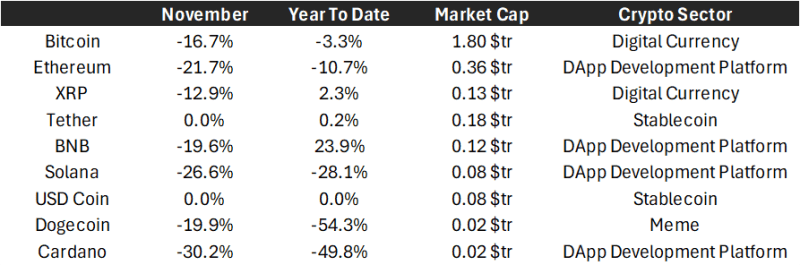

November 2025 proved to be one of the harshest months for the crypto ecosystem in the current cycle, characterized by a sharp “reset” in valuations. After peaking in October, the market faced a significant deleveraging event – a wave of forced unwinding of leveraged (debt-funded) positions – driven by record ETF outflows and macroeconomic headwinds.

While Bitcoin and major assets suffered double-digit drawdowns, the month highlighted a rotation of capital into privacy-focused assets and exposed fragility in speculative sectors like meme coins, a type of cryptocurrency often inspired by internet memes, characters or trends.

The broader market saw approximately $1 trillion wiped from the total market cap in what analysts described as a classic ‘flush’ of excess leverage.

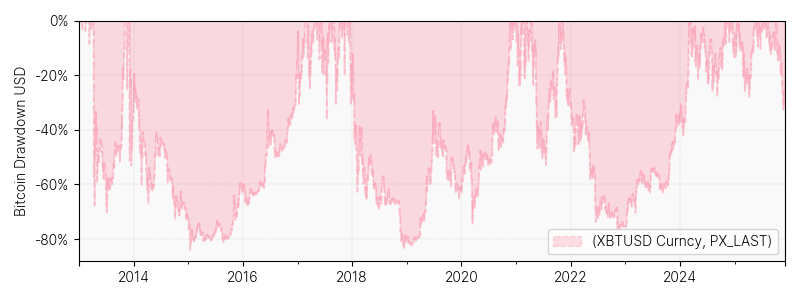

Bitcoin ended the month trading near $91,000, representing a roughly 17% decline for the month and experiencing a total peak-to-trough drawdown of approximately 32%, testing support levels near $80,000 before stabilizing.

Ethereum underperformed Bitcoin, closing down roughly 21% for the month while meme coins were decimated, with the sector down about 19% on the month and some indices reporting a 66% collapse from 2025 peaks.

We must emphasise that, given its high volatility, Bitcoin should be treated with care within a portfolio. While we are convinced that the ongoing institutional transition suggests we will no longer see drawdowns as in the past, its management in portfolios requires a cautious approach.

The macro

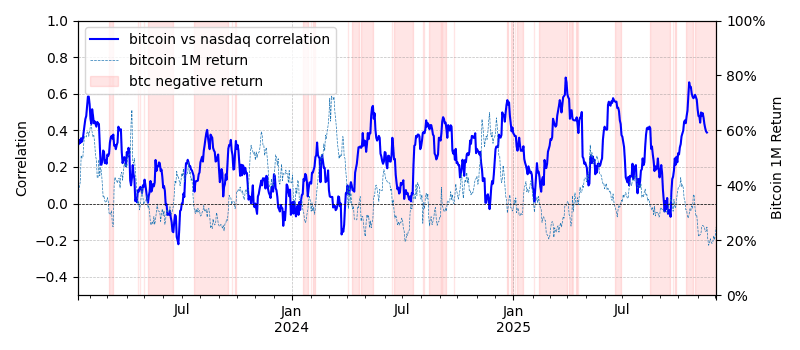

Bitcoin was caught in the broader retreat across financial markets, suffering from the general risk-off sentiment. The weakening of finance risk appetite was driven by several factors, including uncertainty surrounding Artificial Intelligence (AI), a reversal in expected monetary policy, mixed global economic signals, and trend exhaustion.

As is typical during periods of market stress, the correlation between Bitcoin and other cyclical equity assets increased as they collectively underperformed.

The current macro narrative suggests that conditions are aligning favorably for Bitcoin. As global liquidity reflates and monetary and fiscal policies ease across major economies, the coming weeks will be critical in determining if Bitcoin is truly positioned to navigate the narrative it is supposed to: decentralization, global fragmentation and increasing sovereign risk default.

The micro

In a month which offered few interesting narratives, one stood out remarkably. The “Privacy Renaissance” was arguably the most defining sub-narrative of November 2025: while the broader market deleveraged, capital rotated aggressively into privacy protocols. Privacy coins are cryptocurrencies designed to hide transaction details, like sender, receiver, and amount, making them more anonymous than standard cryptocurrencies like Bitcoin.

In our view, the increasing demands for transparency and accountability, driven by the integration of established crypto assets into the traditional financial world, are what is shaping the crypto user base response. This wider institutional acceptance comes with the cost of greater scrutiny. Consequently, it is not surprising that some coins may face being banned from “compliant” Tier-1 exchanges (that is, top-tier platforms meeting strict regulatory standards, such as Coinbase or Kraken in specific regions).

It is an important dynamic to be monitored, as it is an important step in the tug-of-war between old and new in the crypto investment landscape we have been describing for the last couple of observatories.

The flows

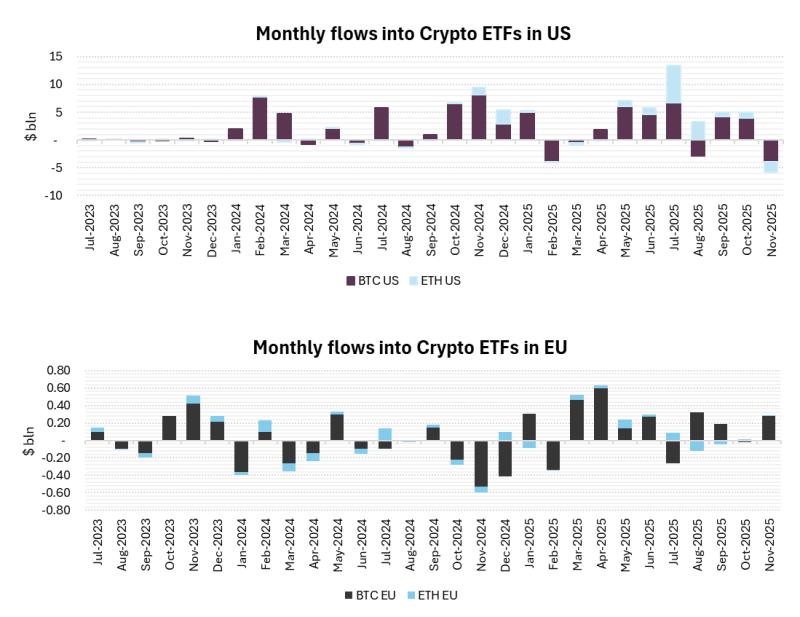

Flows were, predictably, subdued. In the US, both Bitcoin and Ethereum experienced their first month of outflows since February. Ethereum, in particular, saw its worst month on record in the US, underscoring the more cyclical nature of altcoins (that is, cryptocurrencies other than Bitcoin), even for well-established assets. European flows showed greater resilience; specifically, Bitcoin saw positive ETF inflows in November, following a more muted October. This signals a “buy the dip” sentiment among European investors.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.