The period leading up to retirement can often represent a crucial phase for many – a time to reflect on decades of hard work, plan for any desired activities or hobbies, and devise an effective strategy to achieve a financially sound retirement.

As a total wealth partner, we understand the importance of this life stage, as well as the challenges it may bring. This article is intended to present an overview of your pension choices and their nuances, while providing you with the tools to achieve a solid and sustainable retirement strategy.

An overview of your pension choices

In the UK, there are three main types of pensions, each with their own features. Reflecting on which of the below you hold (or are eligible for) might be a great starting point as they can often act synergistically by complementing one another.

The state pension

The state pension is paid by the government based on National Insurance Contributions (NICs).

Eligibility typically requires a minimum of 10 years of NICs (for a partial pension amount), and 35 years of NICs for the full amount. While this provides a guaranteed income for life, increases to the State Pension age (rising to 67 by 2028) and shifts in demographic factors such as increased life expectancy may pose challenges regarding its long-term sustainability.

In turn, this may suggest a need to seek supplementary solutions to ensure an adequate level of retirement income. Knowing how much you are entitled to could add peace of mind when approaching retirement. You can check your state pension forecast directly on the GOV.UK website.

Occupational pensions

Occupational pensions are provided by your employer, with many individuals often having several pots resulting from various jobs during their working life. These can include the following.

- Defined Benefit (DB) Schemes: often known as ‘Final Salary’ pensions, they provide a guaranteed income based on salary and years of service. Access to DB schemes tends to follow the State Pension age, though this may vary. Notably, while these can still be found in the public sector (e.g. NHS, Teachers, Army etc.), they are becoming increasingly rare in the private sector.

- Defined Contribution (DC) Schemes: here both you and the employer contribute to a pension pot which is then invested, giving you control over where it’s invested and how you draw down. Its value depends on the level of contributions, the underlying investment performance, as well as any management fees incurred throughout. Access to DC schemes tends to coincide with the Normal Minimum Pension Age (NMPA), currently 55 and rising to 57 from April 2028.

Self-Invested Personal Pensions (SIPPs)

SIPPs are DC schemes set up privately, which can be held alongside any of the above and often provide greater investment options.

A major benefit of SIPPs – which also generally applies to all DC schemes, occupational or otherwise – is the tax relief on contributions, ranging from 20% for basic-rate taxpayers to 40% and even 45% for higher and additional-rate taxpayers.

Examples of smart DC contribution strategies

At the time of writing this article, the maximum you can contribute to a pension while receiving tax relief equals the lower amount between £60,000 and your taxable earnings. For example, if you earn £80,000 the annual allowance is capped at £60,000, and if you earn £40,000 this will be the maximum you can contribute.

Prioritising pension contributions ahead of retirement could be especially appealing for those in a higher/additional tax bracket. The below example illustrates what this may translate to.

In employment

- Higher-rate taxpayer (up to 40% income tax) invests in their SIPP.

- Their contribution is initially subject to a 20% tax relief within the SIPP.

- A further 20% could be claimed from HMRC (via self assessment) on the portion of their income which was taxed at 40%.

- This results in an overall tax saving and a boosted pension portfolio.

In retirement

- Up to 25% of the SIPP’s value can be typically taken as a tax-free lump sum. This is known as Pension Commencement Lump Sum (PCLS).

- The remaining 75% is then taxed as income at your marginal rate. With individuals generally spending less during retirement, this leads to less income being required, which in turn will decrease the associated income tax amount as part of drawdown.

- The initial contributions made during employment would have continued growing in the background up until when you decide to draw an income

Moreover, a valuable, yet often overlooked strategy entails leveraging the carry forward rules to maximise your annual allowance. This allows you to tap into unused allowances from the previous three tax years, whilst still receiving tax relief. Some key conditions must be met however: you must have been a member of a registered pension scheme in each of the tax years from which you wish to carry forward unused allowance and the total value of your contributions (including what you wish to carry forward) must have been earned in the current tax year, amongst others.

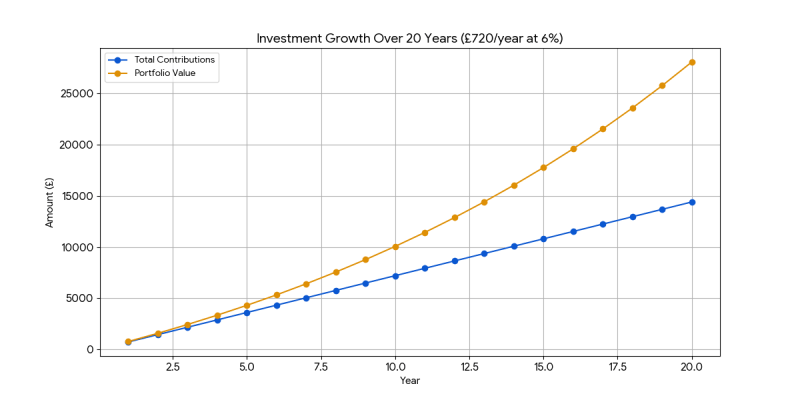

Another valuable strategy is to continue contributing to your pension after you stop working. Even in the absence of relevant UK earnings, you can still contribute up to £2,880 p.a. and receive 20% tax relief from the government (£720), bringing the total contribution to £3,600.

For illustrative purposes, assuming a regular contribution of £2,880 between the ages 55-75, and an average yearly growth rate of 6%, the extra tax relief could account for an additional £26,485.63 (as shown below). Notably, from the age of 75 any new contributions will cease receiving tax relief.

A pragmatic plan for drawing your retirement income

Having a clear accumulation strategy during your working life is just as important as having an effective decumulation strategy. This ensures that your funds will continue growing sufficiently throughout your lifetime, especially when accounting for the effect of inflation.

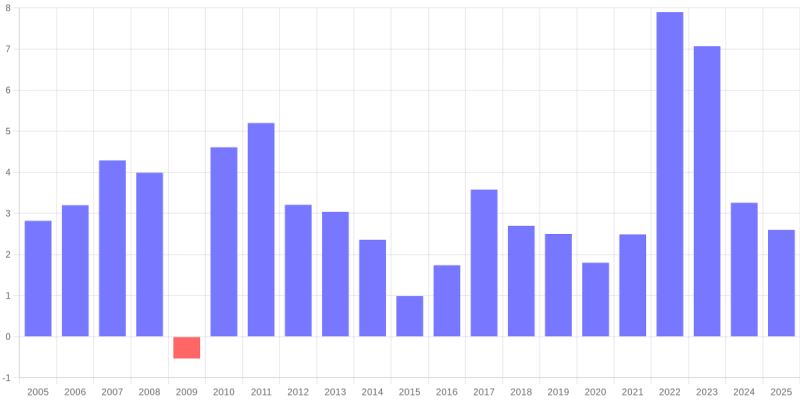

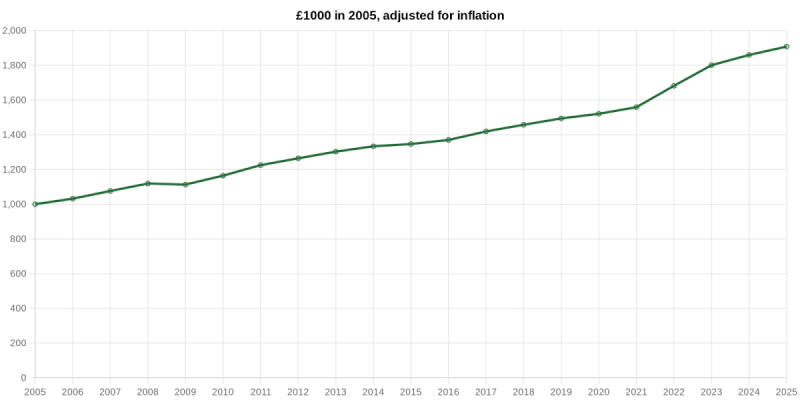

Indeed, when looking at extended periods of time, the erosion of purchasing power is not to be underestimated. The below charts outline UK inflation rates over the past 20 years, and a calculation of buying power equivalence. Acquiring £1,000 worth of goods in 2005 would require £1,908.20 in 2025, meaning that the “real value” of each pound decreases over time.

GBP inflation since 2005

Annual Rate, the Office for National Statistics CPI (Consumer Price Index)

A pragmatic drawdown plan including multiple pensions could look as follows.

- The State Pension and DB pots could form the bedrock of your strategy

These constitute a reliable income stream, as their value does not fluctuate based on investment performance. These might be especially helpful during periods of market volatility by providing income stability.

- Maximising the flexibility of DC pots

Following the introduction of Pension Freedoms in 2015, accessing DC pensions has become more flexible. The most popular options include taking advantage of the 25% PCLS (tax-free cash) to fund all sorts of objectives, including additional investment in tax efficient wrappers (e.g. ISAs). The remaining 75% (taxable portion) remains invested and continues growing over time. Based on whether you have additional sources of income, making regular withdrawals can be structured each year in such a way to maximise your standard Personal Allowance, currently £12,570 (2025/26).

Given the above-mentioned degree of flexibility, reflecting on when you would like to begin drawing down may help mitigate the so-called “Sequencing risk” – taking an income from your investments during periods of unfavourable market conditions. As you transition from the accumulation phase to the decumulation phase, selling investments during a market downturn could place pressure on the remaining capital to cover any shortfall – thus possibly having long-term financial impact. Having access to external cash reserves, such as an emergency fund, could reduce the effect of “Sequencing risk” on your retirement portfolio.

- Live, Enjoy, Review, Repeat

After creating a clear and efficient plan, it’s now time to embrace the fruits of your labour. Equally, retirement planning shall not be seen as a static concept but rather as a reiterative process. As we progress in life, our circumstances may vary, in turn bringing a new set of financial needs. Continuous monitoring is a key component, as it helps apply necessary tweaks to ensure you can enjoy retirement as you have always dreamed of.

Making the most of your contributions

Whether you have been investing for decades or are just getting started, your fifties represent a crucial period. For many, this is a phase of greater earning potential.

However, with nearly 40% of Brits set to struggle meeting basic financial needs in retirement, and with the average cost of residential care being £67,132 p.a., avoiding the risk of running out of money might be an aspect worth exploring in detail. This is referred to as longevity risk, resulting from members of the population living longer, thereby requiring greater levels of funding than anticipated in order to sustain ongoing living costs.

Making the most of your contributions while still in employment may significantly boost your pension savings. Indeed, once you cease working, your pension allowance is significantly reduced, with only ISAs being left as tax-free vehicles. This may be especially appealing as a higher or additional-tax payer, given the substantial amount of tax relief that takes place as a result of pension contributions.

We are proud to support you during every stage of your life. Through our robust investment solutions, we specialise in offering exceptional client service and professional financial guidance to help you achieve your holistic financial aspirations.

If you’d like personalised guidance, you can book a free appointment with our experts to talk through your financial situation.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.