For someone in their 20s and 30s, retirement may seem like a far off event. Something that is decades away. And since it is so far away, many people don’t give it much thought. However, this is exactly where compounding can be your best friend.

Saving in a SIPP (Self-Invested Personal Pension), with even very small amounts, can pay off handsomely when the retirement age comes close. Additionally, with a SIPP, you get control, flexibility, and a generous dose of tax relief to boost your savings.

What is a SIPP?

As anticipated, SIPP stands for Self-Invested Personal Pension. It is a type of personal pension that provides you full control over where your money is invested in to prepare for retirement. You can invest in various types of assets including stocks and shares, bonds, commodities and even real estate investments, depending on your provider.

Although many SIPPs allow employer contributions – like the one offered by Moneyfarm – unlike a workplace pension, it is not tied to your employer. It is yours, portable, and flexible. Most people use a SIPP to top up their annual pension allowance in addition to their workplace pension or to consolidate any old employer pensions.

The big advantages: tax relief and compounding

A major benefit of investing in a pension is the tax relief you receive from the government. For example, if you pay £80 into your SIPP, the government adds £20. Therefore, your £80 becomes £100, even before it gets invested. Additionally, if you are a higher-rate taxpayer, you can reclaim even more.

Your money, once invested, grows tax-free. In a SIPP, there are:

- No capital gains tax; and

- No tax on reinvested income; which allows

- Growth to compound without a drag

This combination of additional funds added from government, tax-free growth, and compounding has the potential to drive huge long-term returns.

Contributing to a SIPP gives your retirement savings a stronger start because the government adds tax relief to your contributions – something you don’t receive with an ISA. This makes SIPPs more powerful on a pound-for-pound basis and boosts your investment from day one.

However, ISA funds can be accessed at any time, while pension savings are generally locked until retirement age, which is rising to 57 from 2028. It’s also important to remember that although up to 25% of your pension can usually be withdrawn tax-free, the remaining balance may be subject to income tax when taken.

The accumulation and decumulation phases

Your investment journey can be broadly divided into two stages: accumulation and decumulation.

The accumulation phase is the period where you plant the seed to grow your wealth. It is a time where you contribute regularly to build your long term savings. As you have the benefit of time on your side, you can ride out any market ups and downs while letting compounding do its magic.

Finally, the decumulation phase is when you begin withdrawing from your pension, this is usually at the retirement age.

To simplify, your 20s is the time where you plant the seed, 30s are when the trunk strengthens, yours 40s and 50s is when it grows and becomes a fully mature tree, and finally in your 60s you start enjoying its shade.

Starting late means your tree will still grow, but won’t become quite big.

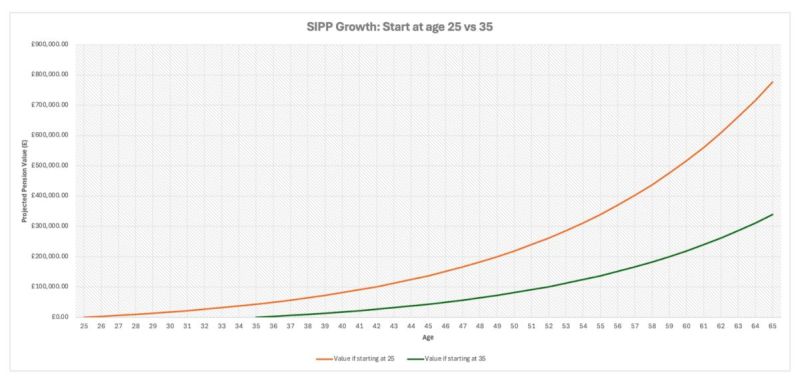

Starting at 25 vs starting at 35

To visualise what we have been discussing, let’s take a simple example to understand how SIPP returns work.

Let’s assume the following:

- £200/month net contribution

- 20% tax relief

- £250/month going into your SIPP after tax relief

- 8% yearly investment return

- Investing until the age of 65

Even with modest contributions, the effect is enormous.

As the graph demonstrates, the saver who starts early at 25 ends up with almost double the amount at the time of taking funds out of their pension pots even though they contributed for just 10 extra years. Why? Not because they saved that much more, but because their money had the time to compound.

An important point to note, is that the projection is for illustrative purposes only, uses an assumed annual return of 8%, and does not consider any fees paid. The actual returns may be higher or lower as investments in stocks and shares are subject to market risks.

The first 10 years of contributions don’t just grow, but they grow on top of their own growth, over and over, for four decades. This is the power of time.

The 2029 salary-sacrifice changes: what to expect?

During the recent Budget, a change in the salary sacrifice amount was introduced by the government. There is now a new cap that restricts National Insurance savings from salary sacrifice to £2,000 per year.

However, on the whole, investing in pension remains advantageous as a whole. You still get all the major benefits of investing in a pension:

- You still receive 25% upfront tax relief on personal contributions

- Higher-rate relief remains in place

- Employer contributions remain powerful

- SIPP investment growth remains tax-free

- No changes in the 25% tax-free lump sum allowance

It can be inferred that for most savers, the overall impact will be limited from the new rules, though the impact will vary based on individual circumstances.

How to start investing in a SIPP

Getting started with a SIPP is far easier than most people expect. You don’t need to know everything about investing, you just need to take the first step.

- Choose a SIPP Provider

Picking the right provider can be a great way to start your SIPP journey without any obstacles. Investors who do not know much about markets or do not have the time to manage can benefit from a managed SIPP, like the one offered by Moneyfarm. Your investments will be managed by experts, and you can observe where your funds are invested with complete transparency.

- Decide how much to contribute

You can start investing with what you can afford. For a Moneyfarm SIPP, you can get started with a minimum £500 investment and a minimum £100 monthly direct debit if you wish to contribute regularly to make the most out of compounded growth.

- Automate it

Set up a monthly direct debit. Automation removes emotion and makes investing consistent which is the key to long-term success.

- Review once a year

As a SIPP is a long-term investment, you won’t be able to access it until retirement. The age for retirement is increasing to 57 from 2028 onwards, and is likely to be higher when the current 20s and 30s workforce retires. This makes a regular check-in helpful. They allow you to understand how your portfolio is performing, whether your risk level is still appropriate, and how the broader market conditions impact your long-term plan. It’s also one of the advantages of a SIPP; you have far more control over where your money is invested as compared to most employer pension schemes.

Should you feel the need to do so, you can always book a call with a Wealth Manager at Moneyfarm to gain clarity.

Conclusion

A SIPP is one of the most powerful financial tools available to anyone in their 20s or 30s. It blends generous tax relief with the unstoppable force of compounding, giving even small monthly contributions the potential to grow into substantial long-term wealth.

The biggest advantage younger adults have isn’t money – it’s time. Starting early gives your investments decades to grow, smooth out market volatility, and multiply far beyond your contributions. And while pension rule changes may grab headlines, the core benefits of a SIPP remain intact: tax efficiency, flexibility, and long-term financial freedom.

The path to a strong financial future doesn’t require dramatic sacrifices. It only requires consistency and the willingness to start now.

This content is for general information only and does not constitute personal financial or tax advice. The value of investments (including a SIPP) can fall as well as rise. Past performance is not a reliable indicator of future results. Tax rules are subject to change, and the tax treatment depends on individual circumstances. Pension savings are generally locked until retirement age. If you are unsure you should consult a qualified and regulated financial adviser before making any investment or savings decisions.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.