In the Autumn Budget 2025, the Chancellor introduced a major change to the annual limit for Cash ISAs, effective from the start of the 2027/2028 tax year.

For individuals under the age of 65, the maximum you can contribute to a Cash ISA each tax year will be reduced from £20,000 to £12,000. Your total annual ISA allowance remains at £20,000. The change effectively designates the remaining £8,000 of the total allowance exclusively for investment products, such as Stocks & Shares ISAs.

There is an over-65 exemption. The government confirmed that individuals aged 65 or over will retain the full £20,000 limit for their Cash ISA contributions, as it acknowledged the greater need for lower-risk, accessible savings for those nearing, or already in retirement.

Given that this adjustment to allowances will have little meaningful impact on tax revenues, the underlying intention is likely to encourage UK savers to hold less cash and instead consider investing in stocks and shares. The aim is twofold: to channel more capital towards domestic economic growth and to help improve households’ long-term financial resilience.

That said, there are still uncertainties around how these rule changes will work in practice. While the government has published some guidance, it is also clearly trying to address potential loopholes. The proposals currently include the following measures to prevent savers from bypassing the new lower Cash ISA limit.

- Prohibiting transfers from stocks and shares and Innovative Finance ISAs to cash ISAs.

- Tests to determine whether an investment is eligible to be held in a stocks and shares ISA or is ‘cash like’. This may include qualifying Money Market Funds, which are investment funds focused entirely on capital preservation and income generation.

- A potential charge on any interest paid on cash held in stocks and shares or Innovative Finance ISA. Customers holding stocks and shares ISAs that pay interest on uninvested cash may face additional charges, to ensure these accounts cannot be used as de facto cash ISAs.

For now, these changes remain as draft legislation, and amendments can be made following consultation with the wider industry, leaving us all slightly in the dark for now.

Why are they doing this?

It’s worth noting that, when it comes to investing personal savings, people in the UK tend to be more risk-averse than many of our peers across the G7 – the group of major advanced economies. A recent piece of research conducted by Barclays (2024), estimates that UK adults are holding around £610 billion in cash savings in excess of the rule-of-thumb emergency fund recommendation (e.g. 3-6 months’ income). Their survey also uncovered that anywhere between 14-25% of adult savers are keeping more than 75% of their investable assets in cash.

It’s certainly worth bearing some context in-mind when reading this. It’s fair to assume that a portion of these individuals may be soon-to-be property owners, who may be holding a large proportion of their wealth in cash for good reason. Moreover, there will always be a relationship between interest rates, and the level of money being saved (as opposed to invested). With current interest rates being higher now than the 10-year average, it’s understandable that a greater amount of capital is being saved, not invested.

Nevertheless, the chancellor is obviously attempting to shift the balance between capital invested versus capital saved. On the whole, we believe there might be a compelling case for this allowance reform when you consider the longer-term outcomes. Let’s take a look at the last 20 years in more detail.

Examining 20 years of returns on cash versus stocks

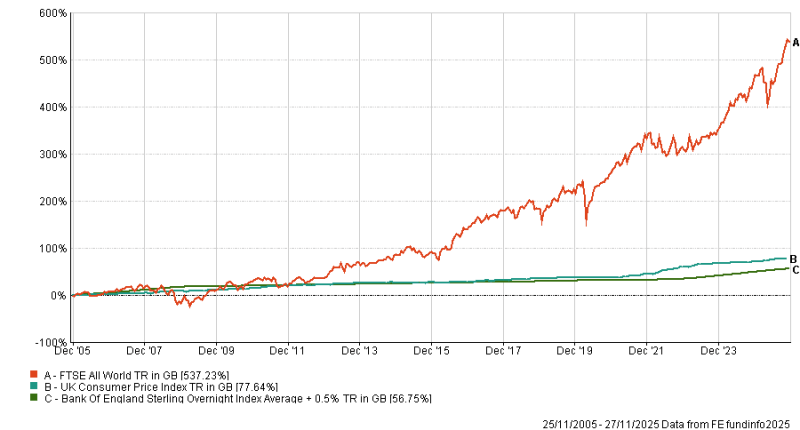

Cumulative 20-year returns on Global Equities, Cash & Inflation

The chart above illustrates the total returns of three different indices over the last 20 years. Plotted in red is the FTSE All World index, which we’ll use as a benchmark for global equities; tracking some four-thousand large and mid-cap stocks, over c. 50 countries. Plotted in cyan-blue is the consumer price index (CPI); the preferred measure of inflation in the UK. Plotted in green is the Sterling Overnight Index Average (SONIA) + 0.5%; a measure of UK interest rates, which we’ve uplifted by 0.5% per annum to more accurately reflect the average interest rate available to savers.

What’s staggering is the divergence between the total returns of global equities (red) versus the rate of savings (green). Your average saver might have obtained a total cumulative return of around 56.7% over the last 20 years. It’s worth noting that interest rates were particularly low between 2008-2022, and savers will therefore have realised a meaningful chunk of that return in the last few years. On the contrary, an investor of global equities might have made a return of 537.2% in that same time period.

In other words, investors in global equities are around 9.5 times better off than if they had simply saved that money. Naturally, past performance is not a reliable guide to future results.

Moreover, and perhaps more worryingly, savers have not beaten inflation over this 20 year period. Total CPI has increased by 77.6%, roughly 19% more than the cumulative rate of interest accrued by savers. In other words, relative to rising costs of living, money sitting in savings accounts has actually lost almost 20% in buying power over the last 20 years.

No matter which way you look at it, an overarching trend is clear. Historically, over a long enough period of time, global markets tend to outperform the rate of interest, and more importantly, the rate of inflation. We should all bear this in mind when we think about our long-term saving and investment plans. The Chancellor evidently has, and this is why we think she’s made this policy announcement.

How should we strike a balance?

Why do we save? First and foremost, for safety, and principal preservation. Cash is the lowest-risk asset class; its nominal value is stable because it is not subject to market volatility. You are usually guaranteed to preserve the initial (principal) amount you put in, and it is usually protected by government deposit schemes like the Financial Services Compensation Scheme (FSCS) in the UK.

Of course it’s valuable to have funds that will remain nominally stable if you’re preparing for a liability, but we must be mindful of inflation risk eroding the real value of our money. If the interest rate you earn is lower than the rate of inflation, the purchasing power of your money has decreased over time, despite nominally rising in value. Investing, particularly in diversified portfolios of assets, is the most reliable way to generate a real return – a return above inflation – over the long term; both protecting and growing your future purchasing power.

Liquidity is usually a big part of our desire to save too: cash is instantly accessible. You can access these funds immediately (unless using a fixed-term savings product) without needing to go through the process of selling investments, which can take days, and without worrying about having to sell your investments when markets are falling.

Whilst definitely a key point, for any goals beyond the short term (typically 3-5+ years), the ease of instant access comes at a high opportunity cost. Cash sits practically idle, missing out on the historically heightened compounding growth offered by equities and bonds over the long term. The potential gains from your time spent in the markets, and the long-term historical upward trend of global markets, should far outweigh the minor inconvenience of a few days’ settlement time, especially when proper financial planning involves ensuring that your emergency funds are held separately, and that you can do both.

For those who are also investors, holding cash may be a portfolio ‘anchor’ and act as a buffer, reducing the volatility of your total value of assets and savings. It acts as a financial buffer, potentially preventing you from being forced to sell your growth investments if you suddenly face an emergency or need to cover short-term expenses.

There is a cost of over-anchoring, though. While cash is necessary as an emergency buffer, holding an excessive amount beyond this safety net can severely limit your portfolio’s long-term growth potential.

Every pound held in cash beyond your immediate needs is a pound that is not contributing to higher-growth returns. A well-constructed, diversified investment portfolio – containing both lower-risk bonds and higher-risk equities – can be appropriately de-risked without resorting to keeping large sums entirely in cash, thereby maximising the likelihood of achieving significant long-term financial goals.

In a nutshell, the risks of saving too much, and for too long, can have negative outcomes. Individuals who want the value of their capital to rise over time, not only to beat inflation but to become objectively wealthier, will invest their capital instead. This is precisely why your workplace pension schemes will be invested on your behalf, and don’t jut sit in a bank account generating interest.

At Moneyfarm, we recognise both the short and long-term needs of our clients, and that’s precisely why we’ve built a variety of new products and services in recent years. This is all achieved by combining robust digital advice solutions with human guidance and expertise.

When it comes to performance, we boast a strong track record of risk-adjusted returns, with our actively managed and diversified portfolios being consistently monitored and adjusted by our own Asset Allocation team.

We know that the world of savings and investment can be complex and overwhelming, even for more experienced investors. We believe that a big part of the investment-savings gap in the UK exists, in part, because people don’t have access to reliable, honest and free financial guidance. That’s why we offer the provision of free guidance from qualified Investment Consultants to all clients, blending the low cost of a digital platform with the reassurance of human expertise for portfolio selection and goal setting.

What’s more, as your assets grow, you’ll gain access to a dedicated Wealth Manager, ensuring the support scales with their financial complexity. By offering solutions like their low-risk Liquidity+ for short-term goals, alongside our core Stocks & Shares ISAs, Self Invested Personal Pensions (SIPPs), and General Investment Accounts, we aim to ensure that all parts of a client’s financial picture are managed in one cost-efficient and expert-supported environment.

If you are unsure where to start, you can book a call with one of our Investment Advisory team for expert guidance on your retirement strategy.

This content is for general information only and does not constitute personal financial or tax advice. The value of investments can fall as well as rise. Past performance is not a reliable indicator of future results. Tax rules are subject to change, and the tax treatment of all savings products depends entirely on your individual circumstances. You should consult a qualified and regulated financial adviser or tax professional adviser if you are unsure about your investment or savings decisions.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.