UK investors are, in general, much less interested in investing in government bonds than their European counterparts. In Italy, for example, BTPs (Italian government bonds) are one of the most held investment products. But since the Budget, with the increase in the capital gains tax rates and a very promising and rare price environment, we have seen UK government bonds come much more into focus. The fact that they are exempt from capital gains tax is increasingly drawing investors in. But does this make them gold dust? Should you be adding them to your holdings?

What are gilts and how do the returns work?

I don’t want to take everyone back to school, but to frame the conversation it’s important to have an understanding of how it all works.

Gilts are UK government bonds. A bond is essentially a debt: you lend the UK government £100 for a set period and then they will return that £100. There will be some interest payments over that period – usually every 6 months – based on the interest rate at the time that the money was borrowed (with perhaps a little bit extra for any credit risk). These bonds can then be traded among investors. The price fluctuates based on a variety of factors, but crucially it depends on how the interest rate on the bond compares to current (or expected) interest rates.

For example, if you are holding a bond that pays 3% of interest, but interest rates go up to 5%, the price of your bond will fall, as demand for something that pays less than current interest rates will go down. Conversely, if you are holding the same 3% bond but interest rates drop down to 1%, then the price of your bond will go up as you are getting more interest than is currently available.

So, from a bond there are, loosely, two types of returns. There can be capital gain, so returns that are made by price moving in your favour. Then there is interest income, which is the income payments that are made to you while you hold the bond.

Crucially, if you hold the bond to the end of its ‘term’ you will get the £100 repayment.

It’s worthwhile remembering that gilts are ‘capital gains’ tax free, but you still have to pay income tax on the interest – as with any bond or cash account.

A unique opportunity

The rules on the tax-free nature of gilts are usually not that exciting. In a stable interest rate environment, the prices don’t move as much (unless you have a really long-term bond) and most of your return comes from income – which is taxable.

However, we are currently in a scenario which hasn’t been seen for some time. Because, even 2-3 years ago interest rates were incredibly low (around 0.5%) and had been since the financial crisis, a lot of gilts were released with really low interest rates. When interest rates suddenly raced to more than 5%, the price of these bonds plummeted. This wasn’t particularly fun for anyone holding bonds, but it does now present savers an opportunity for a tax-free solution.

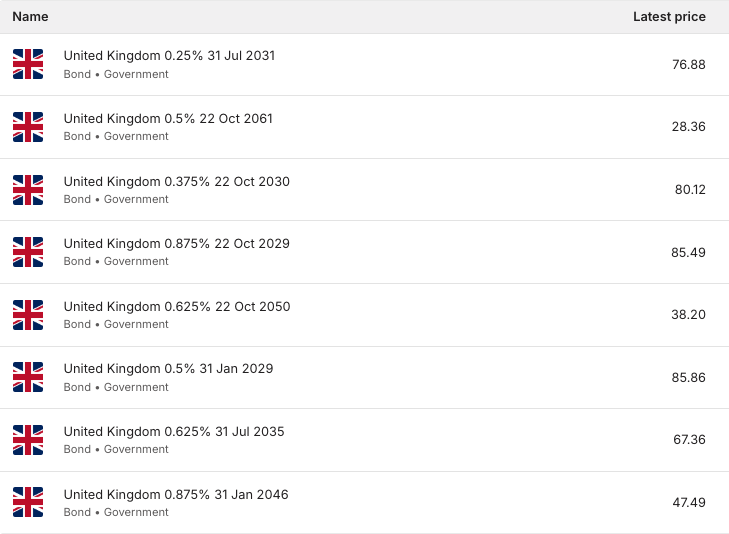

Prices as at 18/11/2024 – these prices will fluctuate.

If you look at the selection Gilts below par which we have on our Share Investing platform, you can get a good visual sense of what we’re talking about. These are all bonds which will repay £100 at the end of their term (the date listed in the name). But because the interest rate is so far below current interest rates, the prices are quite far below £100 (the further you are away from the ‘maturity’ the lower the price, because no one wants to accept 0.5% interest for 40 years if you were focussing on income).

So, if you bought the top one, you would pay £76.88 for every bond and on the 31st of July 2031, the government will pay you £100 for each one and that return would be tax free. You would get 0.25% per year (i.e. 25p per bond per year), but this is fine because the income is not tax free, so outside a tax wrapper you are happy for it to be lower.

Hold to maturity or buy and sell: what are the risks?

Many of you are probably looking at the above and thinking; “Yes, but 2061 is very far away” – and you are right. But you don’t always have to hold them until the end, you can sell them just as easily as you bought them. Particularly if you anticipate that bond prices will go up (possibly due to a view that interest rates will drop more quickly than expected). However, this comes with different risks as well – such as those related to bond pricing.

If you do hold a bond to term, you will be paid the £100, regardless of how the price fluctuates in the meantime, unless the other entity – in this case the UK government – is not able to pay you back. This is called credit risk and is essentially the only key risk that you face if you are planning to hold the bond to par. This is very low risk when it comes to UK government bonds. So that would make this, on the whole, a low risk investment.

However, if you were planning to buy a bond because the prices are low with the view that you could sell it in the future, you are open to a variety of other risks which affect the price of a bond. These could be a change in inflation expectations (an increase would be bad for a bond price), or it could be a big change in the borrowing behaviour of the government (as we saw recently, which also leads into the first point) which may affect investors view of future rates and, in extreme situations, a change in the creditworthiness. It could be other macroeconomic factors, like strong labour market statistics, which decrease the likelihood of a rate cut or similarly high-wage growth.

So, whilst the buy and sell strategy can result in realising gains sooner – which would still be free from capital gains tax – you could certainly end up selling for less than you bought if factors moved against you.

This unique situation of having 0.25% bonds on offer when rates are still 4.75% is suited more to creating a low risk, capital gains tax-free return holding it to par.

In this world of strong equity returns and high interest rates on lower risk assets, the returns won’t immediately get people salivating – it’s worth bearing in mind that outside of ISA, JISA and pension tax wrappers, you could be paying up to 45% tax on the interest gained in a bank account* (suddenly 4% looks more like 2.2%) and 24% capital gains on other investments. So, the – very very crude mathematics here – roughly 30%** return in just under 7 years on offer on the top gilt above, capital gains tax free and relatively low risk, is becoming a proposition that more and more people are interested in.

Where would this fit into an overall allocation?

The first port of call is always still to fill the tax wrappers that you have available to you and to invest in an asset allocation that is fit to your time horizon – generally more equities for the long term and more fixed income for the shorter term.

But after the last few years of tax-free allowances outside of the wrappers being cut – capital gains allowance down to £3,000, dividend allowance down to £1,000, interest down to £500 for higher rate tax payer – and with tax rates being increased (or frozen, in the case of income) there are fewer and fewer places to hide. In the case of income tax, for those paying 40% or 45% on their salary, this rate now also applies to their cash savings (over the allowance of £500 of interest). More and more people are starting to have to think about this, as it starts to eat meaningfully into the returns they are making.

However, holding a bond to par is quite unique in the sense that you know exactly when your payout is going to be – so that has to be relevant in the planning. If your goal is before that date, you can take on the volatility and try to benefit from the ‘pull to par’ – when it still trends towards £100 as you get closer to the end of the bond’s term – but it may not be the best option.

If your goal is around that exact date, say retirement, then perfect – this could make a meaningful part of your allocation. This is actually how defined benefit pensions schemes work on a big scale. But again, the probability of matching the dates exactly is quite low.

Ultimately these types of investments are most relevant for clients with a meaningful amount of money outside of tax wrappers and a time horizon that is around or beyond the timeline of the gilt in question. This can then act as a diversifier against other investments, delivering a reliable return, tax free and being a counterweight to some other more volatile and cyclical investments.

However, this would not be the same as the short-term cash pot, as it would not really be an investment suitable for providing short emergency cash needs – although you can sell them at any time.

This is specifically related to the ‘gilts below par’. Individual bonds, particularly at the moment, can be a great source of income, with some corporate bonds still offering over 5% per year in interest payments. However, this is not tax efficient and should probably then be in a tax wrapper. While there’s much more to explore on this topic, we’ll save that for another time to keep this article concise and focused.

Speak to us

As always, you can reach out to our friendly team to discuss any of the points above – or anything else related to your financial situation. Alternatively, if you have anything on the above that you wanted to discuss further with me directly, I am more than happy to take your questions, please email me on christopher.rudden@moneyfarm.com.

*on interest earned over the allowance of £500 for a higher rate tax payer

**Using (100-76.88)/76.88 to give £23.12 return on a £76.88 investment

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.