For many people in their twenties and thirties, pensions may feel like a distant concern. Not least because you’re a long way off retirement, but also because other financial goals like buying a home, or saving for kids can take priority. Yet the earlier you begin saving, the greater the long-term impact.

The decisions you make today will shape the income you rely on later in life. Time is essential for allowing your investments to grow, and even small contributions made consistently in your twenties or thirties can build into significant sums by the time you stop working.

Most of us have heard of compounding, the process by which returns generate further returns over time, creating a snowball effect. It’s one of the key drivers of long-term growth. What’s sometimes overlooked, though, is that the benefits of compounding usually take a long time to become truly visible. That’s why starting early makes such a difference: it gives your money more time to grow on itself, and it also allows you to spread the effort over many years, reducing the need to put aside large amounts later in life.

Moreover, there are numerous tax-advantages to saving in a pension. Your pensions will benefit from both tax-free investment growth and your contributions benefit from government support through tax relief, so building a pot from a young age gives you the best chance of reaching a comfortable retirement without financial strain. Treating pension contributions as part of your financial routine now makes the goal of lasting financial security far more achievable.

Let’s outline some key reasons why starting your retirement planning early is a good idea.

The incentives are generous

There are several incentives in place for those contributing to a pension. Most employees are automatically enrolled into a workplace pension scheme, where a portion of salary is directed into the pension. These contributions are deducted from pay before income tax, National Insurance (NICs) and student loan repayments are applied. As a result, pension savings benefit from tax relief at the individual’s marginal rate – 20%, 40% or 45%.

For example, if you’re a higher rate tax-payer (40%), and receive a £1,000 bonus, you would take home £600 after Income Tax is paid (and even less after NICs and student loan deductions).

On the other hand, if you sacrificed that into your pension, the full £1,000 would go into the scheme. You’ve just saved yourself £400+.

Beyond that, employers must also make employer contributions to your workplace scheme. Most employers will match your contributions, up to about 4% of your salary, though some are willing to do more. It’s worth making use of these incentives, as almost no other products in the UK offer this level of tax-relief at this scale.

Otherwise, you can also opt to make personal contributions to your pension, whether that’s your workplace pension, or a personal/private pension you’ve set up yourself. The same treatment exists. Your pension contributions will be grossed up by 20% at source (automatically). If you’re eligible for additional tax relief (if you’re a 40% or 45% income tax payer), then you can reclaim an additional 20% or 25% via your self assessment. This is practically the same benefit as you get when you do salary sacrifice, albeit done personally. It’s worth mentioning that personal contributions generate the same level of income tax relief, but do not accrue tax relief on NICs or student loans. Therefore, sacrificing your salary is slightly more efficient than making personal contributions.

Outside of income tax relief, the pension regime also allows for the avoidance of investment-related taxes that would otherwise apply. The money in your pension is treated a bit like an ISA; the capital gains you realise, the dividends you receive, and the income it generates will all roll-up in your pension pot free of tax. You therefore don’t pay any of these taxes on the money that’s in your pension scheme, as is the case with your ISAs.

On top of all that, when you reach retirement you can usually take 25% of your pension tax-free. The remainder is subject to Income Tax at the point of withdrawal. For instance, if your pension is worth £400,000, there’s £100,000 of tax-free cash that you can take – either in one large lump sum, or phased in a series of smaller payments.

For these reasons, the pension regime in the UK is arguably the most tax-efficient investment vehicle available to you. These incentives are in place for a reason.

The state pension isn’t enough

The primary reason the government has created such incentives to contribute to personal and workplace pensions is precisely because the state pension alone is unlikely to be sufficient to live on.

Assuming full eligibility, the current state pension pays £230.25 per week – just under £12,000 a year. Even without a mortgage, most people would struggle to live on £12,000 a year without cutting back their lifestyle.

The state pension is a bit of a controversial political football. For decades, politicians have debated both the age of eligibility and the sustainability of the triple lock — the guarantee that the state pension rises each year by the highest of inflation, average earnings growth, or 2.5%. The broad consensus is that, in its current form, the state pension is becoming unsustainably expensive.

The state pension relies on maintaining – or increasing – the number of workers paying in relative to those drawing from it. With an ageing population, driven by lower birth rates and longer life expectancy, this balance is shifting in an unfavourable direction. While big-picture, long-term solutions are needed for sustainability, the most immediate options are to reduce the pension amount, raise the retirement age – or more likely, a combination of both.

As a result, those currently in their twenties and thirties are likely to receive a smaller state pension in real terms (after inflation) than previous generations, and to access it later in life. This makes it important to build additional savings through workplace and personal pensions.

Private pensions can generally be accessed earlier than the state pension, and under current plans the state pension age will remain 10 years higher than the minimum retirement age for private pensions. Having private pension savings is therefore essential for anyone aiming to retire before 67.

Compounding is key

If you’ve ever seen a chart that plots something growing exponentially, then you’ll be familiar with compounding. Compounding returns can be viewed as a form of exponential growth. In this context, an old tenet comes to mind; “slowly, slowly, then suddenly all at once”.

Compounding returns illustrate the phenomenon whereby the gains you make begin to create their own gains, which continue to create their own gains, and so on and so forth. It’s a concept many are familiar with, yet few have seen play out in their own savings pots – largely because it takes time to become visible.

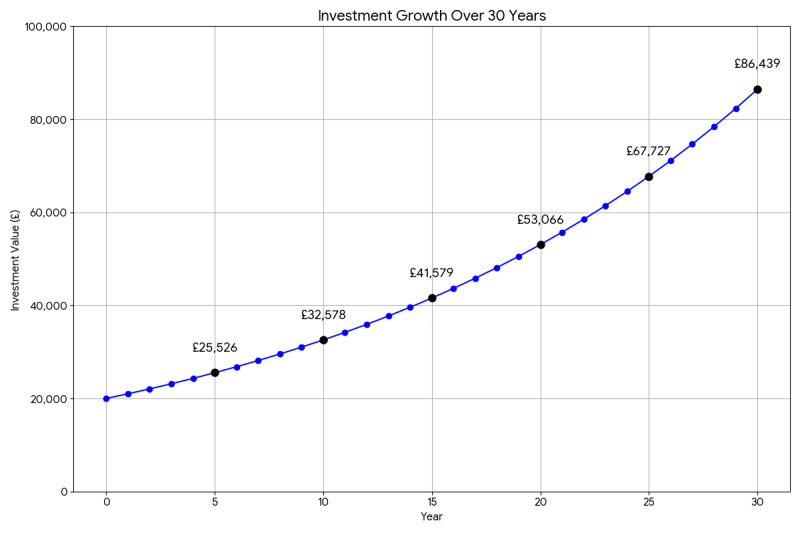

The first chart below plots investment returns, assuming a 5% annual return. The investor starts with a pension worth exactly £20,000. The value of the plot at each five-year interval is displayed on the chart. Growth is gradual in the early years but accelerates sharply as the investment builds, creating a steep upward curve. The investor is generating a consistent return of 5% a year, but each year, generating 5% on a larger starting value. Accordingly, in the first five years, the investor has made £5,526 in profit. In the final five years, the investor makes £18,712. In each year their percentage return has remained consistent, but they benefit from compound growth on a larger capital sum.

What’s clear is that this process takes some time. The yearly profits start very gradually and take a relatively long time before the compounding becomes obvious. The goal is to reach the steeper end of the curve as soon as possible, and the simplest way to do that is by starting early and giving compounding more years to work.

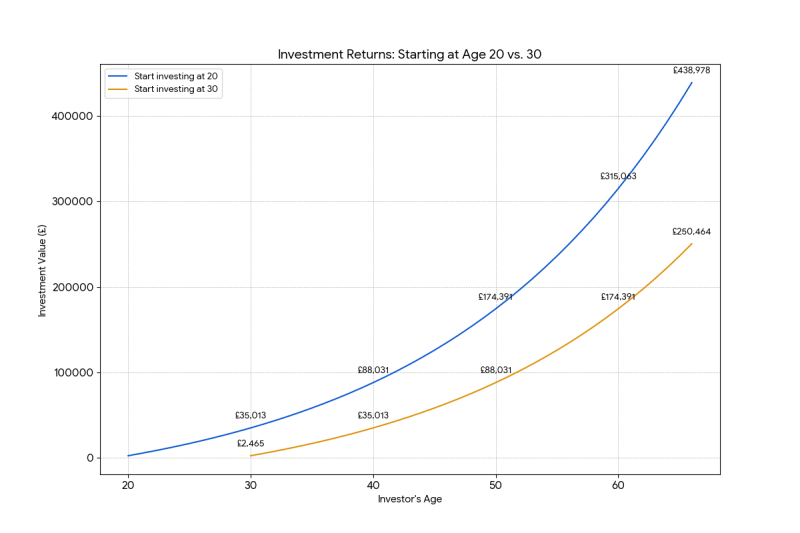

To illustrate this, imagine two scenarios: starting a pension at age 20 versus age 30. In both cases, contributions are £200 per month (£2,400 per year) with an annual return of 5%, continuing until age 66.

What’s visually apparent when looking at a chart like this, is that the divergence (i.e. the difference) between the two lines becomes greater as time goes on. As discussed above, compounding ultimately causes the steepness of this growth curve to grow exponentially sharply over time. Because the two lines continues to diverge, the sooner you can start that effect, the greater its impact will eventually be.

In reality, however, these charts are overly-simplistic. Not many investment products will return a linear rate of return. Instead you are most likely to see a fair bit of variation and volatility over the course of your investment lifecycle, which leads us to our next point.

The longer you have, the more risk you can afford

A core principle of investing and risk management is that the level of risk depends largely on the time horizon. Here, ‘risk’ refers specifically to investment volatility. While every investment carries multiple types of risk beyond the scope of this article, the focus here is solely on volatility.

Simply put, volatility measures the swings – both up and down – in the value of an investment, and is not inherently good or bad. The appropriate level of volatility depends largely on the time horizon. Closer to retirement, stability tends to matter more in planning expenses and income. Earlier in life, particularly when saving into a pension that cannot be accessed for decades, a higher level of volatility can generally be accommodated.

Since higher volatility means greater swings and fluctuations, it creates the potential for both higher gains and sharper losses. Over long periods, accepting some volatility is usually linked with higher average returns, while lower-volatility investments tend to deliver steadier but smaller gains. Given that the funds will not be accessed for decades, sharper short-term losses can, in theory, be overlooked.

The key point is that the earlier pension investing begins, the more volatility can be tolerated – and for a longer period. Assuming global markets trend upward over time, with more positive swings than negative ones, this translates into higher expected returns.

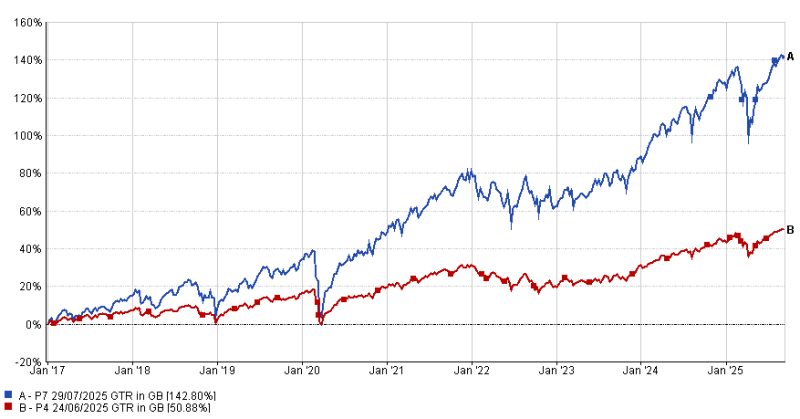

Let’s try and visualise that idea with some historical data. Of course, it must be stressed that historical returns cannot be relied on as a measure of future performance, but it nevertheless gives us a view of a trend, and helps to illustrate a point.

The chart above compares Moneyfarm’s risk level 7 portfolio (P7, in blue) with risk level 4 (P4, in red). P7 is fully invested in global equities, while P4 is split roughly 50% in bonds and 50% in equities.

Typically, an asset allocation like that of the P7 would be taken by someone who is either very adventurous, or who has a long time horizon, or both. As retirement approaches and stability becomes more important, investments are often de-risked gradually, moving toward an allocation similar to P4. Both portfolios follow comparable trends, but the higher-risk option shows greater volatility, with wider swings. Assuming global markets rise on average over the long term, greater volatility can be advantageous, as it offers the potential to capture higher returns.

Risk (volatility) tends to correlate with higher returns over the long term. A longer investment horizon makes it possible to remain in more volatile assets for an extended period, thereby increasing the likelihood of higher returns. This is precisely because time allows greater risk to be taken – and sustained – over the course of the investment journey.

It’s never too early to start planning for your retirement

The pension system is built to reward an early start. Contributions receive tax relief, the savings grow tax-free until withdrawal, and most full-time employees also get money added in by their employer, making workplace schemes especially valuable to stay enrolled in.

The state pension will almost certainly not be enough in and of itself, so having private and personal arrangements in place is key.

Finally, a core rule of investing is that time spent in the markets tends to outperform timing the markets. Starting early is a fantastic way to build a habit, enjoy the long-term returns that it will generate, and prevent the future risks of doing too little, too late.

We appreciate, however, that pensions are a complicated product. They tend to have unique features and rules which can be misunderstood and as a result, often misutilised. Whether you’re unsure about the pension regime, or just want to know more about your options and seek some guidance, let us know. You can speak to our investment consultants by booking an appointment.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.