As the Middle East conflict continues, we wanted to focus on what might be priced into equity markets at this point. We’ll take a look at valuations and earnings expectations.

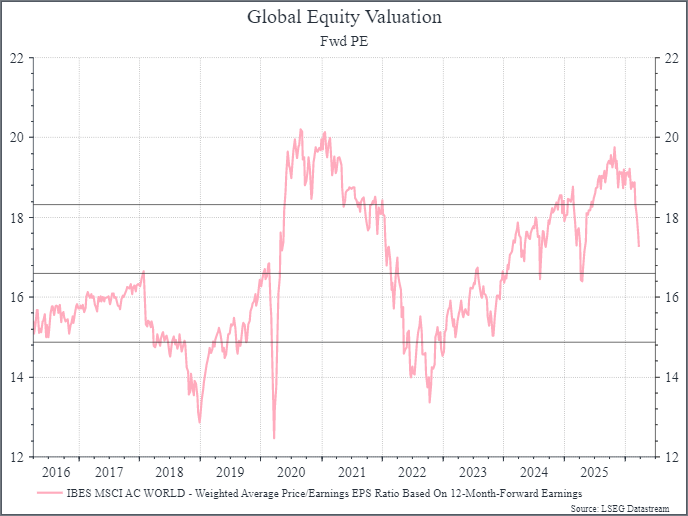

Turning first to valuations, the chart below shows the historical forward price/earnings ratio for global equities. We can see that equity valuations re-rated pretty steadily from the lows of 2022, as robust earnings growth, particularly in US tech stocks, helped to drive investor confidence. Since the onset of hostilities, we’ve seen equity valuations come down towards their long-term average driven by investor concerns about the impact of the conflict.

Long-term investors could view this positively. Starting valuations typically aren’t a great signal for returns over the next twelve months, but they are a more effective predictor for long-term returns. The lower the starting valuation, usually the higher the long-term returns.

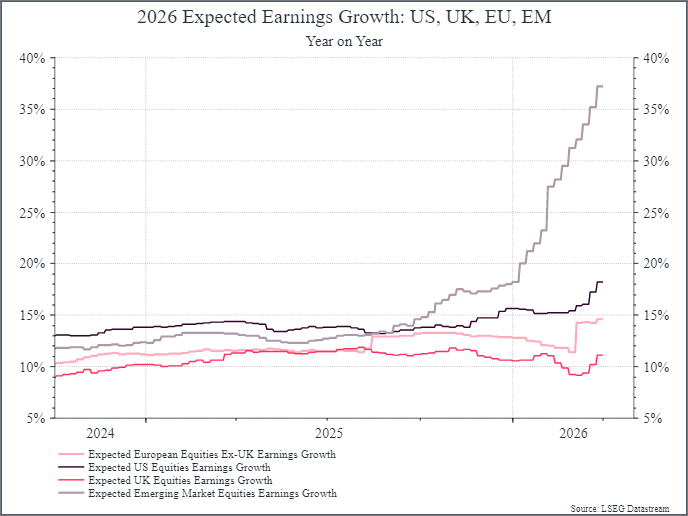

The second thing to consider are earnings expectations. The chart below shows expected earnings growth for 2026 for equity markets in the US, the UK, the Eurozone and Emerging Markets. We can see that we came into 2026 with pretty healthy growth expectations. Investors expected double digit earnings growth across all four regions. That’s part of what helped to drive the above-average valuations. The other point to note is that earnings expectations have risen since the start of the year. Analysts and companies were becoming more optimistic about the outlook – it seems particularly in Emerging Markets.

So, at first glance it looks like we’ve got a combination of lower valuations and stronger earnings growth – that feels like a pretty compelling combination. The catch – there’s always a catch – is that earnings revisions tend to lag. Analysts and companies don’t react instantly to news, particularly geopolitical news. They don’t necessarily want to change their forecasts and budgets in response to events that might be short-lived. Usually, you might expect equity prices to move before earnings expectations.

In this current scenario, the rise in the oil price from $60 to $100 per barrel is a macro shock that is likely to impact growth and inflation, particularly if those higher prices persist. You’d expect to see an impact on a range of prices – from petrol to food and even into technology components. There’s been a lot of focus recently, for instance, on the availability of helium – which is produced in the Gulf and is used in the manufacturing of semiconductors.

We think the key questions for investors are how long will higher prices, and constrained supply, last and how significant will the impact be on corporate earnings. At the moment, it looks like oil prices will stay higher for longer. That could mean earnings growth gets downgraded and we think that’s some of what’s being priced into equity markets at the moment. With earnings forecasts potentially coming down, that price/earnings ratio from the first chart might be higher than it currently seems.

What does it mean for portfolios? Assessing the impact of the current conflict on earnings is a challenge. We don’t know how long the conflict will last, how much damage there’ll be to infrastructure, how great an impact it will have on the global economy and how that will feed into corporate earnings. It’s fair to say that the current move down in equity prices already reflects some of those concerns. We think the declines haven’t been particularly sharp, implying that investors believe the impact of the conflict won’t be too significant at least for the global economy and corporate earnings.

Companies in the US begin to report their first quarter earnings figures in the next few weeks and it will be interesting to hear what they say about the impact of the conflict. We’d expect to see some earnings forecasts come down at least slightly. For now, we’re maintaining a slightly conservative stance in terms of our equity positioning as analysts begin to reflect the impact of the conflict on their earnings forecasts.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.