In a world that moves fast, retirement often feels like a distant thought until it quickly arrives. You don’t want to be caught unprepared for a potential 20 or 30 years without working. Putting a plan together now is the most effective way to ensure a comfortable future, especially with the tax year end drawing to a close.

According to research by the Pensions and Lifetime Savings Association (PLSA), developed in partnership with Loughborough University, the average single person will need around £31,700 a year in retirement for a moderate lifestyle, while a couple needs £43,900. Yet, many savers find themselves on track to fall short, often because they underestimate how long they’ll live in retirement or delay saving. Starting early can help close that gap and provide peace of mind for later life.

The rising cost of procrastination

We are currently navigating a challenging environment defined by volatility and persistent cost pressures. We’ve all felt the impact of the cost-of-living crisis, which saw inflation soar to 11% in 2022.

On top of rising costs, the tax landscape is getting tougher. The previous Conservative government’s decision to freeze income tax bands until 2028 has already contributed to fiscal drag, and the current Labour government is continuing the policy. This is the subtle process where, as wages and prices rise, more and more people are quietly pulled into higher tax brackets, effectively eroding the purchasing power of your income over time.

This increasing tax burden makes the need to utilise tax-efficient savings vehicles, such as a Self-Invested Personal Pension (SIPP), more critical than ever. The SIPP is one of the most powerful tools available for insulating your savings, providing longevity, and making your retirement planning easier later.

The power of early investment: compounding explained

Time is an investor’s greatest asset, and starting your savings early is the most beneficial action you can take. This is entirely due to the phenomenon of compounding.

Compounding is the idea that your investment will grow not just on your initial capital (the principal), but it will also immediately begin earning returns on the growth itself. This creates a powerful snowball effect where your returns earn returns, leading to exponential growth over time. The longer you delay, the more growth potential you lose.

Despite this, many people delay saving for retirement due to “present bias”, our natural tendency to prioritise immediate needs and pleasures over future benefits. Recognising this bias is the first step in overcoming it; automating regular pension contributions is a great way to stay disciplined and let compounding work in your favour.

The impact of time: a direct comparison

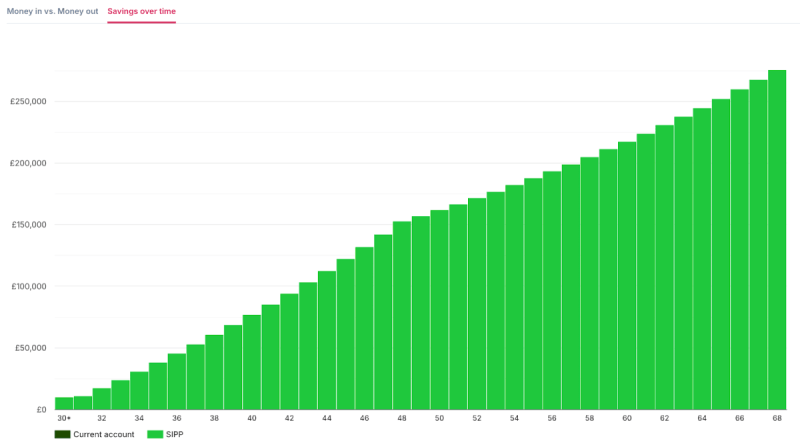

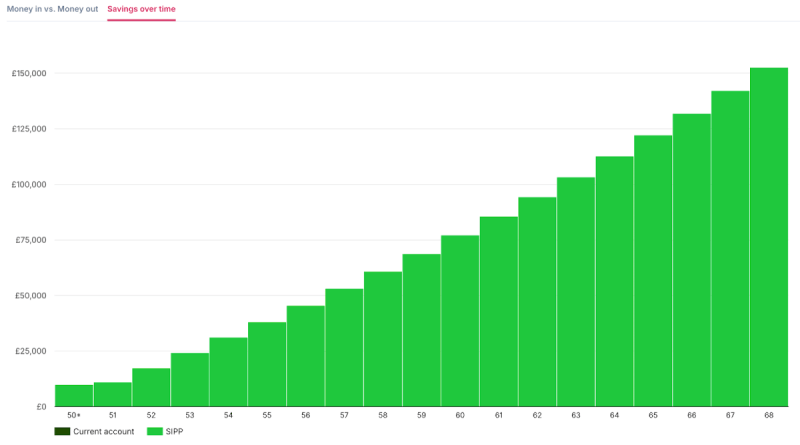

The profound impact of compounding is often overlooked. Let’s compare two scenarios, assuming 5% growth annually for both, with both investors starting with a value of £10,000 and making contributions for the exact same amount of time (18 years), before retiring at age 68:

- Investor A starts making contributions of £500 a month into their SIPP at the age of 30 and stops at age 48. Their money then has 38 years to grow before retirement.

- Investor B waits until the age of 50 to start contributing £500 each month, stopping 18 years later at retirement (age 68). Their money only has 18 years to compound.

While both investors paid in the exact same amount of net contributions (around £108,000), as you can see below the difference in returns is stark:

Investor A:

Investor B:

- Investor A ends up with a SIPP worth around £275,700 at age 68.

- Investor B ends up with a SIPP worth around £152,600 at age 68.

The £123,100 difference shows that the extra 20 years Investor A’s early capital had to compound was significantly more valuable than if they had contributed that capital later in life.

The benefit of consistency

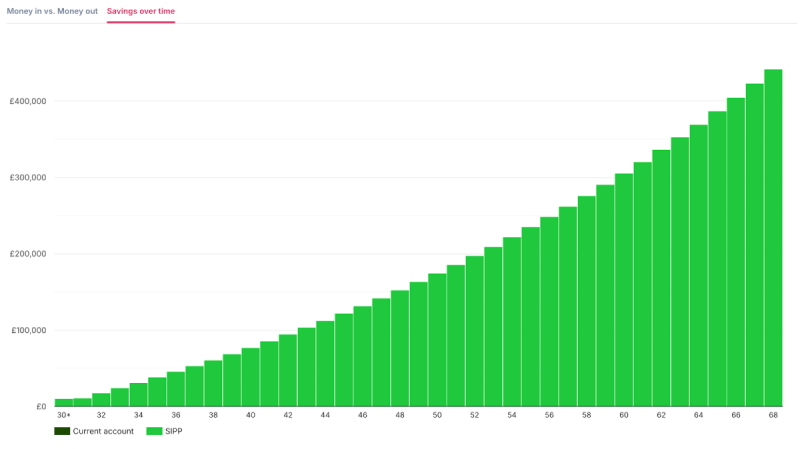

If we look at a third example, Investor C starts contributing £500 a month at age 30 and continues this regular commitment all the way until retirement at age 68. This further illustrates the power of consistency: Investor C’s SIPP would be worth around £441,800 at age 68, proving that putting a plan in place now and contributing regularly significantly increases your savings in retirement through the impact of compounding over the longest possible time horizon.

Investor C:

Why cash is riskier than you think

Now that we’ve discussed the immediate benefits of compounding, you might think you can achieve this effect by simply holding assets in cash. While cash provides security, compounding in cash is a riskier long-term strategy than investing.

The paradox of holding cash is that it almost guarantees the erosion of your money’s purchasing power over time. As we saw during the recent cost-of-living crisis, inflation can be incredibly high. Although current interest rates are better than in previous years, cash traditionally fails to keep pace with inflation over the long run.

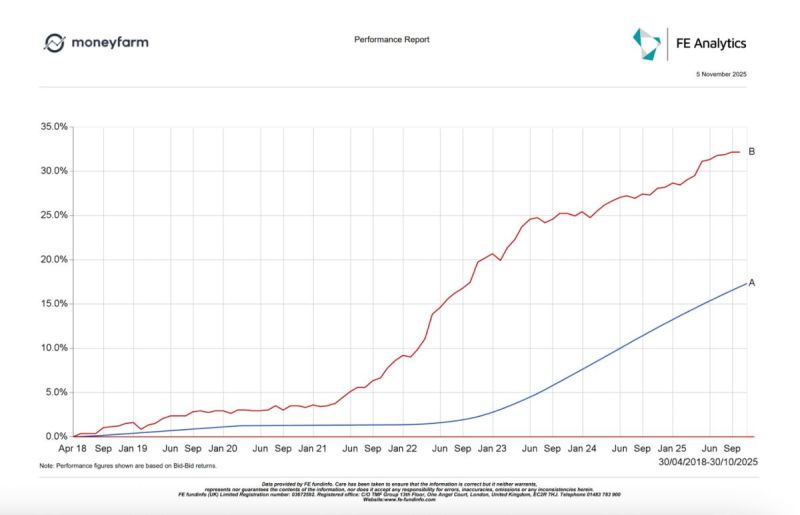

For example, someone who held £10,000 in cash over the last 20 years, with average interest rates around 1.5%, would now have roughly £13,500. However, due to inflation averaging about 2.8% a year, the real purchasing power of that money would have fallen to just over £8,000 – a clear reminder that inflation quietly eats away at cash savings. The chart below illustrates this perfectly: cash (represented by the SONIA interest rate, blue) consistently loses value over time against inflation (CPI, red), confirming that saving in cash over the long run results in a loss of purchasing power.

Building a smarter portfolio for long-term growth

To counter this inevitable loss, investors must adopt a strategy that uses the market rather than avoids it. This requires constructing a diversified portfolio. While historical evidence shows that equities provide the strongest hedge against inflation, bonds can provide income and help smooth volatility, and commodities can act as an additional hedge against rising prices. Proper diversification involves holding a mixture of assets across global geographies and industry sectors to mitigate risk.

Of course, markets don’t rise in a straight line. Short-term volatility is a normal part of investing. However, maintaining a long-term view allows investors to ride out temporary downturns, and diversification helps smooth returns over time. The key is consistency and time, and not trying to time the market.

This comprehensive approach ensures your portfolio is robust, grows your investment over time at a level of volatility that aligns with your individual risk tolerance, and ultimately provides the necessary power to significantly outpace long-term inflation.

Why the SIPP is a crucial tool for retirement savings

Now that we have established that investing early into stocks and shares provides the essential foundation for long-term wealth, we can turn to why the SIPP is one of the most powerful tools in your arsenal.

The immediate financial boost and tax protection

The SIPP offers an instant, compounding boost through tax advantages. Each time you make a personal contribution, you receive an automatic tax relief from the government. As a basic rate taxpayer, every £80 you contribute sees £100 go into your SIPP, making the government’s contribution an instant 25% return on your net outlay. Higher and additional rate taxpayers can claim further relief through their self-assessment.

Furthermore, you can secure additional tax savings if your employer offers salary sacrifice. Under this arrangement, your employer contributes to your SIPP before you pay Income Tax or National Insurance (NI). This reduces your gross salary, often resulting in less NI paid by both you and your employer, ensuring a larger amount is directed toward your pension over the years.

While ISAs are flexible and tax-free, they lack the upfront tax relief and potential employer contributions that make pensions (particularly SIPPs) so effective for long-term saving. Combining the two, however, can provide a balanced approach: ISAs for accessibility and pensions for maximum efficiency.

Protection against fiscal drag and generous allowances

The SIPP is also shielded from political and economic threats to long-term wealth. Any investment growth within your SIPP is completely free from Income Tax and Capital Gains Tax (CGT). This tax-free environment is a vital defence against fiscal drag, the process where frozen tax thresholds push more of your income into higher tax rates as inflation increases. The SIPP effectively takes money out of the part of your income most vulnerable to this extra tax burden.

Finally, the SIPP offers incredibly generous allowances compared to other investment vehicles. While an ISA is limited to £20,000 per year, you can contribute up to £60,000 per tax year (or 100% of your pre-tax income, whichever is lower). If you need to make a larger contribution, you can take advantage of the Carry Forward rule to apply any unused allowances from the previous three tax years, provided you meet certain conditions.

You can utilise Carry Forward if you were a member of a registered pension scheme during the past three years. You must first maximise your £60,000 allowance in the current year, and the total amount you contribute is still limited by the amount of income you have earned in the current tax year.

The SIPP’s combination of instant tax relief, compounding growth, and defence against fiscal drag makes it an indispensable tool for securing your financial future.

The future may feel uncertain, but one thing is clear: time and consistency are your greatest allies. Whether you start small or go big, taking action today helps ensure you’ll have the freedom and financial confidence to live life on your own terms.

If you are unsure where to start, you can book a call with one of our Investment Advisory team for expert guidance on your retirement strategy.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.