As we do every month, our Senior Portfolio Manager and Head of Research, Roberto Rossignoli, takes stock of the cryptocurrency market. The spotlight is on Bitcoin’s performance, which has reached 20 million mined units, marking a crucial step towards its maximum programmed scarcity, and on significant regulatory and institutional developments.

March was largely driven by macro developments linked to the Middle East war. The Iran conflict, and the grip on the Strait of Hormuz pushed Brent crude toward $116 per barrel and compressed risk appetite across every asset class.

On March 18, the Federal Reserve – through the FOMC (Federal Open Market Committee), the body responsible for setting US interest rates – decided to keep rates unchanged at 3.5%–3.75%.

However, the overall tone was more hawkish than expected: policymakers revised their 2026 inflation outlook higher (to 2.7%), and the dot plot – which reflects individual members’ rate expectations – continues to point to just one rate cut by year-end.

Jerome Powell, Chair of the Federal Reserve – the US central bank – described the outlook as one of “elevated uncertainty”, a signal markets interpreted as support for a higher-for-longer interest rate environment. In the aftermath, Bitcoin fell by around 5%, while the Dollar Index moved back above 100, creating additional pressure for digital assets. This marked the eighth of the last nine FOMC meetings after which Bitcoin declined within 24 hours of the announcement.

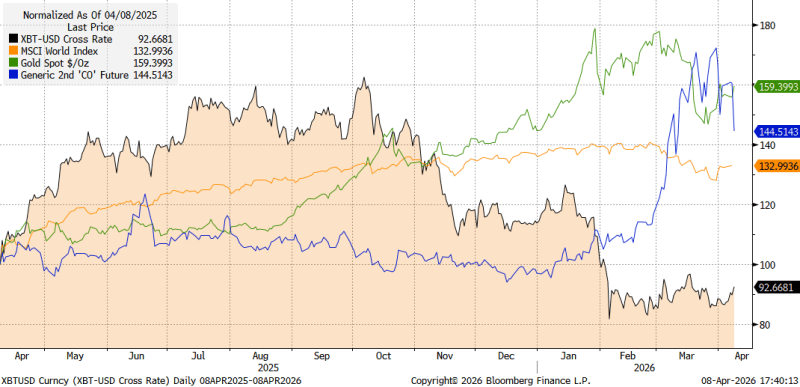

There was no clean defensive trade in March. The S&P 500 index dropped roughly 4.5% from early March levels. Gold, one of the year’s best performers, fell nearly 10% in two weeks as the energy shock simultaneously increased inflation fears and rate concerns. Bitcoin matched the S&P’s percentage decline; which, given its historical volatility, felt more like stability rather than weakness.

The market spent March choosing between imperfect shelters, and crypto held its own better than many expected. Bitcoin ended March around $66,700, down roughly 4% on the month despite briefly touching $76,000 mid-month. Ethereum traded between $2,000 and $2,300. The broader market sat near $2.44 trillion of total market cap. Nothing about the headline numbers screamed optimism. Beneath the surface, though, these weeks delivered arguably the most important regulatory and institutional developments the industry has ever seen.

Happy 20th million birthday

Another important fact worth mentioning is that, on-chain, the Bitcoin network mined its 20 millionth coin on March 10, leaving just 1 million BTC to be produced over the next 114 years. Reaching the milestone of 20 million mined Bitcoin (BTC) marks a crucial step towards its maximum programmed scarcity.

Out of a total maximum of 21 million, this means that over 95% of the total supply is already in circulation. Nevertheless, with an estimated 2.3–3.7 million BTC permanently lost, effective circulating supply is far tighter than headline figures suggest. Anyway, with just 1 million BTC left to be mined over the next 114 years, Bitcoin is cementing its status as a digital safe-haven asset, much like gold. Bitcoin’s inflation rate now sits below 0.85% – less than half of gold’s.

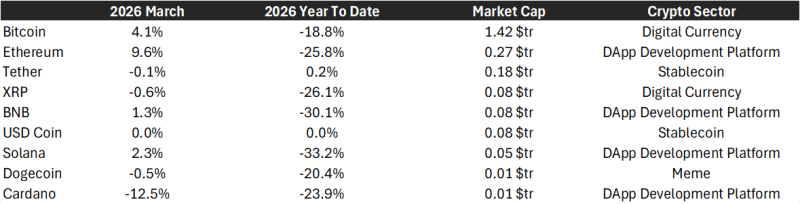

Within crypto, performance was fragmented and driven by specific narratives. Bitcoin dominance remained around 58%, suggesting that capital stayed concentrated in Bitcoin and that we are not seeing a broad “altseason” – a phase where alternative cryptocurrencies tend to outperform Bitcoin.

Ethereum outperformed Bitcoin in March, supported in part by BlackRock’s launch of the iShares Staked Ethereum Trust ETF (ETHB) on March 12 – the first crypto ETF from the world’s largest asset manager to incorporate staking, a mechanism that allows investors to earn a yield by locking up their assets to support the network. The fund allocates 70–95% of its ETH to on-chain staking via Coinbase Prime, generating a yield that is partially distributed to investors. Around 82% of the staking rewards – currently about 3.1% annually – are paid out on a monthly basis. ETH climbed over 20% in the eight days following the launch, reclaiming $2,300, as the “real yield” proposition attracted institutional capital in a higher-for-longer rate environment. ETH ETFs recorded a record $160.8 million in weekly inflows. The template – staked proof-of-stake asset packaged into a regulated, yield-generating ETF – now applies to Solana, Cardano, and Polkadot, for which filings are already pending.

Adding to the institutional momentum, Morgan Stanley launched its spot Bitcoin ETF (MSBT) on NYSE Arca on April 8 – the first such product issued by a major US bank. A spot ETF invests directly in Bitcoin, offering exposure that closely tracks its market price rather than relying on derivatives. With an annual fee of 0.14%, it undercuts BlackRock’s IBIT, making it the lowest-cost spot Bitcoin ETF currently available. The launch is supported by Morgan Stanley’s network of 16,000 advisors, who collectively oversee $6.2 trillion in client assets.

The regulatory breakthrough

March 17 may prove to be the most consequential day for US crypto regulation since the approval of spot Bitcoin ETFs. While global attention was focused on the Middle East, the SEC (Securities and Exchange Commission) – the main US regulator for financial markets – and the CFTC (Commodity Futures Trading Commission), which oversees derivatives and commodity markets – jointly published a 68-page interpretive release. The document classified 16 cryptocurrencies, including Bitcoin, Ethereum, Solana, XRP, Cardano, Dogecoin and Chainlink, as digital commodities rather than securities.

The release established a five-category token taxonomy and confirmed that staking, mining, and airdrops do not constitute securities transactions. After a decade of jurisdictional ambiguity, the fog lifted in a single day. SEC Chair Atkins said the agency was no longer the “securities and everything commission.” CFTC Chairman Selig told builders the signal was clear: build in the United States.

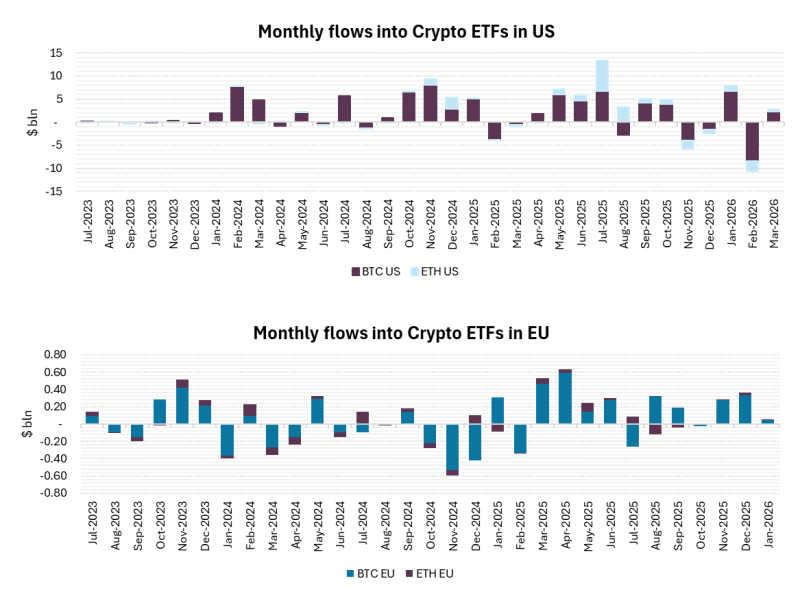

Three days later, a bipartisan Senate deal removed the last obstacle in the CLARITY Act – the stablecoin yield question – putting comprehensive crypto market structure legislation on track for passage, with prediction markets giving it 72% odds of becoming law in 2026. Bitcoin ETFs recorded $2.5 billion in net March inflows, reversing four consecutive months of outflows totalling ~$6.4 billion. Over 90 ETF applications were pending, with the commodity classification removing the primary regulatory barrier for all 16 named assets. The regulatory picture was, without hyperbole, the best the industry has ever had – and Bitcoin still ended the month down 4%, a reminder that macro overrides fundamentals in the short term.

Flows

The regulatory and market developments of March were the primary driver of flows. While still far from prior peaks, U.S.-listed products saw a meaningful pick-up in inflows, concentrated overwhelmingly in Bitcoin. On the Ethereum side, BlackRock’s newly launched ETHB captured the vast majority of net inflows, suggesting that the staking yield proposition – rather than a broad ETH re-allocation – was the marginal draw for institutional capital.

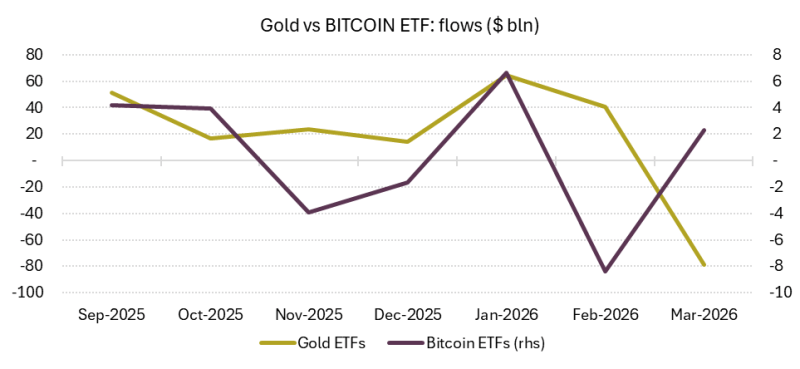

Finally, the first quarter of 2026 saw a notable divergence in the flow of funds between Gold and Bitcoin Exchange-Traded Funds (ETFs). Gold ETF flows, which were approximately $60 billion in January, plummeted, entering negative territory by March. This collapse was paradoxically linked to the Iran-driven energy shock, which undermined precious metals by fueling inflation and concerns about interest rates. While Bitcoin ETFs also experienced a sharp drawdown in February, losing around 8bn, they demonstrated a critical reversal in March. Flows turned positive again, notably coinciding with the March 17 commodity classification and a subsequent period of sustained inflows.

Looking ahead

March brought significant momentum to the crypto market. Key developments included the classification of 16 tokens as commodities, the launch of BlackRock’s first staked ETH ETF and Morgan Stanley’s first bank-issued BTC ETF, the mining of the 20 millionth Bitcoin, advancing comprehensive legislation, and a ceasefire alleviating a major macro overhang. While it’s premature to declare the end of the turmoil, the hope is that a lasting ceasefire will allow the market to finally acknowledge and price in what has quietly become the strongest fundamental backdrop crypto has ever experienced. This repricing will be the defining factor of the next chapter.

Investing in Crypto involves a high level of risk. You should not invest unless you are prepared to lose all of the money you invest. The value of your Moneyfarm portfolio can go down as well as up, and you may get back less than you invest. You may not be protected if something goes wrong. Past performance is not a reliable indicator of future results. The views expressed here do not constitute a recommendation, advice or forecast. If you are unsure whether investing is right for you, please seek independent financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.