In recent years, more individuals have been dipping into their pensions earlier than planned. Now more than ever, early pension withdrawals are on the rise. But early pension withdrawals can come with serious long-term consequences.

While accessing your pension early can be the right choice for some, it’s important to understand the risks and consider your long-term needs before making a decision. Here are some of the main factors behind this.

Financial hardship

For many, the rising cost of living, unexpected bills, or debt can feel overwhelming. Cashing out a pension can seem like a quick solution to alleviate these immediate pressures. While it may solve a short-term problem, it often creates a bigger issue down the line: reduced retirement income or having to work much longer than anticipated.

Big purchases

Some individuals see their pension as a fund for a significant purchase, such as a new car, home improvements, or even a dream holiday. While tempting, dipping into your pension early can potentially affect your long-term financial security and lifestyle.

Lack of financial guidance

Some people cash out simply because they don’t know their options. Without clear guidance it’s easy to see the pension as a windfall rather than a safeguard. Speaking with your pension adviser, even for a short consultation, can make a major difference in understanding the consequences and exploring alternatives like loans or partial withdrawals.

Reasons why people regret it

Around one in 10 retirees (8%) aged 55 or older who had taken money from their pension pot before reaching State Pension age regret it, according to research by Just Retirement.

Nearly half (49%) of this group chose not to get advice or guidance before accessing their pension. Only 27% spoke to a regulated financial adviser before withdrawing money from their pension. The findings come from research by the Just Group, carried out by Opinium, and based on 1,050 retirees.

Almost a third (32%) of this group say they needed the income to bridge the gap to State Pension age or because of redundancy or lower earnings. More than half (52%) had retired sooner than expected.

But while the idea of having a lump sum of money today may sound appealing, many people later find themselves regretting the decision.

Running out of money in retirement

The most significant regret is often the realisation that the money withdrawn was intended to provide an income throughout retirement. By taking it early, you could dramatically reduce your future financial security, potentially facing poverty in later life or having to work far longer than anticipated.

Emotional and psychological toll

What seems like a good idea in a financial pinch can later feel like a mistake. Many retirees report stress, regret, and anxiety when they realise they don’t have enough saved to support their lifestyle. The emotional toll can be heavy, especially if they’re unable to go back to work.

Impact on future contributions

Accessing your pension early can trigger the Money Purchase Annual Allowance (MPAA). This is a reduced annual contribution limit, currently £10,000. Once triggered, it replaces the standard annual allowance, which is up to £60,000 or 100% of your earnings, whichever is lower. This significantly restricts how much you can contribute each year with tax relief. As a result, rebuilding your retirement savings becomes much more difficult if you continue working and want to make future contributions.

Losing compound growth

One of the biggest advantages of a pension or retirement account is compound growth.The longer you keep your money invested, the more chances it has to grow – not only on what you put in, but also on the returns it earns over time. This compounding effect could significantly increase the value of your portfolio. Withdrawing funds early not only reduces your immediate balance, but also interrupts this growth process, potentially limiting your long-term wealth and resulting in a substantial reduction in future returns.

The way forward

Pensions are designed to provide steady income in retirement. Tapping into them early can mean significantly less money when you need it most – when you’re older and possibly no longer able to work. However, with a little bit of forward planning and by speaking to a pension adviser, you can make the most of your pension and help pave the way to a brighter retirement.

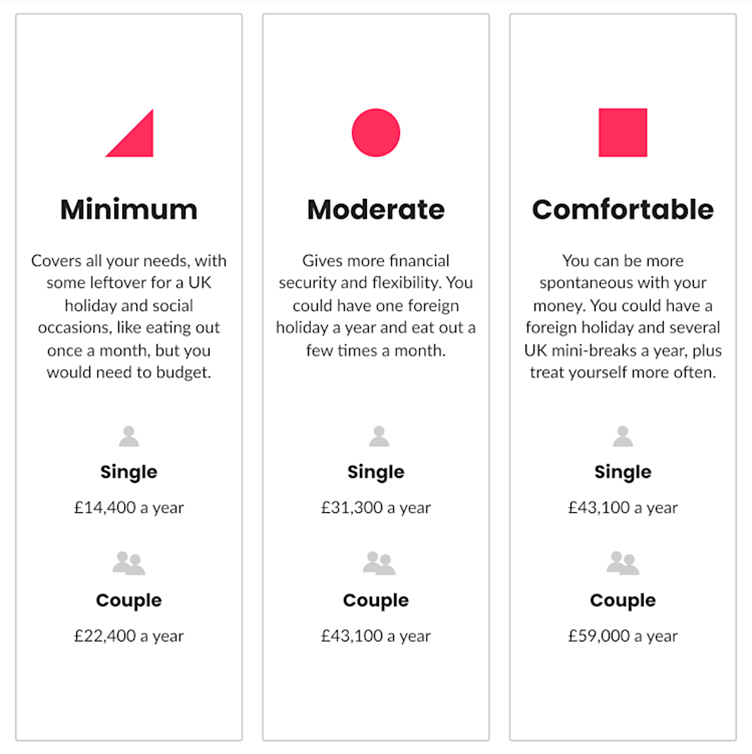

What income do I need in retirement?

The Pensions and Lifetime Savings Association (PLSA) have released the Retirement Living Standards, showing how much income you’d need in retirement. This is split into minimum, moderate and comfortable lifestyles for single people or for couples.

There has been a 38% increase in the amount you’d need per year for a moderate income in retirement, compared to the figure from last year (2022/23). This means we may all need to save more to make sure we have the lifestyle we want in the future.

These figures are a good place to start when you’re working out when you could afford to retire and how big your pension pot will need to be. You can then work out just how much you should be contributing to your pension each month. And remember, your pension adviser is always here to help you work out what you could have and how much you should be paying in now to make your retirement goals a reality.

Retirement planning in five easy steps

- Work out how much income you’ll need in retirement. This includes essentials like housing and bills, but also fun things to do like holidays, shopping and eating out.

- How much income are you on track to have in retirement? Check your State Pension forecast on GOV.UK, combine your old pensions into one plan and use our pension calculator to work out the size of your pension pot and how much income you could have in retirement.

- Look at when and how you can access your pension. You can start drawdown with defined contributions pensions from age 55 (rising to 57 in 2028) and the State Pension age is currently 67. When you can retire will depend on your pension pot, whether you are a couple or single and the income you need in retirement.

- Start your retirement plan. Based on all the things above, you should be able to work out if your pension is on track, if you can retire at the age you want or if you need to reassess your pension, contributions or retirement age to make it work.

- Next steps: Once you have worked out your retirement plan (or if you’ve realised you need some extra help with retirement planning), our expert Pension Advisers can help you reach your goals and guide you towards a brighter financial future.

You can trust us with your retirement planning

At Moneyfarm, we believe everyone deserves a comfortable and fulfilling retirement, and we’re here to help you achieve it. Here’s what you’ll benefit from with us.

- A personalised pension plan and ongoing service to keep your pension in the right place for you, even when you’ve retired.

- Find, check & transfer service to help you find and combine any old or lost pensions into one place, to make planning for retirement easier and to get a better picture of your total pension savings. We charge a one-off 1% fee for our pension consolidation service, which covers the process of finding and combining your pensions into one. This fee is deducted from your pension when the transfer is completed — there’s nothing to pay upfront.

- You can see your estimated sustainable annual or monthly drawdown income in your account in real time.

- Your money will remain invested during your retirement to benefit from potential further growth.

- Your pension adviser will be available to talk to whenever you need to.

- Arrange withdrawals from your pension through your online account or over the phone with your adviser.

Let’s make sure you’re on track

Are you confident you’re saving enough or wondering if you can retire when you want to? Don’t wait and risk missing out on a secure future.

We’re here to help you understand where you stand and what simple changes can make a big difference. Taking action now means you’re in control of your retirement journey.

Taking money from your pension early can significantly reduce your income in retirement. You may also pay more tax or lose out on future investment growth. Always seek advice before making any decisions.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.