For a long time, financial planning was seen as a service which was reserved exclusively for the wealthy. The prevailing belief was that unless you had a large sum to invest, bespoke guidance was either unnecessary or entirely out of reach.

Even those with the means often hesitated. On the surface, managing personal finances seems straightforward: if you understand your outgoings and maintain a modest savings rate, things generally “tick along” just fine. While this reactive approach may suffice for the short term, financial planning is about ensuring you have enough throughout every stage of your life.

In a world defined by unpredictability where salaries fluctuate, families grow, and market conditions shift, the ability to adapt a plan is not just beneficial; it is imperative for achieving long-term goals.

So, what are the benefits of financial planning?

It is worth having a think of what are the benefits of financial planning. Some of these are more obvious than others, like having a better chance of setting yourself up for the future and being prepared for any unforeseen expenses.

While the primary goal of a plan is wealth creation and preservation, the psychological benefits are equally significant. A study published by Vanguard last year highlights the emotional value of financial support:

- Reduced stress: advised clients are roughly half as likely (14%) as self-directed investors (27%) to experience high levels of financial stress.

- Peace of mind: 86% of advised clients report greater peace of mind regarding their finances.

- Emotional resilience: professional guidance is particularly effective at mitigating negative emotions such as feeling overwhelmed or worried about the future.

Painting a picture

Consider the contrasting experiences of John and Marie, who shared identical career paths and lifestyle expenses. The critical difference in their outcomes was timing and planning: Marie was diligent from the start, contributing consistently to investment vehicles throughout her life, whereas John did not follow a plan or begin focussing on investing until much later.

So the basic assumptions are:

- Through their 20s they both earned £25,000 and £15,000 of expenses.

- Through their 30s, they both earned £45,000 and £25,000 of expenses.

- Through their 40s, they both earned £75,000 and £45,000 of expenses.

- Through their 50s they both earned £100,000 and £50,000 of expenses.

- They both decided to retire at the age of 60 with full state pension kicking in when they are 67.

To make it realistic, I have also added that both individuals make salary sacrifice contributions to their pension of 5%, whilst their employer matches them up to 3% for the total of 8%.

Both models will run till 83 (which is the ONS life expectancy for women) and have invested portfolios of the same risk level. Pension average growth of 6.5% and ISA average growth of 5.5%.

Upon retirement, both individuals utilise the Uncrystallised Funds Pension Lump Sum (UFPLS) method to withdraw funds efficiently, a strategy designed to maximise the longevity of their pension holdings. The following cashflow models illustrate the significant difference in wealth at the point of retirement, highlighting the impact of Marie’s commitment to a consistent, long-term plan.

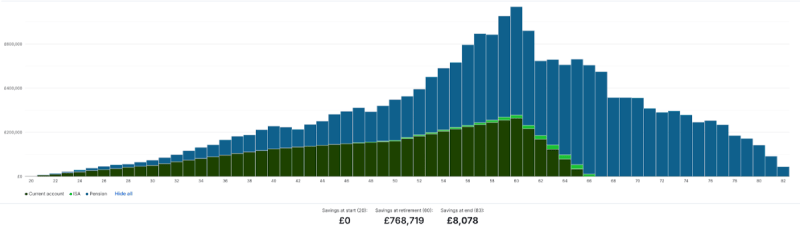

John’s cashflow

In this cashflow, you can see three separate coloured bars. The dark green bar is the cash savings that John has built through his career. The light green bar is an Individual Savings Account (ISA) he starts investing in when he is 45 and finally the blue bar at the top is his pension. He has been adding to this pension throughout his working life. Luckily for John, as he has been consistently in employment and has been contributing to his pension throughout, along with his employer. Unsurprisingly, it is the portfolio which grows the most.

John retires with an overall pot of £768,719, and is able to afford spending around £43,500pa till the age of 83.

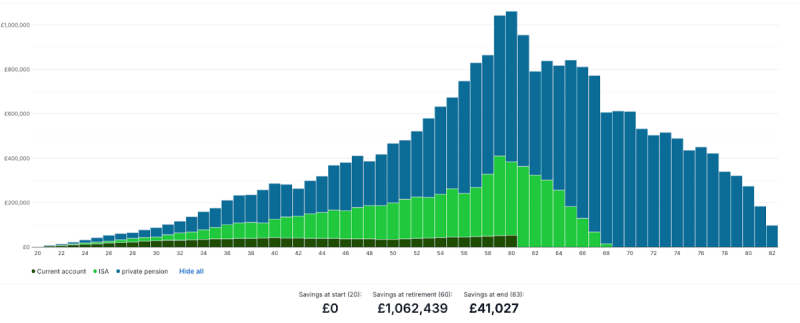

Marie’s cashflow

In Marie’s case, she has been saving a lot more regularly into her invested pots, but also keeping some cash reserved in case of any emergency. She has never had to stretch herself to keep money invested, instead she has remained consistent to her plans and saving habits. Because of this, she has been able to save a whopping £1,062,439 at the age of 60, with a healthy £63,000pa she can afford to spend through retirement and has money to spare. This is nearly £20,000 per year more income that she has in retirement.

By prioritising organisation early and establishing consistent, affordable saving habits, Marie secured a significantly more comfortable future than John, who delayed his financial planning until later in life.

Marie’s success was built on simple, disciplined contributions:

- Early career (20s): contributed £100 per month into her ISA.

- Mid-career (30s–50s): increased ISA contributions to £500 per month.

- Late career (50s+): maximized contributions at £1,000 per month.

Continuous support: added £100 per month to her pension from the start of her career to further boost her retirement pot.

Unlike John, who eventually had to play “catch up,” Marie’s proactive approach across short, medium, and long-term horizons allowed her wealth to grow without ever overstretching her finances.

Planning in a volatile world

The last few years have been undeniably chaotic. We have seen significant budgetary shifts, frequent changes to fiscal rules, and markets that are difficult to read driven by everything from the rise of Artificial Intelligence to global geopolitical tensions and tariff wars.

Navigating this complexity is time-consuming and often daunting. At Moneyfarm, we are dedicated to helping individuals navigate their financial journey, regardless of which stage of life they are in. Rather than struggling on and making all the decisions for yourself, we are here to help, guide you and give you the support you need, so that you can achieve your financial goals. As we should now be well underway with our new years resolutions, one to add could be to get control of your finances, building a solid plan to secure a more comfortable future.

Our Guidance+ service offers a comprehensive analysis of your income and expenses in relation to your short, medium, and long-term objectives. We use advanced cashflow modelling to help you visualise your financial trajectory and identify any potential shortfalls.

The models shown above were created using FE Analytics, the tool we use to provide these detailed visualisations. This allows you to make informed decisions about your priorities and make sure you remain on track to reach your goals.

Rather than a one-time event, our clients find that returning for periodic reviews is helpful to long-term relevance. By regularly adjusting your strategy to reflect life’s changes, you ensure your plan remains accurate. This proactive approach provides reassurance that you are moving in the right direction, reducing financial stress and anxiety.

As always, our team is always available to assist with any questions regarding your account. Please feel free to reach out to discuss your account; our consultants are ready to listen, offer guidance and help you make sense of your investment objectives.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.