For many people, the late 40s and 50s mark a turning point when retirement stops being a distant idea and becomes a pressing reality. Some are aiming for early retirement and want to ensure their savings will last, while others may feel they are “late to the game” and are only now starting to consider what their later years might look like.

Planning for retirement is not simple. There are many moving parts that can dramatically influence your quality of life in later years. Inflation may erode the value of income, people are living longer – raising the risk of outliving savings – long-term care costs are increasing, and tax rules are constantly evolving. Even state pensions, while helpful, are unlikely to maintain their full real value over time.

It’s easy to assume that you will “probably be fine” in retirement, but most people only discover shortfalls once they put all their assets, income, spending and timelines into a structured plan. Surveys consistently show how common this over-optimism is. The Saltus Wealth Index, for example, found that 96% of respondents underestimated how much money they would need for a comfortable retirement, even among individuals with substantial investable assets.

Similarly, the latest UK Retirement Confidence research from Nucleus revealed that only around a third of UK adults feel confident they will have enough money to live comfortably in retirement. In an environment of rising living costs and increasing taxation, this gap between expectation and reality has left many retirees facing a lower standard of living than they anticipated.

Given this context, recent changes introduced in the November 2025 UK Budget make careful planning even more important. These changes affect property income, savings, dividends, and pensions, altering the landscape for anyone over 50 who is planning for retirement. Understanding these changes is crucial for deciding how to allocate your savings and which retirement strategies will be most effective.

UK Budget 2025: changes shaping retirement

The November 2025 UK Budget introduced several measures that directly affect retirement planning. For those relying on property income, cash savings, or non-tax-efficient investments, these changes are significant.

Rental income from buy-to-let properties will face higher taxation from April 2027, rising to 22% for basic-rate, 42% for higher-rate, and 47% for additional-rate taxpayers. For landlords, this reduces net returns and raises questions about the viability of property as a central retirement income source. Beyond taxation, property ownership carries ongoing responsibilities, including maintenance, tenant management, and regulatory compliance, which may be burdensome as people age.

Cash savings outside tax-efficient wrappers are also affected. Interest earned on deposits in ordinary accounts will see a 2% increase in taxation across all bands, reducing the real return on cash holdings. Dividend taxation will rise as well, with basic-rate dividends taxed at 10.75% and higher-rate at 35.75% from April 2026. This diminishes the appeal of non-tax-wrapped investment accounts as a source of retirement income.

ISA allowances are being restructured. For under-65s, the annualISA allowance for the Cash ISA will be capped at £12,000 from April 2027, with the remainder redirected to non-cash investments. This adjustment encourages savers to focus on long-term growth via Stocks & Shares ISAs rather than holding large cash balances.

Finally, pension arrangements through salary sacrifice will face a cap on contributions benefiting from National Insurance savings, limited to £2,000 per year from April 2029. Personal contributions, however, will continue to attract full income tax relief. This ensures that pensions remain a highly effective vehicle for retirement planning, particularly SIPPs, which combine flexibility with significant tax advantages.

Taken together, these changes signal that relying heavily on property, cash, or non-tax-efficient investments is becoming less attractive. Tax-efficient vehicles, like ISAs and particularly pensions, are increasingly critical for maintaining retirement security.

Evaluating retirement planning options

With these Budget changes in mind, it is helpful to assess the main strategies for retirement planning and how they are affected.

Property

Property has historically been a cornerstone of retirement planning in the UK. According to the English Private Landlord Survey, 58% of buy-to-let landlords view their properties as a long-term pension investment, highlighting how central property has been to long-term financial planning. Many over-50s have used rental income to supplement pensions, and research by Savills estimates that retirement-age households hold around £378 billion in net buy-to-let property wealth, showing how long-term house price appreciation has contributed significantly to net worth.

However, the landscape is shifting. Higher property income taxes, rising maintenance costs, and stricter regulations have reduced the attractiveness of buy-to-let as a retirement strategy. Managing tenants and maintenance is also time-intensive, which can become burdensome when a more relaxed lifestyle is desired. While property still has a role, it may no longer be the reliable cornerstone it once was.

Cash savings

Cash savings remain popular because of their predictability and accessibility. They provide liquidity for emergencies or short-term needs and are often seen as a “safe” option. Cash ISAs and savings accounts offer peace of mind and immediate access to funds, which is essential in retirement.

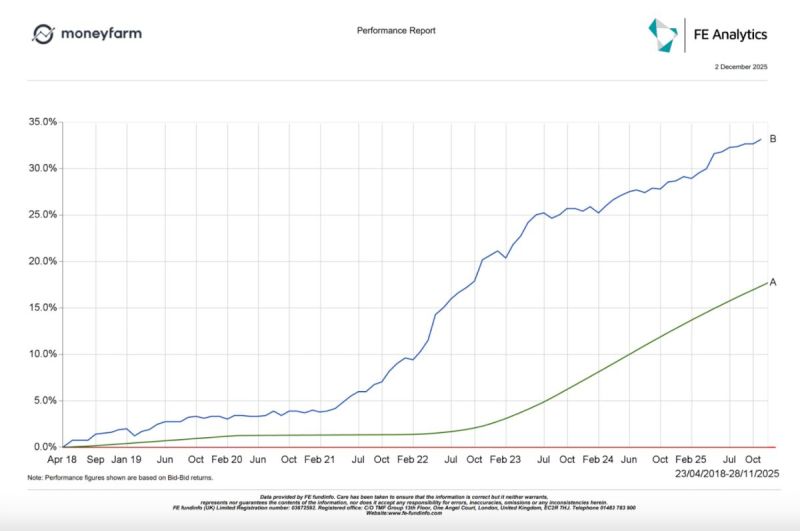

Yet relying too heavily on cash carries risks. Inflation erodes the purchasing power of savings over time, and recent tax increases on interest income further reduce returns. While cash has a vital role in providing security and liquidity, it is rarely sufficient for generating real long-term growth and cannot on its own maintain standards of living in a prolonged retirement. This is evidenced by the graph below where you will see that Cash (SONIA, Green) has significantly underperformed inflation over time (CPI, Blue).

Stocks & Shares ISAs

Stocks & Shares ISAs provide access to global markets, offering strong long-term growth potential in a tax-efficient wrapper. They allow flexible withdrawals without triggering taxes, making them a useful supplement to pensions. However, they lack the structured tax relief and retirement-focused benefits of a pension, meaning they may not be as efficient for generating sustainable retirement income.

General Investment Accounts

Many investors also hold non-tax-efficient accounts such as General Investment Accounts (GIAs). GIAs provide flexibility and broad investment access, but all growth and income are subject to taxation each year. With dividend tax rates rising and savings income taxed more heavily following the 2025 Budget, holding large amounts outside tax-efficient wrappers can significantly reduce net returns over time. For individuals nearing retirement, this makes shifting assets into ISAs or pensions increasingly advantageous.

Pensions and SIPPs

Pensions, particularly Self-Invested Personal Pensions (SIPPs), remain one of the most powerful tools for retirement planning, especially in the context of the 2025 budget where taxes on cash, property, and dividends are rising. SIPPs offer a tax-efficient environment: contributions receive immediate tax relief, investments grow free from UK capital gains and income tax, and retirement drawdown can be tailored to individual needs. This allows savers to protect and grow their retirement wealth where other assets are increasingly eroded by taxation.

SIPPs also provide greater control over investments. Unlike cash, which can lose value to inflation, or property, which can be illiquid and costly to manage, SIPPs let investors access global markets, diversify across funds, stocks, and bonds, and adjust allocations as market conditions change. Retirement drawdowns can be structured flexibly to suit lifestyle or income requirements, giving savers active control over how and when they access their funds.

Finally, SIPPs offer generous contribution limits that can significantly boost retirement savings. Those over 50 can contribute up to £60,000 per year, or 100% of pre-tax income, and can carry forward unused allowances from the previous three tax years. This makes them far more flexible and potentially lucrative than other tax-free wrappers, such as ISAs, particularly for late-career savings and high earners seeking to maximise pension wealth.

Choosing the right strategy

There is no single approach to retirement planning; your ideal strategy depends entirely on your personal priorities: growth, stability, flexibility, or tax efficiency. Asking yourself the following questions can help clarify what matters most:

- Could I benefit from additional tax relief on my retirement savings?

- Do I want flexibility and control over my investments as markets change?

- Am I comfortable with market volatility if it could help my retirement pot grow over the long term?

- Do I want to avoid the responsibilities and risks of property ownership, like tenant management or maintenance?

- How important is tax efficiency in protecting my retirement income and investments?

- Am I aiming for long-term growth, or primarily looking to preserve capital?

These questions aren’t meant to point you toward a single strategy. A balanced approach often works best: using a SIPP for long-term, tax-efficient growth alongside shorter-term options like a Stocks & Shares ISA or Cash ISA for liquidity and flexibility. This strategy helps your savings grow over time while keeping funds accessible when needed.

Planning for retirement can feel overwhelming, which is why professional guidance is so valuable. Our Guidance+ service is designed to help you create a personalised financial plan. Our Qualified Wealth Managers would be happy to assist in evaluating your retirement goals and helping you structure a plan that makes the most of tax-efficient savings. To discuss your options, you can book an appointment with our team.

This content is for general information only and does not constitute personal financial or tax advice. The value of investments (including property and pensions) can fall as well as rise. Past performance is not a reliable indicator of future results. Tax rules are subject to change, and tax treatment depends entirely on your individual circumstances. You should consult a qualified and regulated financial adviser or tax professional before making any investment or retirement planning decisions.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.