It’s been a busy couple of weeks globally and on the markets. We could be forgiven for concentrating solely on events related to Greenland, but that was not the only issue drawing attention.

There were at least two topics of debate within the Asset Allocation team – specifically, the Japanese government bond market and the proposal to cap credit card interest rates in the US at 10% for a year.

First, on Greenland, there was certainly a lot of noise. At one point, it seemed the US might consider using military force to occupy territory on which it already had a military presence. Then, there was the threat of tariffs on countries who might oppose the US “purchase”. Finally (at least as of Friday afternoon), there seems to be some sort of agreement in principle, whose details are vague, but which doesn’t involve either an outright purchase, or the use of military force or the imposition of further tariffs.

Financial markets reacted as one might have guessed. Equity markets weakened on the unlikely prospect of a conflict between NATO members and the (higher) probability of increased tariffs between the US and Europe. Gold rallied. Signs of a resolution on both counts then left investors at least somewhat relieved.

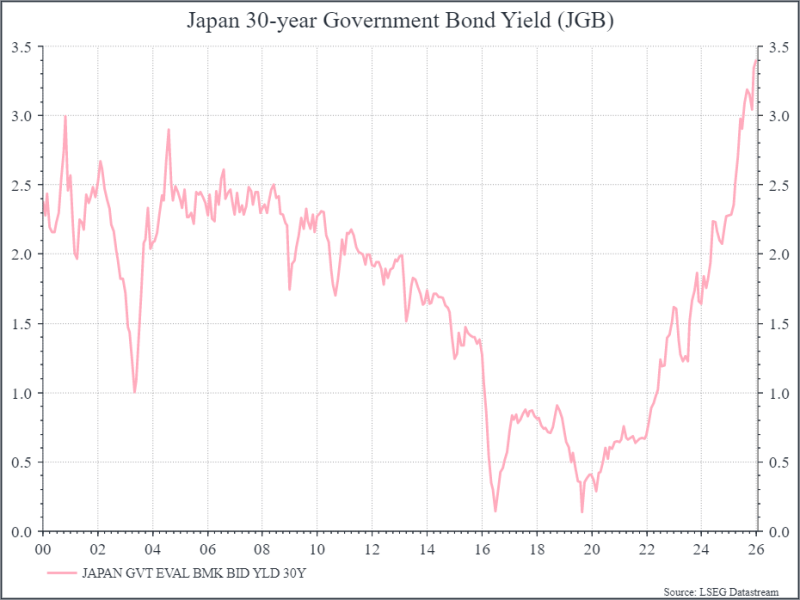

Second, we’ve seen volatility in the Japanese bond market, with bond yield rising (and then falling) quite sharply. The immediate cause has been around concerns of increased government spending, but we’ve seen Japanese bond yields rising sharply over the past couple of years, as you can see in the chart below, while inflation has picked up.

So far, we’ve not seen a significant global impact from rising Japanese bond yields, but with a high debt to GDP and some political uncertainty ahead of a February election, we’ll continue to monitor Japan’s macro closely. We continue to hold Japanese equities in many portfolios, but our exposure to Japanese fixed income is comparatively limited.

Third, there’s ongoing tension between the US administration and US commercial banks. The administration is pushing to cap credit card interest rates at 10% for a year – compared to somewhere above 20% currently. As you might imagine, US commercial banks are opposing the proposal. The timing of the announcement suggests that this is an attempt to provide additional cash to households ahead of the mid-term elections later in the year – although similar proposals have gained support among Democratic politicians. At this point, getting this legislation passed looks unlikely, but the administration will probably look for other ways to boost its popularity among voters in the coming months.

What about the possible sector impacts?

Some of the consequences are already apparent – notably the prospect of increased defence spending – and European defence stocks benefited from this in 2025. It’s something we’d expect to continue in the coming years.

Other sectors that could be impacted include technology and pharmaceuticals. We’ve already seen regional legislation potentially impact global technology businesses – and add to geopolitical tensions. We could see the rise of national or regional champions, as governments try to reduce their dependence on global providers. In a similar vein, the US administration has been focused on drug pricing and sources of production. Chinese producers hold a high market share of many medicines, or active ingredients. In a world of rising geopolitical tension, governments could increase their focus on domestic production.

This line of thinking hasn’t come out of nowhere. The Covid experience highlighted the ways in which global trade linkages could break down under unexpected stress. The challenge for many Western governments is that building that resilience requires investment, and cash is in short supply. It remains unclear how governments in Europe will fund the increased defence spending that they need. One potential outcome is larger deficits and potentially higher bond yields.

The other side of the coin is the potential for increased investment spending driving faster economic growth. We’ve already seen spending on data centres help to support US GDP growth and we remain optimistic that Artificial Intelligence (AI) adoption will justify that spending over time. Whether other economies, notably in Europe, can accelerate their investment spending, on AI or other projects, remains to be seen.

How should we think about all this?

There’s a lot of noise in politics at present and we’re generally wary of making snap judgements on the basis of the latest headline or tweet. That said, we do think that geopolitical relationships are shifting in ways we haven’t seen in the recent past, following on from US Commerce Secretary Howard Lutnick’s remark that “Globalisation has failed the West”. That could have implications for government balance sheets, economic variables and corporate profitability – creating potential winners and losers.

In terms of portfolio construction, we think that the old adages still hold, if not even more so. Happily we continue to see opportunities across a range of asset classes. We think that looking past short-term noise remains as important as ever. We think that diversifying exposure remains key – across sectors, geographies and factors – as we look for ways to manage potential short-term volatility.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.