As US companies begin to report their results for the fourth quarter of 2025, we wanted to take a look at what analysts are expecting for earnings growth this year. Earnings aren’t the only thing in life, but they are typically a key indicator that many investors look at. Looking at how these forecasts change over the course of the year gives us a sense of how corporate profitability and even the macroeconomic environment are changing.

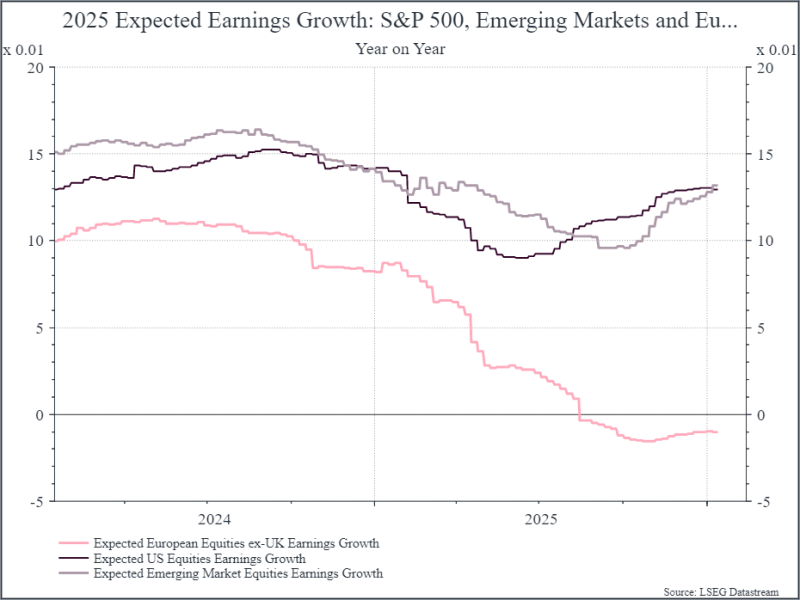

Let’s start by looking back at 2025. The chart below tracks expected earnings growth for 2025 for the US, Emerging Markets and Europe excluding the UK. For the US and Emerging markets, expectations were pretty robust at the start of last year, with analysts expecting double digit growth. Those forecasts came down in the middle of the year, as analysts tried to factor in the impact of the tariff war launched by US President Donald Trump in March.

Later on, as fears of a tariff-driven recession receded, we see earnings expectations rise again – ending the year in pretty decent shape. The picture in Europe was a bit more mixed, with earnings downgrades throughout the year, even as European equities performed well.

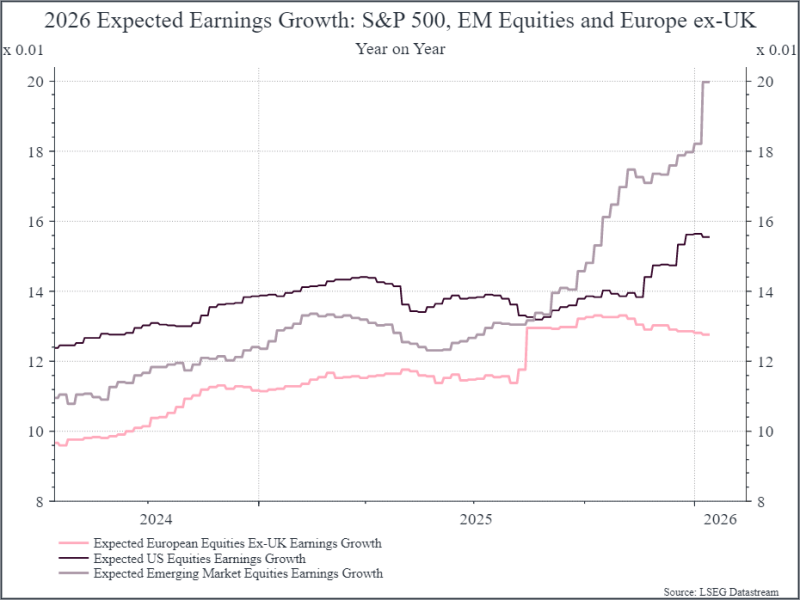

Turning to 2026, the chart below shows the same data but for 2026 earnings forecasts. Again, we are coming into the year with robust earnings expectations – particularly in Emerging Markets. European forecasts are lower again, but analysts are expecting double-digit earnings growth across all three regions, which is a pretty optimistic outlook.

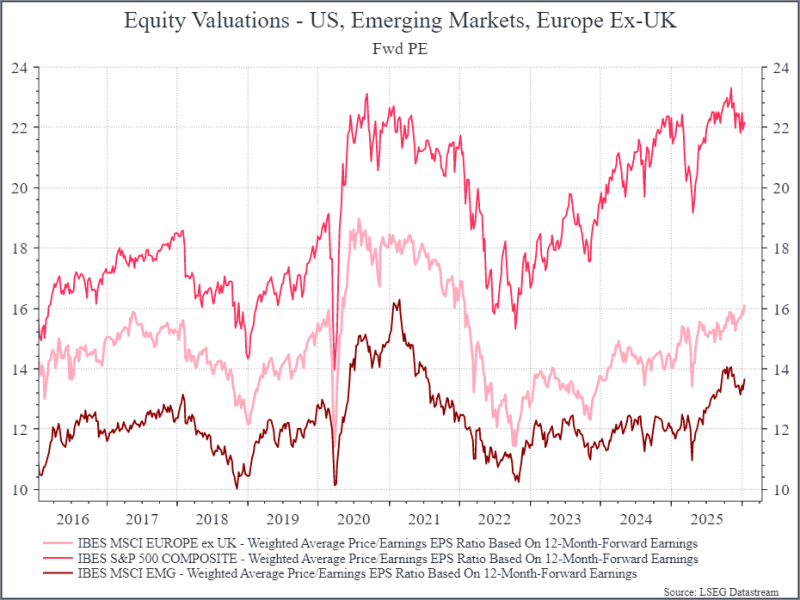

Now let’s overlay this with starting valuations, which suggest that investors are taking an optimistic view of the world. The chart below shows the historical forward Price/Earnings ratio for the US, Emerging markets and Europe excluding the UK. As we’ve noted before, valuations in the US are close to their recent peak. Valuations in Emerging Markets and Europe have risen over the past three years, but are below the 2020/2021 peak and remain at a decent discount to the US.

What should we think about this optimism? Inevitably, there are a couple of different perspectives. On the one hand, you can argue that strong earnings growth, if that’s actually realised, should help drive equity performance. That’s not always the case – Europe performed well in 2025 as earnings expectations fell – but on balance you’d expect that a healthy earnings backdrop would support financial markets. The other perspective is that these earnings expectations are already high, and that’s reflected in both forecasts and, to some extent, starting valuations. According to this line of thinking, high expectations raise the risk of disappointment down the line.

Where do we come out? On balance, we’re taking a constructive view for now. We’re mindful of the high starting expectations and valuations that are above long-term averages, and that has kept us from increasing our equity exposure in recent months. But we think that the macro backdrop looks quite solid. Lower policy rates, increased fiscal spending and a continued boost from Artificial Intelligence investment should be supportive.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.