The UK Budget for 2025 landed last week, and it’s a good moment to take stock of your financial plan – and consider what those two hours of policy announcements (and that now-famous 203-page document) could mean for your long-term financial journey.

Of course, the spending deficit had to be closed through higher taxes in some form. But what really matters now is understanding the changes and how they fit into your broader financial resilience.

When policy misses the point

Britain loves cash. If you’re reading this, you are likely part of the minority who invests, yet many of your peers are not. The Budget has now capped Cash ISA limits – including ‘cash-like’ stocks and shares ISAs – at £12,000 from 2027, as part of an effort to boost the UK economy.

But will this work? Unlikely. Limiting cash allowances won’t suddenly turn savers into investors. The Chancellor herself stated that the average person is £50,000 poorer due to saving solely in cash products instead of investing.

While we at Moneyfarm know this to be true – it’s our full-time job, and we’re surrounded by the facts and evidence – the same can’t be expected of the average Brit who doesn’t work in the industry.

The real issue, in our view, isn’t the allowances – it’s education. Having been both a student and a teacher in my previous career, I’ve seen how uneven financial education can be. While experiences vary, I don’t recall any comprehensive teaching on financial literacy, investing, or the real impact of inflation. The message may now be “save less, invest more”, but I remain cautious, because it doesn’t address the underlying gap in financial understanding.

That’s where your most valuable asset comes in: a financial plan. At Moneyfarm, you also have access to our team of qualified financial consultants, who provide guidance to help you navigate these decisions with greater confidence. Knowledge is power – and the reality is that, if you leave your wealth in cash or cash-like products for three years or more, you may be missing the opportunity for potentially stronger long-term returns available from other asset classes.

The next step isn’t just about moving money; it’s about making a commitment to your future self. You need a strategic roadmap that confirms you’re not just saving, but optimising for your final goal.

Pension planning is a cliché, but it’s one for good reason

“Future you will thank you.” We recognise this in so many areas of life – exercise, eating habits, career choices – and personal finances are no different. The saying “Patience is bitter, but its fruit is sweet” fits well here. Planning is about setting your intentions and building the resilience needed to give your hard-earned efforts the best chance of paying off over the long term.

One of the biggest pitfalls for mid-career professionals is neglecting the long term. You’re busy managing the present – mortgage, children, career – but your future self will rely on the compound growth you may be missing out on today, meaning the way your money can grow on top of previous growth over time.

Now, it may be clear a plan is essential, but how does that actually look and should the news of the Budget change our plans?

Short answer is no. While the Budget has made pension saving through salary sacrifice slightly less advantageous for higher earners – by capping the National Insurance Contributions (NICs) relief to £2,000 – this does not change the core reality: pensions remain a central part of building a long-term financial plan for retirement.

The tax benefits of a pension – and especially of a SIPP (a Self-Invested Personal Pension) – remain strong and shouldn’t be overlooked. It’s also worth keeping in mind that the pension system is designed to encourage people to save for their own retirement, and tax relief is one of the main tools used to support that. None of this has changed with the Budget, and these features continue to make pensions an important part of long-term planning.

Just to recap the key incentives offered by a SIPP – incentives that remain in place and which we don’t expect to change for the reasons outlined above.

1. Immediate tax boost: You still receive Income Tax relief instantly. A basic rate taxpayer contributing £1,000 sees an immediate £250 boost, turning it into £1,250 in their SIPP. This is an immediate 25% return that no other investment provides.

2. Tax free growth: Your SIPP investment grows free from Income Tax and Capital Gains Tax throughout its lifetime, unlike other investment vehicles such as General Investment Accounts.

3. Final Tax free cash: You can still take up to 25% of your pension tax-free in retirement, up to the maximum permitted under the Lifetime Savings Allowance. This had been a major concern ahead of the Budget, and its confirmation is a useful reminder that making knee-jerk decisions based on hearsay isn’t always a sound strategy.

These benefits are great at any age, but by way of example say you’re 35 and planning to retire at 65. That’s 30 years of reaping the benefits; 30 years of top ups which in addition to your net contributions have three decades to grow (as we’ve always seen has shown to happen), 30 years of growth with no taxes, and 30 years of your tax free 25% growing in value.

If you’re serious about shaping the retirement you want and building a long-term plan, it’s important to understand the advantages of contributing to your pension. A SIPP remains one of the most tax-efficient ways to save for the future.

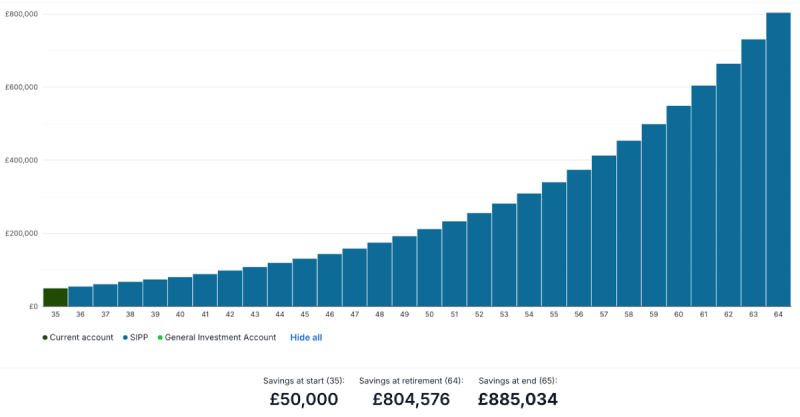

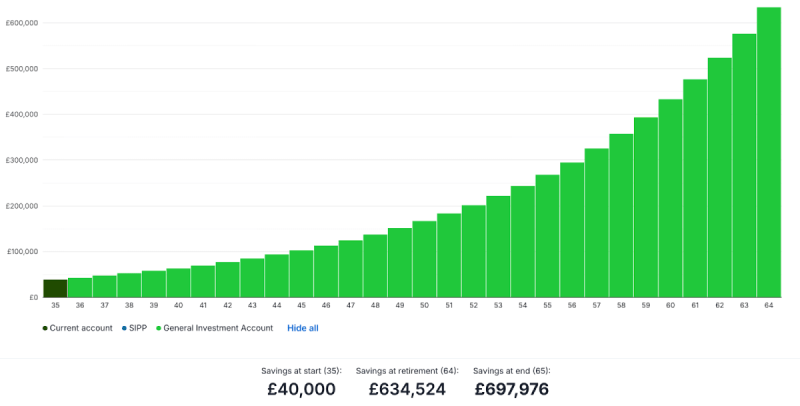

Let’s take a crude example to really see this in action: consider Kassandra and Ronald below. Both are 35 and considering investments with the aim to take funds at 65. Both Kassandra and Ronald invest £40,000; Kassandra into her Moneyfarm SIPP and Ronald into a GIA (a General Investment Account). We’ll assume 10% growth per annum for both.

Kassandra

Ronald

Although just for illustrative purposes, in the first scenario, contributing to the SIPP £40,000 (topped up to £50,000 from the government) would mean £221,258 could be taken entirely tax free (25% of the pot value) – leaving the remaining pot at £663,775.50 and no tax bill at that point in time.

If Ronald were to withdraw the same amount of £221,258 from the GIA, not only would he be looking at a hefty tax bill not far from 24% (£53,101.92) but the remaining pot stands at a comparatively measly £476,718.

All in all, hopefully this simple comparison clearly illustrates why your pension is such a critical tool for long-term saving and therefore the bread and butter of any long-term financial plan.

So, while the Budgets decision to cap NICs exemption for salary sacrifice contributions will impact many granted, hopefully the benefits of pension contributions are still overwhelming. If anything, the SIPP may seem more appealing relative to the duller salary sacrifice perk.

Bringing it all together

Where does this leave us? We’ve covered the importance of pension contributions, but a robust financial plan doesn’t end there. Alongside pensions and ISAs, consolidation is often the quiet hero of long-term planning.

Many people in their 30s, 40s and 50s have multiple old workplace pensions or scattered investments they’ve never properly reviewed. Bringing these together into a single, well-structured portfolio (for each type of account like SIPP, ISA etc) not only gives you better visibility, but could potentially make your money work harder for you rather than collecting dust (with likely higher fees) in forgotten pots.

And importantly you don’t have to figure this out alone. At Moneyfarm, our team, made up of Investment Consultants and Wealth Managers (myself included), are here to guide you through these decisions. Our job is simple: to help you build a plan you understand and can stick to. Clear guidance, smart structures, and a strategy built around your life.

Because at the end of the day, financial planning isn’t about predicting markets or reacting to every Budget headline. It’s about taking steady, intentional steps so your future isn’t left to chance.

So review your plan, consolidate where it counts, invest with purpose, and lean on the experts when you need clarity. The decisions you make today are setting the way for the future you want.

Just remember: your financial future isn’t built in a Budget, it’s built by you – one decision at a time.

This article is for information and general educational purposes only. The content offers general information on the Autumn 2025 Budget changes to salary sacrifice and long-term financial planning and is not personal financial or tax advice. The value of investments can fall as well as rise, and past performance is not a reliable indicator of future results. UK tax laws, including those relating to SIPP benefits and salary sacrifice, are subject to change, and the tax treatment depends entirely on individual circumstances. Before making any decisions about your pension or savings & investment strategy, you should seek advice from a qualified and regulated financial adviser if you are unsure about investing.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.