With all the focus on Artificial Intelligence (AI) and US tech, we wanted to shift our focus back onto European stocks.

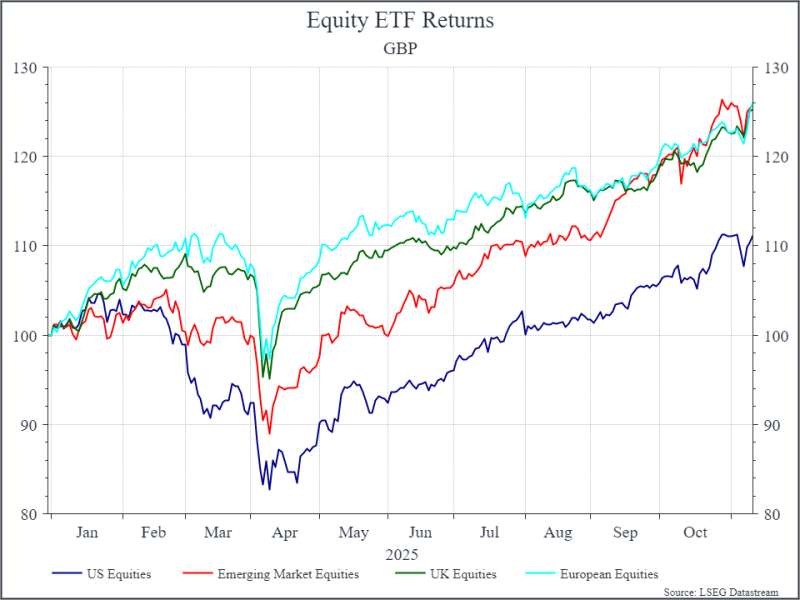

It’s easy to forget that so far in 2025 European equities have done pretty well. The chart below shows Equity ETFs for US, UK, Europe and Emerging Markets. The US lagged in the first half of the year, driven by concerns over slowing growth and the impact of higher tariffs. Outside the US, there wasn’t much to choose between Europe and Emerging Markets.

If we look only at the second half of the year, European performance has lagged behind the US and Emerging Markets, but given a return above 10% (in sterling), perhaps we shouldn’t complain too much.

It’s also worth remembering that this performance came at a time when earnings expectations in Europe slowed sharply. The chart below shows how expectations for 2025 earnings growth have shifted over time. For the US and Emerging markets, earnings growth expectations have held up well, while expectations for European (ex-UK) earnings have come down sharply over the course of the year. Overall earnings in 2025 look set to be flat compared to 2024. Given that backdrop, European equities have done better than we might have expected.

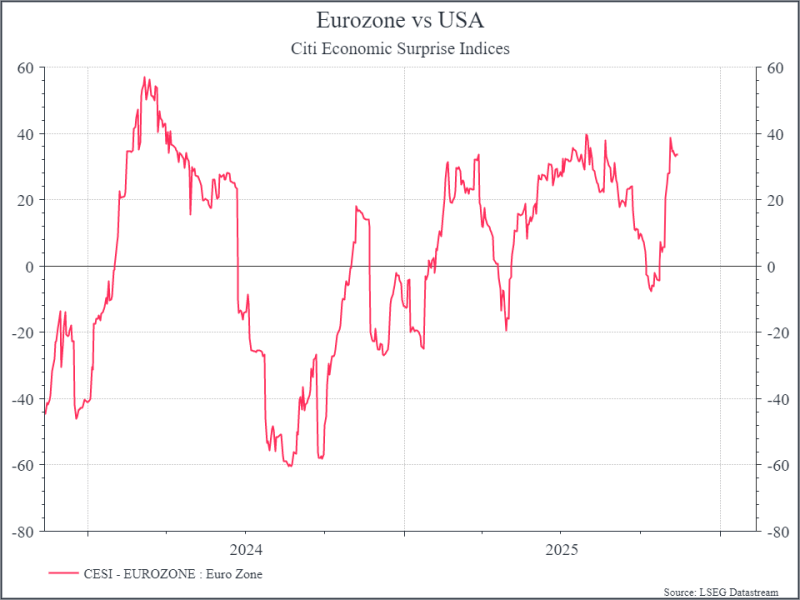

But there are some signs of improvement. First, on the macro side, we’ve seen macro data for the Eurozone coming in a bit stronger than expected – even if the expectations are typically quite low. The chart below shows a measure of economic surprises – how much did macro data come in better or worse than economists had expected. We’ve seen an improvement here in the last couple of weeks.

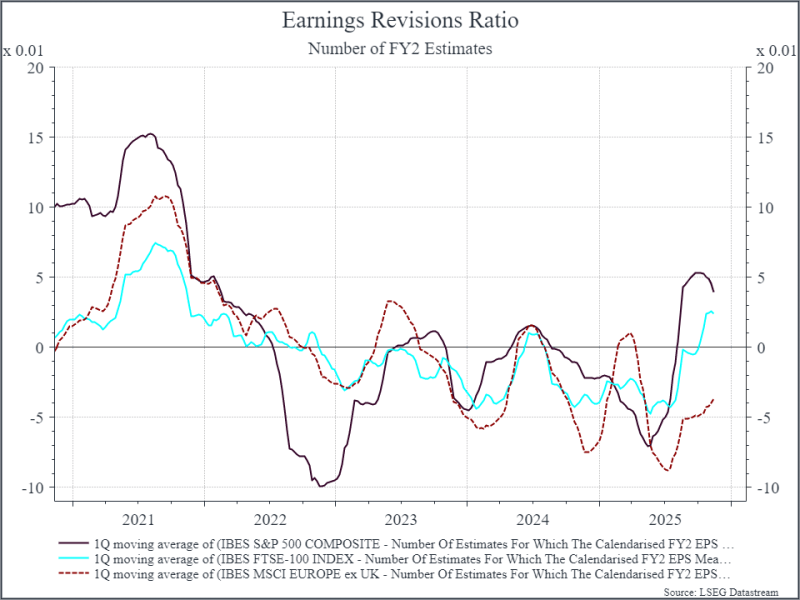

When we look at earnings revisions, we see that Europe has continued to lag behind the UK and the US. Equity analysts continue to reduce their forecasts more often than raise them. But that ratio has improved, and sometimes it’s the improvement that matters most for equity markets.

It’s probably a bit premature to put too much weight on earnings growth expectations for 2026 – but currently analysts expect US and European stocks to report similar earnings growth (above 10% in both cases). History says those numbers will move around, but a year of double-digit earnings growth would probably be good news for European equities.

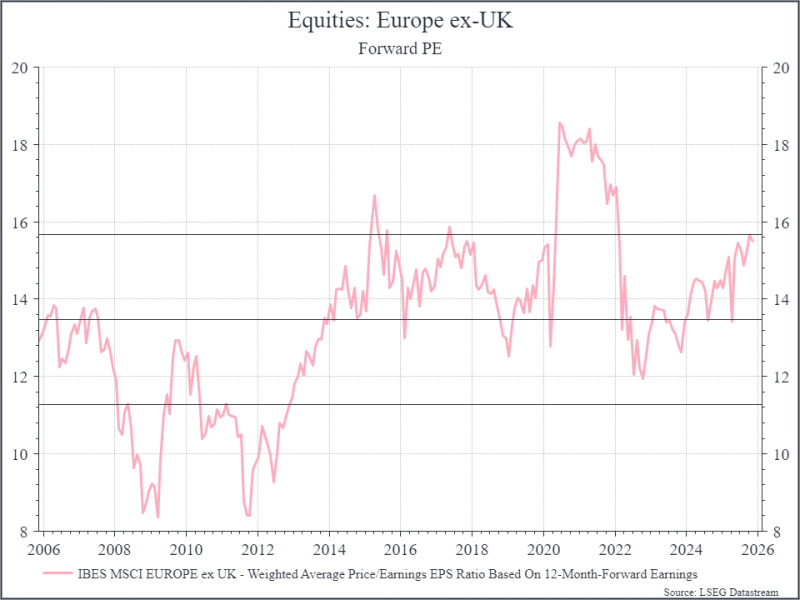

Finally, let’s turn to valuations. Here again, it’s a bit of a mixed bag. The chart below shows the forward price earnings ratio for Europe ex-UK over time. They’ve re-rated over the past few months. That makes sense as prices have rallied, and earnings expectations have come down.

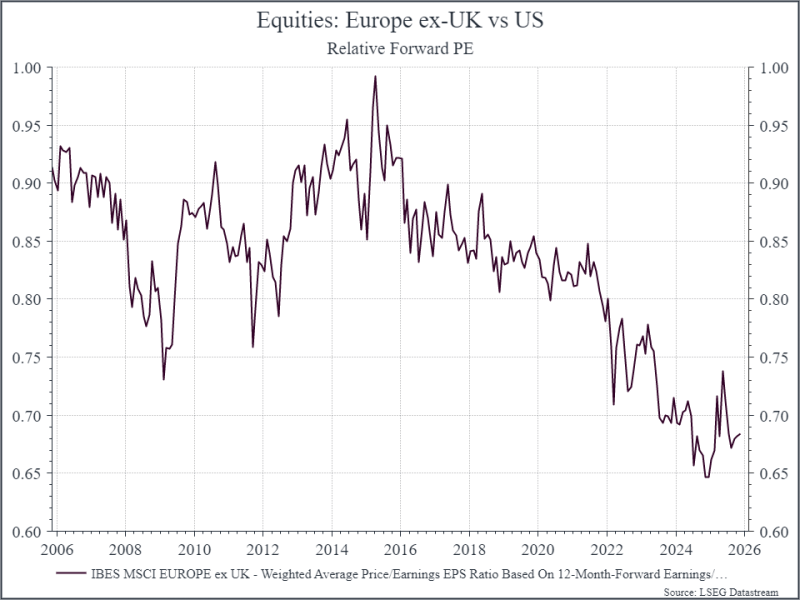

But if we compare valuations in Europe relative to US equities, we can see that the valuation gap remains wide.

So, where does this get us? European equities have probably had a better year than their earnings profile would have suggested. They’ve been particularly helped by financials and defense stocks. But there are some signs that 2026 could shape up to be a better year. With all the talk about AI stocks in the US, it’s a reminder that there’s still value in taking a diversified approach.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.