Planning for retirement can feel daunting, but a well-structured pension strategy can turn uncertainty into long-term financial security. Early preparation, smart asset allocation, consistent contributions, and regular reviews are key factors of a retirement plan that works. The good news is that most people already have some provisions in place. The key now is to take control of the available options and make them work effectively.

Step 1: Assess current provisions

The first step is understanding what is already in place.

In the UK, employees over the age of 22 earning more than £10,000 per year are automatically enrolled into a workplace pension scheme. A minimum of 8% of qualifying earnings must be contributed annually, split between the employee, the employer, and Government tax relief.

While this is a solid start, many experts caution that minimum contributions alone may not be enough to maintain the current lifestyle in retirement.

One of the most important steps is simply keeping track of pensions. The Pensions Policy Institute estimates that more than £31 billion of pension savings are currently “lost” in the UK, often because people forget about old workplace pensions when they change jobs.

When changing employers, pensions remain with the previous provider unless specifically transferred. It is important to record where each pension is held, including policy numbers and provider names. If details are missing, support can be obtained from HR departments, past payslips, or the government’s Pension Tracing Service.

If that fails, we offer a service called Find, Check and Transfer which can track down lost pensions. Only the employer’s details, dates of employment, and workplace location are required.

Consolidating old workplace pensions into one single pension is an effective strategy to keep track of pension pots. This can also reduce paperwork and admin, and potentially lower fees.

Step 2: Understand the investment mix

Knowing how money is invested is just as important as knowing where it is. Academic research suggests that asset allocation drives roughly 90% of long-term portfolio returns, making it a critical decision.

Many workplace schemes offer a default, ‘one-size-fits-all’ investment approach that is not tailored or reflective of a person’s individual circumstances and goals. This can lead to underperformance or unsuitable investments. Reviewing fund choices and adjusting them to match specific objectives ensures the portfolio truly reflects the intended plan.

With more than 10–15 years until retirement, greater risk can typically be taken through a higher allocation to equities (shares), which have historically offered stronger growth potential, although past performance is not an indicator of future results.

As retirement approaches, allocations can gradually shift towards bonds, cash, and other lower-risk assets to protect capital.

A recommendation is then made on the most suitable managed portfolios, aligned with specific objectives, to ensure funds are invested effectively to meet retirement goals.

Step 3: Review contributions & maximise tax advantages

Once pensions and investments are clear, the next step is to assess how much is being contributed.

Many studies have shown that the statutory 8% minimum pension contribution is unlikely to provide sufficient income in retirement to sustain living standards. Increasing your contributions, even by a small amount, can significantly boost savings thanks to compounding, the snowball effect of earning returns on past returns. The earlier the start, the greater the impact.

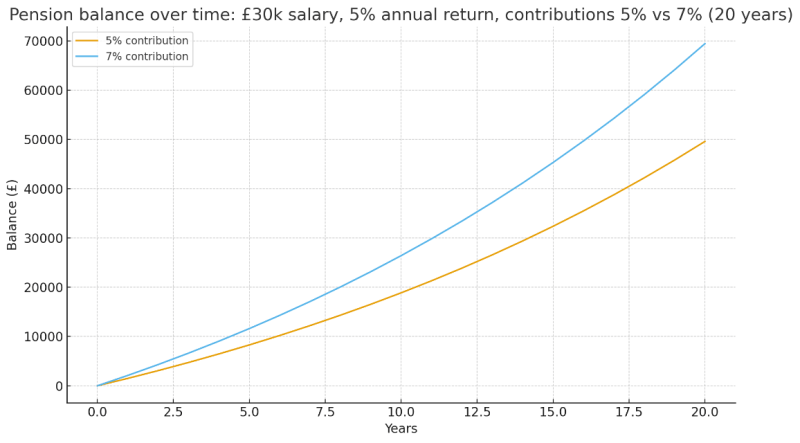

For example, someone earning £30,000 who increases their contribution from 5% to 7% would, over 20 years and assuming 5% annual growth, add an extra £20,832 to their pot – all from just £50 more per month.

Importantly, some employers match contributions above the minimum, so it is worth understanding if the employer pension has any additional benefits, and how to maximise this benefit.

Pension contributions benefit from automatic tax relief.

- Basic-rate taxpayers receive 20% tax relief automatically.

- Higher-rate and additional rate taxpayers can claim back an additional 20% or 25% via self-assessment.

Self-employed individuals can open a personal pension or SIPP and still receive tax relief. Business owners may benefit from making employer contributions directly from the company, which can also be tax-efficient.

Step 4: Forecast & adjust

Once pensions, investment mix, and regular contributions have been assessed, it is useful to forecast whether they will provide the desired retirement, both in terms of timing and expected income.

At a basic level, there are many online calculators that can project future outcomes based on contribution levels and assumed growth – one is available here on our website.

At a more detailed level, our Guidance+ service provides an in-depth review of retirement plans based on current provisions. It highlights whether goals are on track or if a shortfall exists. In case of a gap, possible measures include:

- Increasing contributions

- Delaying retirement

- Adjusting lifestyle expectations

- Taking more investment risk (where appropriate)

Step 5: Review regularly

A pension strategy should evolve with life circumstances. Marriage, children, job changes, or windfalls can all have an impact. Pensions should be reviewed at least once a year, checking:

- Investment performance

- Contribution levels

- Whether the portfolio needs rebalancing

Staying engaged ensures the plan keeps pace with retirement goals.

Conclusion

A successful pension strategy is not just about saving, it’s about staying engaged, reviewing regularly, and adapting to life’s changes.

By consolidating where appropriate, optimising asset allocation, maximising contributions, and forecasting retirement needs, it is possible to build a plan that adapts over time. The earlier the start, the more powerful compounding becomes, but it is never too late to begin.

A well-crafted pension plan is one of the best gifts for the future: peace of mind, independence, and the freedom to enjoy a retirement built through years of work.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.