If your only source of news was the US equity market, what would you think? Well, given that the market is basically at an all-time high, you’d think that the world was in pretty good shape. No hint of US$100 per barrel oil, no suggestion of rising inflation and higher bond yields.

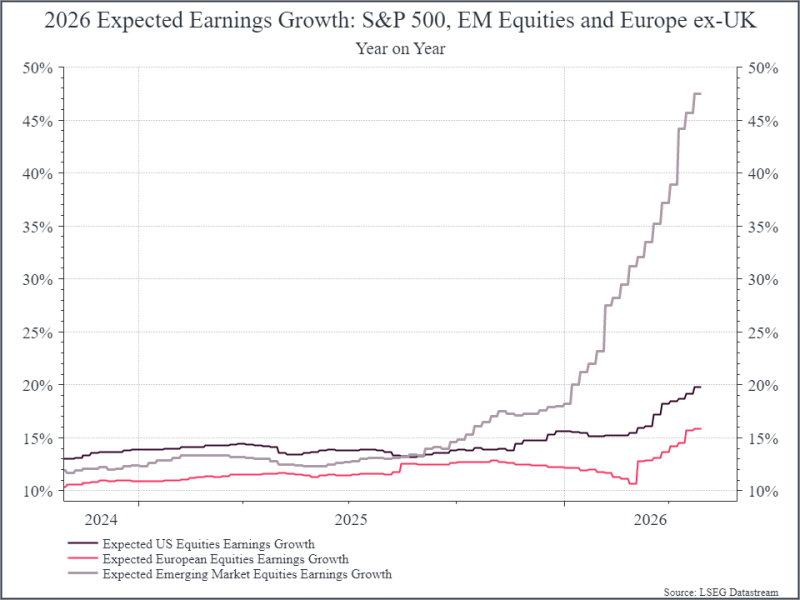

So what’s going on? We think there are a few drivers, but strong corporate earnings are an important part of the answer. The chart below shows expected earnings growth for equities in the US, Europe and Emerging Markets in 2026 – and how those forecasts have changed over time. We can see that across the three regions, earnings growth is robust and has been drifting higher, even in the wake of the Middle East conflict.

Looking at the most recent data, first quarter earnings from US companies have generally been pretty strong. The percentage of companies beating expectations is higher than in the past. As always, we are seeing some differentiation. Tech and energy businesses are generally doing better. The big tech companies still see strong demand related to Artificial intelligence.

Overall, investors have been optimistic about the outlook, although there are still concerns about the level of investment spending. Energy companies’ earnings are benefiting from higher oil prices as you might expect. Outside of those two sectors, the results are a little more mixed, suggesting that some consumer facing businesses are seeing an impact. Nonetheless, the overall message has been that corporate earnings growth remains resilient.

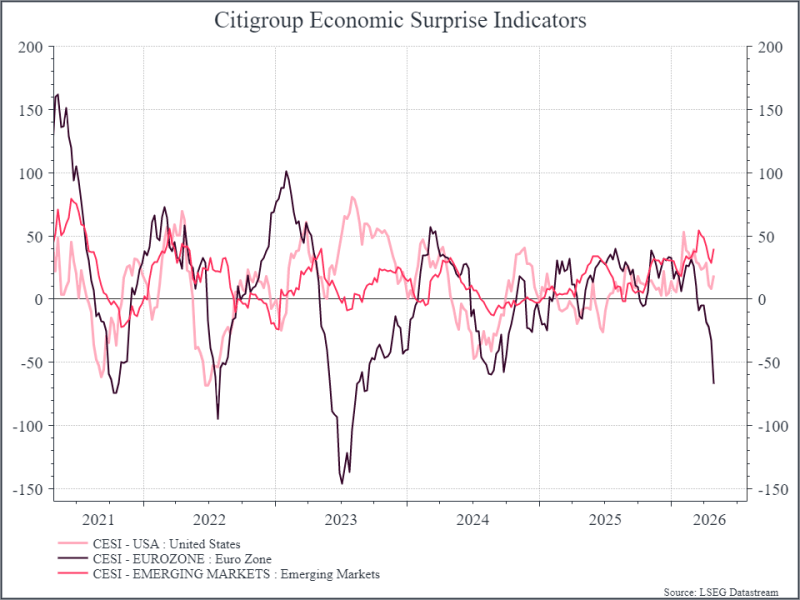

Looking at the macro data, we can see relative stability in the US so far. The chart below shows economic surprise indices. These basically track macro data releases compared to economists forecasts. So far, since the start of the conflict, the macro releases from the US and Emerging Markets have been largely as expected, whereas we’ve seen weaker numbers start to come through from the Eurozone.

It’s never as simple as saying that domestic macro results should translate into corporate earnings, particularly since European companies often operate globally. But if we see persistently weaker macro data, we’d expect that to impact on corporate earnings.

Where does that get us? Strong earnings growth has helped underpin the equity recovery in April, particularly in the US. A lot of that depends on the technology sector, and so far, the large tech businesses have been delivering. Those earnings drivers could be at least partly insulated from the macro impact of higher oil prices, although other sectors will likely feel the effects. For now, we think there’s a risk that European earnings forecasts could weaken a bit in the coming months. But the longer high energy prices persist, the greater the chance that earnings estimates come down more broadly.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.