The tax year end is fast approaching, and that’s got us all thinking about how we can best position ourselves – and our children – financially for the future.

We all live busy lives, and so putting additional funds aside to save for your kids’ future can often be an afterthought. But with time on their side, they are in the best position to reap the rewards of investing.

By putting a simple plan in place, you can set them up with a vital head start. Whether it’s helping with university costs, getting a foot on the property ladder, or simply providing a safety net, investing early can make all the difference.

So how can this be done? We’ve all heard about saving in an interest bearing cash account, though if you’re looking for more compelling returns over the long term, you may like to consider a Stocks & Shares Junior ISA (S&S JISA).

What is a Junior ISA (JISA)?

Introduced in 2011, the JISA replaced the Child Trust Fund (CTF) as the primary tax-free saving and investing vehicle for children. Only a parent or guardian can open a JISA for their child, though anyone (including friends and other relatives) can chip in. Each year up to £9,000 can be contributed, and this allowance resets at the end of the financial year (April 5th).

A JISA grows completely tax-free – meaning no tax to pay on gains, dividends, or interest earned. This presents an excellent opportunity to compound the growth of the investment over time.

Once invested, funds cannot be accessed by the child until they turn 18. At that point, funds are transferred into a regular ISA in their name and can be withdrawn if need be.

So not only does a JISA give your child a financial head start, but it also fosters early investment habits that can benefit them for life. The greatest power of the JISA comes from having a long time in the market, with investment returns compounding over that time.

The magic of compounding, or the snowball effect

Compounding is the process of your investment returns generating even greater returns over time. In other words, your money doesn’t just grow, it accelerates. Each contribution generates its own returns, which then generate further returns – creating a powerful snowball effect of growth. This is why your earliest contributions are often the most impactful.

Whether you’re investing in a JISA, pension, or Stocks & Shares ISA, time is your most valuable asset. And when it comes to those with the longest investment horizons – your children – starting early can make a life-changing difference.

The benefit of starting early

With that in mind, let’s consider an example to visualise the importance of starting early with a simple investment plan.

Imagine that today is your child’s 18th birthday. You’ve been investing for them on a monthly basis into a global equity index fund like the FTSE All-World; a broad measure of global equity market performance.

We will compare 2 different scenarios. In each, you will have contributed the same amount overall, but started at different times (one earlier and one later). As you will see, time in the market makes all the difference.

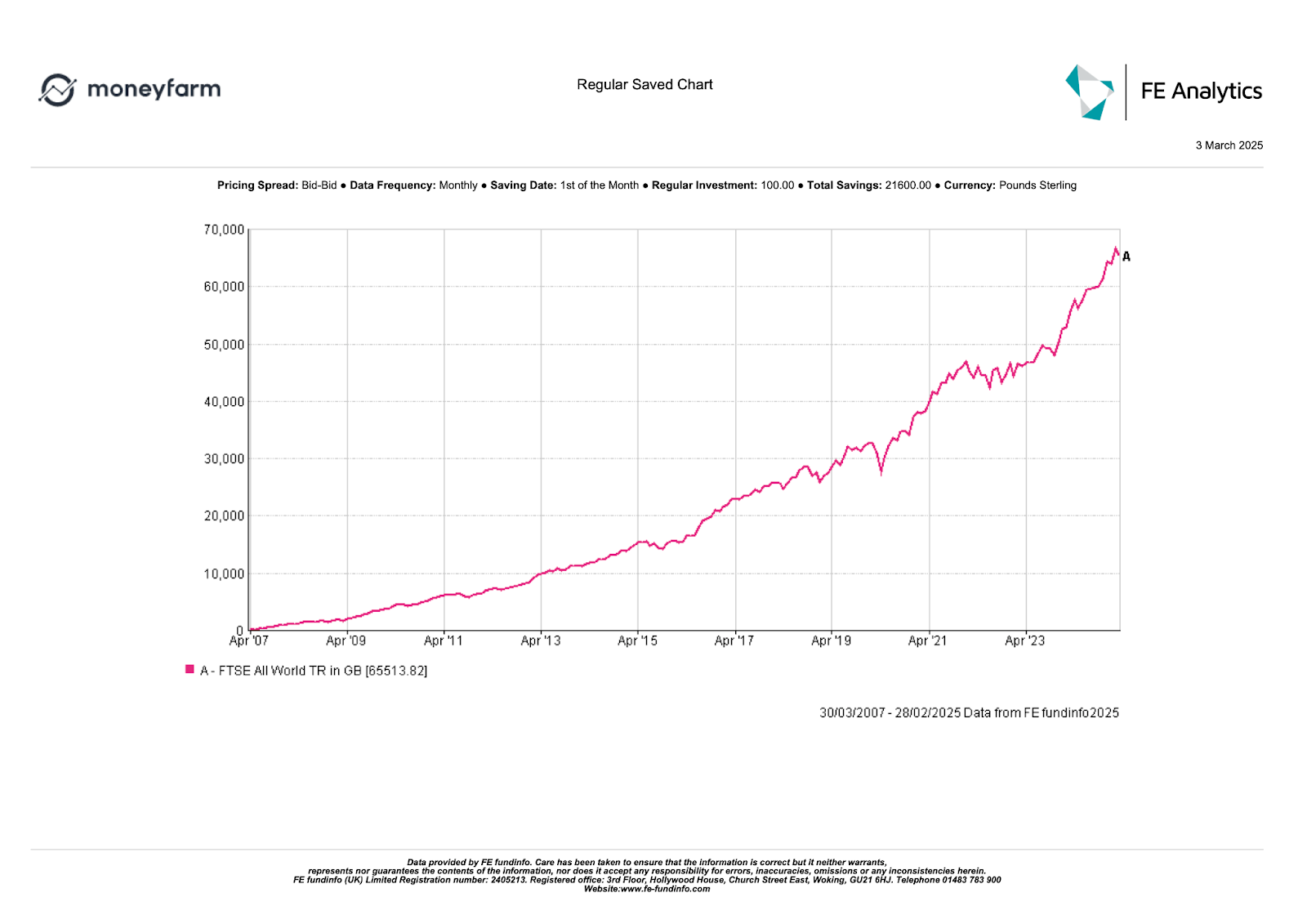

Scenario 1: starting early

· You have been investing £100 per month from birth

· Over 18 years, you invest £21,600

· By their 18th birthday, the account would be worth over £65,000 – experiencing exponential growth

Source: Moneyfarm Analysis, Data Source: FE Analytics

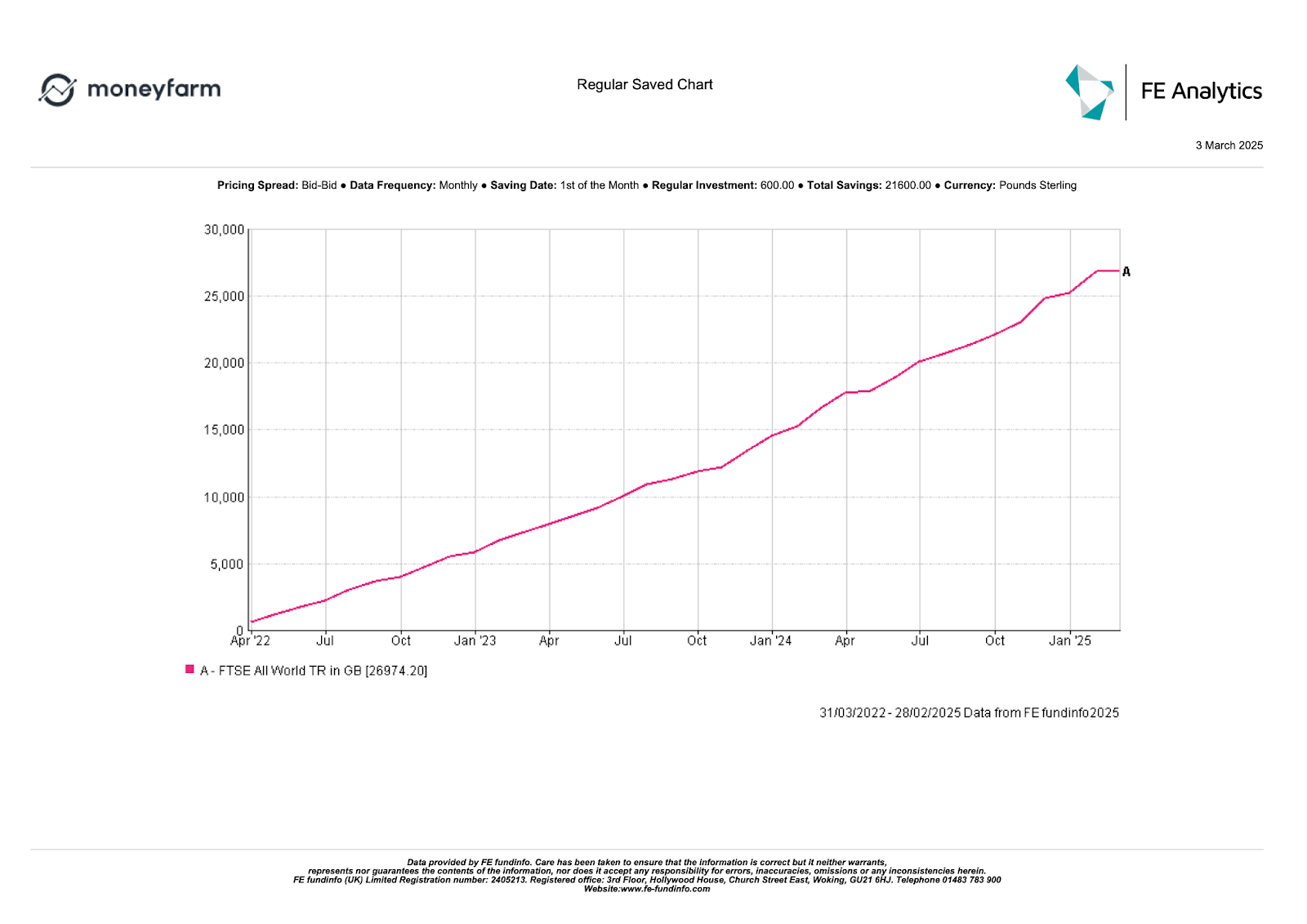

Scenario 2: starting later

· You wait until your child turns 15, then start investing £600 per month

· The total contribution is still £21,600 over a condensed 3 year period

· By their 18th birthday, the account would be worth just under £27,000 – with much flatter growth

Source: Moneyfarm Analysis, Data Source: FE Analytics

The result

By simply starting earlier, you would have experienced over £38,000 in additional growth, all while making the same total contribution overall. That’s the power of compounding in action.

| Starting age | Investment per month | Total Invested | Value at age 18 | Growth |

| 0 | £100 | £21,600 | £65,513 | £43,913 |

| 15 | £600 | £21,600 | £26,974 | £5,374 |

Source: Moneyfarm Analysis, Data Source: FE Analytics

What’s more, the later you start investing, the less time you have to ride out market fluctuations and therefore the more cautious you’re likely to be. So while the FTSE All-World has performed well over the past 3 years, if you only start investing when the child is 15, you might choose a more risk averse, lower-growth portfolio. This further strengthens the case for starting earlier.

Starting earlier also allows you to build up the investment pot more slowly over time, ensuring that each contribution is a more manageable amount. Putting away £100 each month for instance (or £1,200 per year) is a lot easier than finding £600 to invest each month (or £7,200 per year).

What about Child Trust Funds (CTF’s)?

The CTF scheme closed in 2011 and was replaced by the JISA. You cannot have both, though a CTF can easily be transferred into a JISA with Moneyfarm.

Not sure if you have one? You’re not alone. Approximately £1.4 billion is held in unclaimed CTF’s across the UK, with an estimated 670,000 young adults unaware they even have one (source). So if you’re unsure whether you have a CTF, you can use HMRC’s free tool to track it down.

Investing with Moneyfarm

At Moneyfarm, we take the guess work out of investing for your child’s future in a S&S JISA by making all the investment decisions, so you don’t have to.

It’s never too late to start either. As the old saying goes, “the best time to plant a tree was 10 years ago. The second-best time is now”.

Be aware that there is a hard deadline for JISA contributions in this financial year of April 5th and the £9,000 allowance does not roll over.

If you have other investments with us too, you may benefit from a cheaper management fee by adding to a Moneyfarm JISA. This is because the rate you’re charged is based on the total assets across all portfolios (in the same management style).

The benefits of compounding are not restricted to JISA’s either. We also offer pensions, Stocks & Shares ISAs, Cash ISAs and General Investment Accounts as a comprehensive solution for you and your family.

Our team of dedicated investment consultants are here to help every step of the way. Please book an appointment so that we can help you get set up with a JISA and talk through your investment options.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.