For those waiting for the usual 12.30pm start time for the Autumn Budget, you’d be right in thinking you were already playing catch up. The Office for Budget Responsibility (OBR) inadvertently – investigation still pending – leaked details of what was in store 40 minutes ahead of the session. Bond yields whiplashed as a result, reflecting a broader uncertainty over the Government’s ability to get a handle on public finances.

“These are my choices, the right choices” were the words put forward by Chancellor Rachel Reeves during her speech. Despite walking a political tightrope – making necessary adjustments to the UK tax system while avoiding anything resembling a 2022 Truss-esque horror show in financial markets – markets ultimately reacted positively once the dust settled. More on that shortly.

There are certainly significant impacts to the way in which the UK public will save and invest moving forwards, though fortunately, we do have time on our side to plan effectively before anything gets implemented.

What’s happening with ISAs?

Effective April 2027, the government is implementing changes to ISA contribution rules, primarily aimed at encouraging UK savers under the age of 65 to utilise financial markets and achieve better saving outcomes.

The overall £20,000 ISA allowance remains in place, but for individuals under 65 the amount permitted in Cash ISAs will be capped at £12,000. This presents an additional blow as the tax on savings income will increase by 2 percentage points for anything outside of a tax wrapper. Savers must allocate the remaining £8,000 to Stocks and Shares ISAs or consider less favourable options like saving accounts which don’t have the same tax-shielding benefits. Those over 65 are unaffected by the change.

This policy is designed to improve long-term saving outcomes, and it aligns with our view – shared by Number 11 – that taking measured exposure to riskier assets such as bonds and equities offers a greater likelihood of achieving positive, inflation-beating returns over time. Our own track record supports this view as well, and you can see the past performance of our portfolios here, bearing in mind that past performance is not a reliable indicator of future results.

With the government noting that 40% of Britons underfund their pensions, the reduction of the Cash ISA allowance to £12,000, while restrictive, may serve as a catalyst for a much-needed shift in saver mindset. If this nudges more savers, where appropriate, to utilise the Stocks and Shares ISA for the remaining portion of their allowance, the resultant long-term growth in personal wealth would be incredibly beneficial. A population with robust private investment returns is one that is less reliant on future state support, effectively assuaging cost pressures on a cash-strapped government.

The primary drawback is the complexity for short-term savers (0-3 year horizon) who require liquidity without market risk. Not all hope is lost however, as solutions do exist. For example, money market funds like those used in our Liquidity+ product can be wrapped within a Stocks and Shares ISA, allowing savers to maintain the full £20,000 allowance for short-term planning with the headache of adding undue risk to their position.

Our key message to this group of people is that they can still get their full Cash ISA contributions in for another 16 months, though this should be put in the context of their broader financial plan where a high allocation to cash may not be suitable.

Pensions back on the table

Always a popular subject matter in a Budget, some may see that the pension got off lightly with no reduction in the tax-free lump sum available at the point of drawdown. The notable change in this area is a £2,000 cap on the amount of salary sacrifice available to employers and employees, effective from 2029. It should be made clear that this only pertains to the National Insurance (NI) saving by funding your pension this way.

Under the change, the first £2,000 remains NI-exempt, but any excess is subject to standard employee (currently 8%) and employer (currently 15%) NICs, increasing costs for employers and reducing take-home pay for high-contributing employees.

A practical example

If an employee earning £50,000 sacrifices £5,000 annually into their pension, the £3,000 amount that is now over the cap will incur around £240 in additional Employee NI contributions (8% of £3,000), reducing the salary sacrifice benefit and the employee’s net pay.

The implication

While the removal of the National Insurance benefit above the £2,000 salary sacrifice cap may initially seem like a drawback, it represents a shift toward empowering pension savers with greater control over their retirement outcomes. With the NI benefit now negated for larger employer contributions, the tax treatment of making a personal contribution directly, such as into our SIPP, becomes functionally equal. This allows individuals, especially those nearing tax thresholds, to proactively choose where their money is invested.

Savers can gain a clearer understanding of their portfolio, reduce hidden costs, and align their investments with a personal, long-term risk profile, ultimately leading to more informed decisions and potentially improving the growth trajectory of their retirement pot.

Tax bands and tax rates

Income tax

As expected, much to the dismay of many, there is a freeze on income tax bands until 2031. This is known as a ‘stealth tax’ as wage inflation (which remains sticky at around 4%) nudges more people into the higher tax band. It’s thought that this will pull an additional 920,000 people into the higher tax rate in 2029-30.

One of the more popular methods of reducing your income, so as to not go into the next tax bracket and increase tax rates across things like interest and dividends for assets outside of tax wrappers, is by contributing to your pension. This remains one of the most tax efficient products available to Brits and will play an increasingly important role in mitigating tax and improving retirement outcomes.

Interest earned as income, dividends and capital gains tax

No changes to the allowances afforded to people, but some movement on the rate people pay above given allowances and outside of tax shielding products.

The tax rates on dividends above the universal £500 allowance are shown below.

| Who | Current Rate | New Rate (from April 2026) | Change |

| Basic Rate taxpayers | 8.75% | 10.75% | 2 percentage points |

| Higher Rate Taxpayers | 33.75% | 35.75% | 2 percentage points |

| Additional Rate Taxpayers | 39.35% | 39.35% | No change |

Interest earned on income also saw an increase too, so anything above your Personal Savings Allowance (PSA) will be affected.

| Who | Current Rate | New Rate (from April 2026) | Change |

| Basic Rate taxpayers | 20% | 22% | 2 percentage points |

| Higher Rate Taxpayers | 40% | 42% | 2 percentage points |

| Additional Rate Taxpayers | 45% | 47% | 2 percentage points |

Capital gains tax on investment securities and property remains unaffected, though there was a small increase in the tax paid surrounding Business Asset Disposal Relief, though the lifetime allowance remains.

These policy changes will exacerbate fiscal drag, creating greater tax penalties for savings and investments held outside tax-advantaged wrappers like ISAs or pensions. Without wanting to sound like a broken record, but given this new fiscal climate prioritising contributions to ISAs and pensions is fundamental when structuring your finances.

What can you expect from your portfolios?

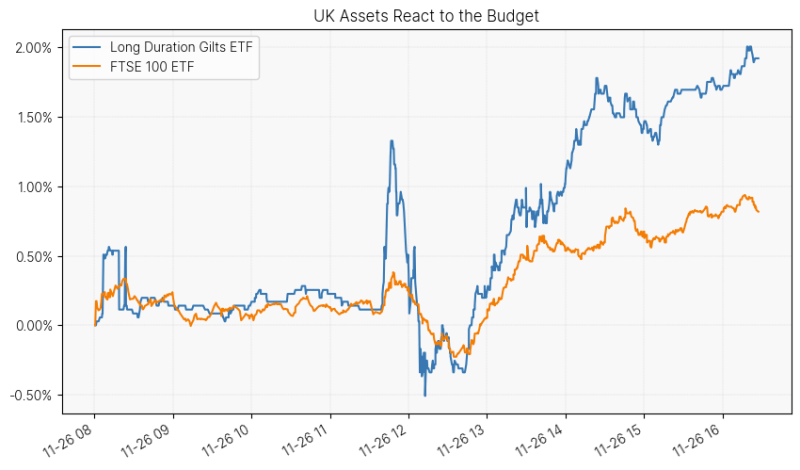

Generally, markets have reacted positively to the Budget. Despite some initial volatility in the bond market, our gilt (UK government bond) exposure is well positioned to contain any negative market movements. We don’t have much duration risk across all risk levels, opting for the shorter end of the yield curve for the most part.

Our longer duration gilt ETF saw some volatility around the leak of the OBR’s forecast, but rallied from that point onwards – and this positivity extended to UK equities too, suggesting the market at least felt relief over the Budget.

This is only an overview of the immediate aftermath, however. Significant questions remain around UK workforce productivity which, set against a backdrop of weaker long-term growth and stickier near-term inflation, suggests the UK outlook may stay subdued and more vulnerable to future shocks.

A delicate balancing act still remains for the Chancellor as she tries to stimulate economic growth and keep inflation under manageable levels. After the expected cut in December, markets are now pricing the next interest rate reduction no earlier than April 2026. This would set the UK apart from the US, where further cuts are anticipated, and from Europe, which has more or less reached its terminal rate.

We still believe in a global diversified strategy across different regions and beyond the scope of the British Isles. We maintain a modest UK exposure in our portfolios, with a far lighter home-country bias than many of our peers.

Whilst the Budget has been recently announced and you all may need time to digest the information, if you do have any questions or would like to have a conversation about how your finances are impacted, please do get in touch with us and we’d be glad to help you through it.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.