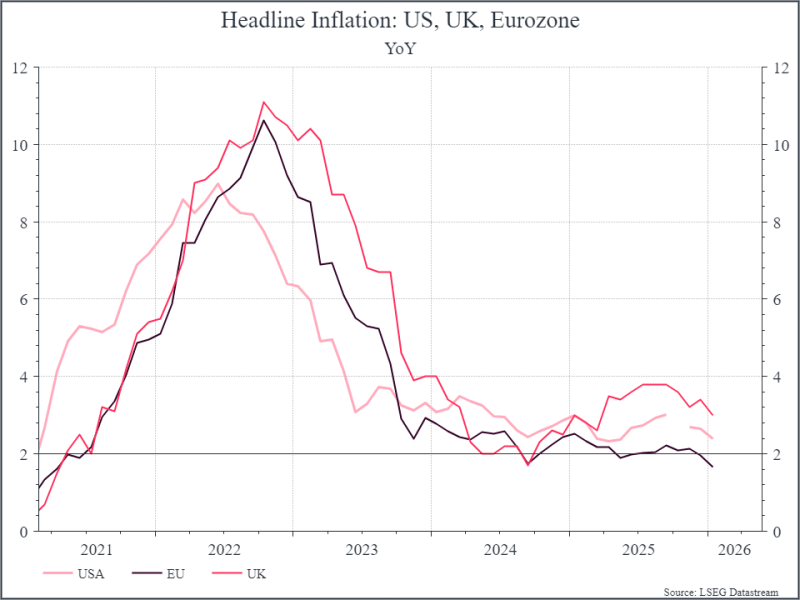

We’re taking a break from Artificial Intelligence (AI) this week and turning our attention to inflation. It might not have captured the headlines recently, but inflation has remained an important topic of discussion. The chart below shows annual headline inflation for the US, the UK and the Eurozone.

The basic story in recent years has had three parts. First, a sharp spike in 2022 pushed inflation to its highest level in decades, prompting Central Banks to hike interest rates aggressively. Second, in the wake of higher policy rates inflation began to normalize in 2023 and 2024, approaching the 2% level that Central Banks usually target. Third, tariff increases in 2025 raised the possibility of a re-acceleration in inflation in some markets1.

Within the Asset Allocation team, we have debated over the past couple of years whether we were moving to a new inflation regime – where inflation would be stickier and more volatile than had been the case in the period after the global financial crisis – from 2009 to 2021. That could mean higher long-dated bond yields and increased cost of credit for households and businesses. The potential impact on corporate profitability in that scenario is very interesting.

Overall, we think that inflation that sits a bit higher than target (say between 2-3%) could be quite positive for corporate margins. Another inflation spike, however, could cause more challenges. We guessed that developed market central banks – particularly in the US and the UK, would tolerate inflation that was a bit above the official 2% target, while staying formally committed.

Looking back at 2025, we could say that it was a case of “the tariff that didn’t bark”. Macro variables like inflation, and growth, didn’t see the impact of higher tariffs that many had expected. On the inflation side, some argued that it was the result of pre-tariff inventory building, so businesses didn’t need to hike prices on day one. Others argued that the ending tariffs were much lower than feared and so were absorbed within the supply chain.

As we come into 2026, the early data suggests that the inflation outlook looks pretty decent. UK and US inflation is still above the 2% target but January data was a bit better than expected. In the EU, inflation has gone below the 2% target. If we see these trends continue, that should give Central Banks some comfort to reduce policy rates a little bit more – albeit not by much. A combination of controlled inflation and decent economic growth would be a positive macro backdrop for financial assets.

There are, inevitably, a few caveats to this pretty rosy picture. Monthly inflation data can be volatile and sometimes contradictory. The PCE index for December (a different inflation report that the US Federal Reserve focuses on) showed figures that were a bit higher than the headline Consumer Price report. Commodity prices and geopolitics are still relevant – particularly if oil supply is disrupted – although a cooling of tensions could provide some relief there.

The labour market also remains a focus of attention – wage growth in the UK for instance has been pretty decent even if unemployment rates have drifted higher – that could create some challenges for Central Banks. Finally, we should remember that slowing inflation doesn’t really tackle some of the cost of living challenges that many households feel. Central bankers can see prices rising at only 2% and declare victory, but households still see rising prices. That might partly explain why decent headline macro data, particularly in the US, hasn’t translated into greater satisfaction among many voters.

But putting those concerns to one side, the inflation outlook so far looks fairly decent in the UK, US and EU. That should help to contribute to a positive underlying macro backdrop that we think will be helpful for financial assets.

- There are various complexities beneath the headlines, but we’ll leave those alone for now – did inflation come down because of higher policy rates, or was it just the result of a supply shock that didn’t need rates to go higher? Will tariffs result in sustainably higher inflation, or would it just be at worse a one-off increase?

↩︎

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.