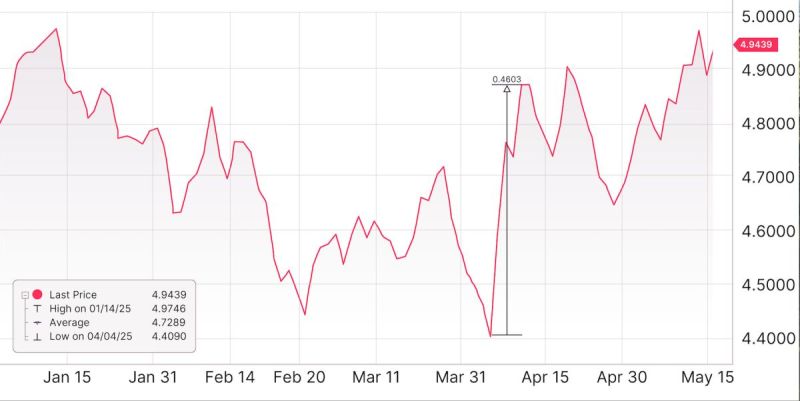

In the preceding week, investors did not just sell equities but also applied significant selling pressure to bonds and the dollar – assets that typically benefit during periods of stress. The result was a rise of nearly 0.5 percentage points in US 30-year Treasury yields.

This move signalled weaker demand for US debt, or alternatively the need for higher yields to compensate for rising concerns around fiscal sustainability and, ultimately, the country’s ability to meet its obligations.

The chart below shows US 30-year Treasury yields and their movement during the market turmoil in April.

In effect, this was a major vote of no confidence from financial markets, one that even a resolute administration like Trump’s could not ignore. The reality is that the global economic and financial system is deeply interconnected, and attempting to disrupt its balance aggressively can generate powerful backlash. Markets remain a key stabilising force and a critical arbiter of political decisions, even under more disruptive governments.

2. Geopolitical volatility is the new normal

2025 forcefully reinforced the importance of managing panic and staying focused on economic and corporate fundamentals. From Liberation Day to crises in the Middle East and the war in Ukraine, and the mini trade war between the US and China, the investors who fared best were those able to manage behavioural biases and navigate volatility effectively.

In an increasingly multipolar world shaped by the new US administration, volatility is unlikely to disappear. More than ever, it is important to rely on professionals whose role is to focus on what truly matters, invest rationally, and construct resilient portfolios while managing behavioural pitfalls.

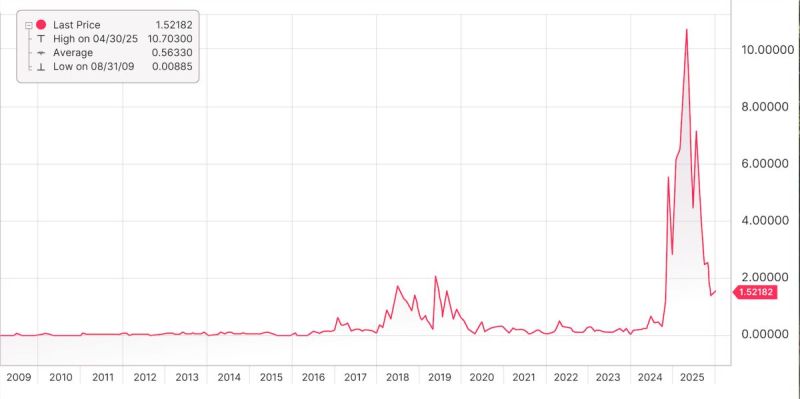

The chart below shows Bloomberg’s Trade Policy Uncertainty Index, highlighting the start of a new regime following Trump’s election.

3. Diversification is making a comeback

2022 was a difficult year for diversified portfolios, with equities and bonds falling together. Even today, the correlation between the two asset classes has not fully reverted to offering its traditional diversification benefits.

That said, with interest rates now stabilising and the fight against inflation either won or nearing its final stages across most major economies, we expect diversified portfolios to once again represent the most sensible long-term investment approach – not because they guarantee higher returns, but because they aim to deliver better returns for a given level of risk.

2026 will begin with elevated valuations and an unusually high concentration in US equities. While we remain optimistic about US technology and the AI theme, this view is embedded within well-constructed and diversified portfolios. This is precisely why we continue to caution against excessive concentration in individual risk factors.

The chart below shows euro-denominated returns across different asset classes and a 60/40 portfolio. As highlighted in the two columns on the right, over the past ten years this type of portfolio delivered the third-highest return while ranking sixth in terms of risk, illustrating the value of diversification.

4. Markets are usually right

After the April sell-off this year, markets staged a remarkable recovery. But according to the AAII asset allocation survey, retail investors’ equity exposure did not return to late-2024 levels until October, while the S&P 500, in dollar terms, had already recovered to early-January levels by May.

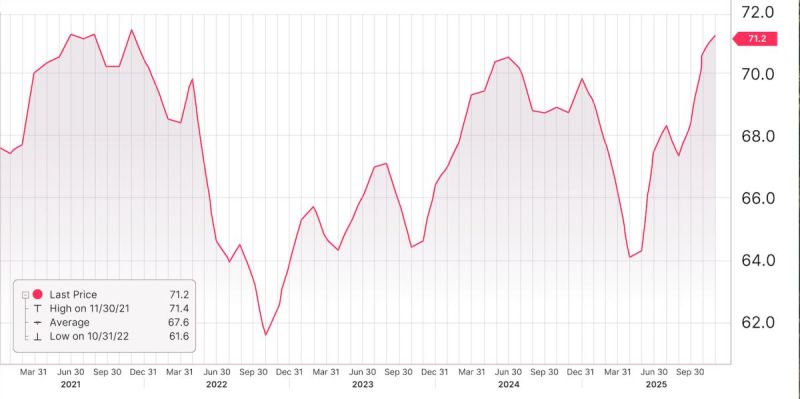

The chart below shows the total equity allocation of US investors, according to the AAII monthly survey.

While the pessimism was understandable given tariff concerns and uncertainty around their impact, the summer of 2025 offered yet another reminder not to underestimate markets and their ability, collectively, to price in and anticipate the most plausible scenarios.

Markets are generally efficient in the sense that they absorb relevant information quickly and translate it into fair asset prices. This does not mean there are no opportunities for outperformance – as demonstrated by Moneyfarm portfolios over time – but it does reinforce the importance of remaining humble and agile when investing.

5. Breaking down bubble fears with more granular analysis

In recent months, we have seen an increasing use of the word “bubble” in reports, referring to AI-related stocks, often accompanied by comparisons – in our view misguided so far – with the early-2000s dot-com bubble.

As noted, we remain optimistic about the AI revolution. We believe recent market performance is supported by strong fundamentals and robust business models across much of the tech sector, and that AI can continue to drive a growth boom.

For now, large investments in data centres and related infrastructure are being funded primarily through cash rather than debt – a reassuring sign. Valuations are high, but well below the extremes seen in the early 2000s.

2025 has forced us to make our analysis even more granular and detailed in order to dismantle bubble fears. Over the year, we developed new analytical frameworks around major tech names and the AI theme, concluding that for now we are dealing with a boom rather than a bubble.

Looking ahead to 2026, we will continue to monitor AI from multiple angles. In the meantime, we maintain some targeted exposure to US tech, always within a disciplined, diversified and risk-aware framework.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.