October 2025 will be remembered as a month of profound contradiction. It began with a euphoric rally – soon dubbed Uptober – during which Bitcoin (BTC) surged to a new all-time high of $126,270 and the total crypto market capitalization climbed to nearly $4.4 trillion.This optimism was, however, catastrophically inverted on October 10.

The month’s defining event was a severe, macro-driven flash crash, triggered by President Trump’s “tariff shock”. The president announced a 100% tariff on critical software imports from China, effective November 1, along with new export restrictions.

This catalyst ignited the largest liquidation event in the history of digital assets, vaporizing an estimated $19-20 billion in leveraged positions. The crash was exacerbated by critical systemic failures at the heart of crypto-native market infrastructure, most notably a trading engine freeze on Binance.

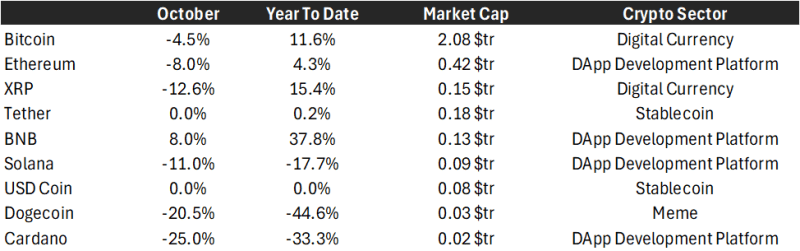

The ensuing damage was severe. The crash erased nearly all of the market’s 2025 gains. Bitcoin finished the month down -4% , and Ethereum (ETH) fell -8%. Risk-on sectors were decimated; the MarketVector Decentralized Finance (DeFi) Leaders Index plummeted -21.84%, and the Meme Coin Index fell -18.24%.

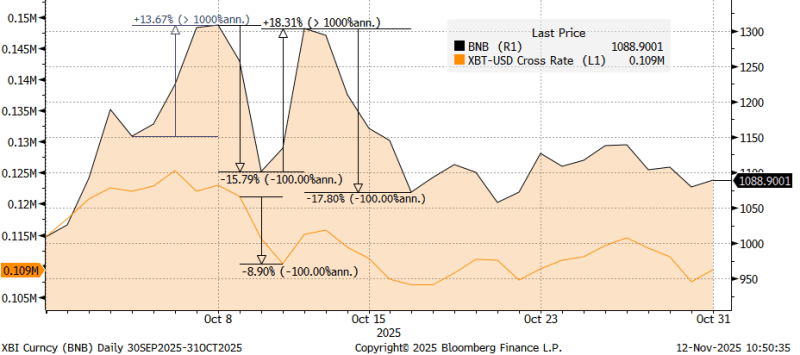

Binance Coin (BNB) ended the month in positive territory, but with extreme volatility – marked by sharp swings of around ±15% in quick succession, far exceeding typical crypto market fluctuations. The week of the announcement was difficult for the entire asset class, with Bitcoin losing nearly 9%. However, as shown in the chart below, it displayed greater stability in the days that followed.

Correlations that matter

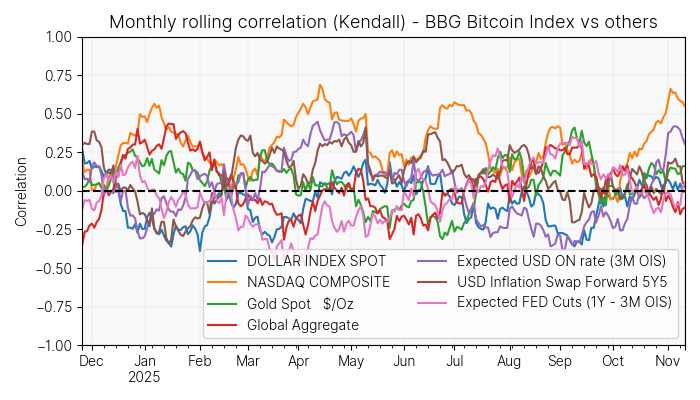

Correlation with major macro drivers remains weak. Bitcoin’s relationship with traditional drivers like gold or US monetary policy remains not significant (see chart below). Bitcoin’s decline started in early October, when the monetary policy outlook was still broadly dovish, and persisted even as sentiment turned more hawkish later in the month. By then, most crypto investors and traders were focused on the volatility triggered by Trump’s tariff announcement. Overall, it continues to be difficult to categorize Bitcoin within the traditional asset space.

The macro

The US government shutdown prevented investors from accessing a slew of data, keeping sentiment cautious as alternative indicators still point to a weak employment picture and softening economic activity, while inflation remains a concern.

The shutdown should have provided the perfect backdrop for Bitcoin, reinforcing the “debasement trade” narrative, but it was overshadowed by the Trump-induced volatility that triggered the month’s major crash.

The Federal Reserve (Fed) meeting was also perceived as broadly bearish, adding pressure on risk assets. However, the separate announcement of the end of Quantitative Tightening – the process by which the Fed reduces liquidity by shrinking its balance sheet – was seen as a mildly positive signal.

In general, as shown by the correlation, markets are still struggling to see a strong, consistent correlation between macro developments and Bitcoin.

The micro

The on-chain tug of war – the clash between buyers and sellers visible in blockchain data – continues, with market commentators attributing the crash to short-term positioning and derivative unwinds rather than fundamental shifts. A long-term “supply squeeze” narrative persists, evidenced by total BTC reserves on centralized exchanges hitting a multi-year low of 2.4 million, signaling a long-term holding strategy and waning sell pressure.

Conversely, on-chain analytics firm Glassnode data shows “persistent long-term holder (LTH) distribution,” with LTHs “selling into weakness” since July, reducing their supply by approximately 300,000 BTC. This signals “deeper fatigue and reduced conviction” among seasoned investors.

Given institutional inflows into ETPs (exchange-traded products that track the price of cryptocurrencies), LTH (long-term holders) selling, and the decline in exchange reserves, it is likely that coins are being moved from trading platforms to custodians and market makers. This transition reflects the increasing institutionalisation of the market, with the ETP ecosystem set to fuel the next phase into TradFi.

On the regulatory side, in October US crypto regulation saw a pro-industry shift. Trump picked Michael Selig as the Commodity Futures Trading Commission’s chair; the new SEC (US Securities and Exchange Commission) Chair Paul Atkins launched “Project Crypto” to create a “fit-for-purpose regulatory framework,” ending jurisdiction disputes; and the Senate drafted a comprehensive “cryptocurrency market structure bill.”

Crucially, the Treasury and IRS authorised crypto ETPs to stake their underlying assets – such as ETH (Ethereum, the second-largest cryptocurrency by market value) – and distribute the resulting rewards to investors. This removes a major disadvantage for US products, aligning them with practices already permitted in Europe.

Europe also saw changes, with the UK lifting the ban on crypto Exchange-Traded Notes (cETNs) for retail investors effective October 8. These products, initially tracking Bitcoin and Ether, are “Restricted Mass Market Investments” with strict consumer protections: mandatory appropriateness assessments, client categorisation, cooling-off periods, and a ban on investment incentives.

The flows

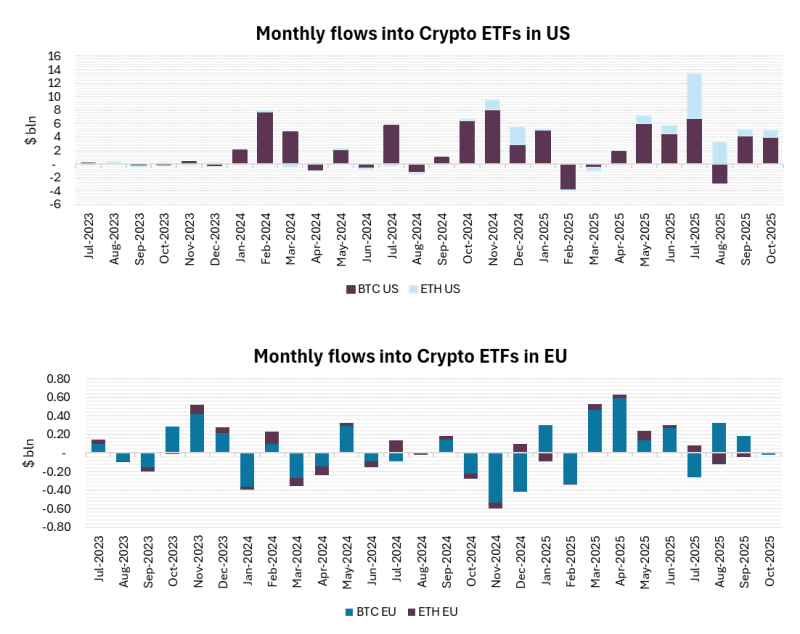

Investment flows in October indicated a mixed performance, with investors appearing willing to purchase the dips offered during the month.

Flows in Europe remained relatively flat for the period, while the US maintained some momentum, albeit significantly below the peaks observed in the Summer.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.