In recent years, the world of ESG (Environmental, Social, and Governance) investing has faced significant challenges. In 2022, amid the war in Ukraine, companies linked to fossil fuels outperformed due to the surge in commodity prices.

More recently, in 2025, gold and defence companies have dominated the markets. The latter has gained around 70% year to date, driven by ongoing conflicts, US pressure to increase defence spending relative to GDP, and Germany’s own spending plans. Gold has also posted an impressive rally, rising nearly 60% – a result only partly explained by the decline in real interest rates (yields adjusted for inflation) and largely fuelled by strong demand from central banks.

These geopolitical crises have temporarily shifted attention away from long-term sustainability goals. Adding to this, complex European regulation – while aimed at improving standards – has made the work of ESG managers more challenging. The sector has, however, developed in a positive direction, with investment methodologies growing more sophisticated and sustainability approaches gaining greater credibility.

In this article, we take stock of the ESG universe, analysing an increasingly complex market and explaining our approach.

ESG methodologies in the market

When it comes to ESG investing, it’s important to understand that there is no single strategy. Broadly speaking, three main categories can be identified.

- ESG Screened (Exclusion): starting from a traditional market index (the parent index), these strategies exclude companies involved in social controversies or controversial activities, such as human rights violations or tobacco production. These products do not actively seek to improve exposure to themes like decarbonisation.

- Climate (Climate-oriented): this category includes the Paris-Aligned Benchmark (PAB) and Climate Transition Benchmark (CTB). They follow the EU’s minimum requirements for climate-related investments, focusing more on climate considerations than on general ESG ratings. They still apply exclusions and select companies with clearly defined climate targets.

- SRI (Socially Responsible Investing): these strategies focus on managing sustainability risks using a “best-in-class” approach. They include only securities with the highest ESG ratings (typically the top 25%) and may apply additional criteria, such as restrictions on fossil fuels.

However, these labels alone are not enough to ensure consistency. An analysis of individual ESG ETFs on the market reveals significant differences: some active ETFs show exposure to fossil fuel–related companies even higher than their parent indices. Even within the same category, there are substantial discrepancies, making ETF selection more complex from an ESG metrics perspective.

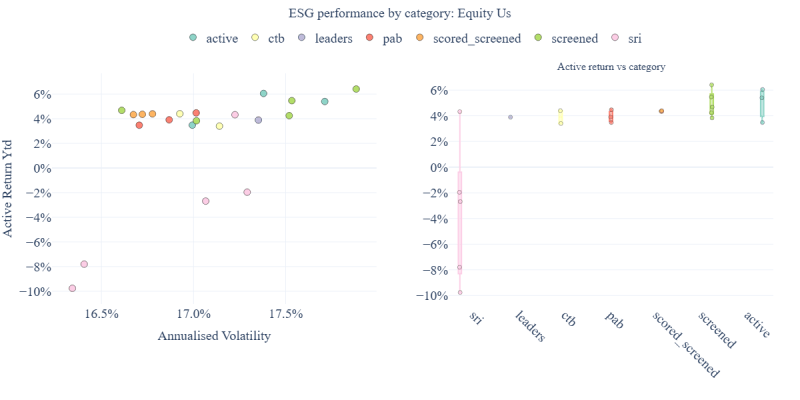

Differences are also significant when it comes to performance. The chart below shows on the left the performance of various US equity ESG ETFs from the beginning of the year to 1 October 2025. Performance is displayed on the vertical axis, while risk, expressed as volatility, is on the horizontal axis. Each point on the chart represents one ETF. It is striking to see that the worst-performing ETF returned around -10%, while the best achieved roughly +6%. In terms of risk, volatility is almost 1% higher.

The chart on the right groups performance by category. Each point on the chart represents one ETF. The SRI category shows the weakest and most inconsistent performance, while on average, screened and active ETFs have delivered better results.

The conclusion is clear: selecting ESG ETFs is a complex task that can lead to significant discrepancies – both in terms of ESG metrics and performance. Relying on a single category does not guarantee consistent outcomes, either from a sustainability or performance perspective.

The evolution of the ESG market

The enthusiasm for sustainability seen in the early 2020s appears to have faded. The resurgence of less environmentally focused narratives, the growing attention on Artificial Intelligence, and the exceptional performance of “excluded” sectors such as defence and fossil fuels have shifted investor focus elsewhere.

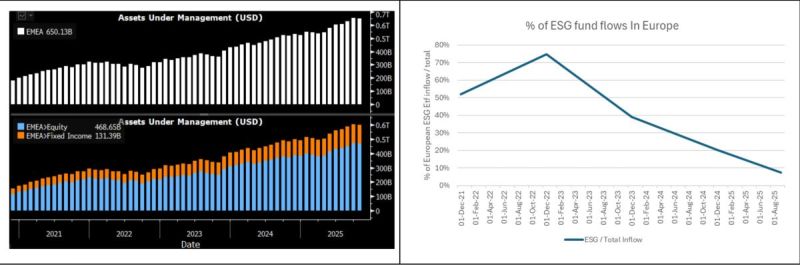

But is this perception accurate? The numbers paint a mixed picture. On the one hand, assets under management (AUM) in ESG ETFs across Europe continue to grow, having reached €650 billion – a sign of a resilient market. On the other hand, the share of new inflows into ESG products has slowed sharply, dropping below 10% of total inflows.

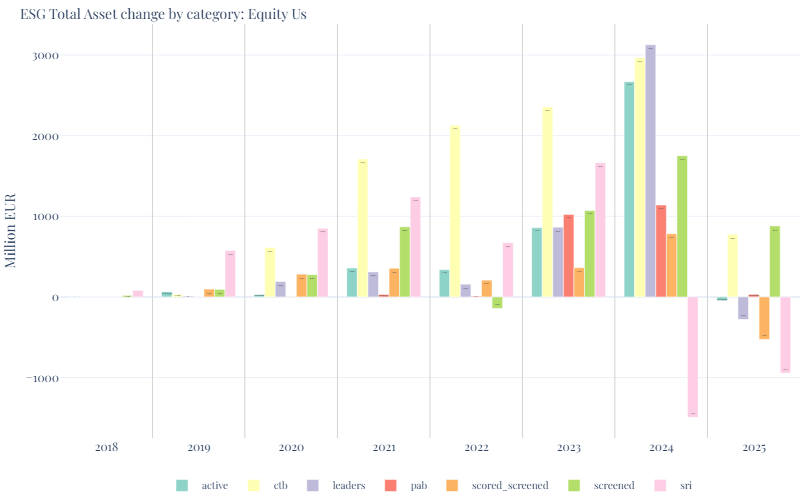

The chart below shows the evolution of assets under management across various categories of ESG ETFs on US equities since 2018. SRI indices led inflows until 2021, when they were overtaken by CTB indices. They held up through 2023, but 2024 saw significant outflows in favour of more flexible strategies, less focused on ESG ratings and more oriented toward exclusions and climate-related factors.

The reasons behind this shift are mainly two. The first is tracking error – the expected gap between portfolios’ performance and their benchmarks: SRI (best-in-class) indices have shown a much larger deviation from market performance than expected – in some cases up to 11.5% year to date – penalising investors when companies with lower ESG ratings (the “laggards”) have outperformed. The second reason lies in the emergence of more sophisticated strategies that offer robust ESG metrics while maintaining a lower tracking error.

Knowing that one’s portfolio does not finance activities contrary to personal values remains a key priority, but it is essential to do so consciously, analysing both methodologies and risks. At Moneyfarm, we continue to monitor ESG strategies available on the market, and our most attentive clients will have noticed this transition within their ESG portfolios, which began as early as 2022.

Our ESG approach

Our ESG portfolios are designed for clients who seek long-term returns without compromising their sustainability values. Since 2020, we have structured our portfolios according to strict criteria aimed at mitigating the risk of greenwashing, as defined in our Responsible Investment Policy.

This policy focuses on mitigating sustainability risks, reducing negative social and environmental impacts, increasing the share of sustainable investments, and enhancing exposure to issuers that demonstrate stronger engagement practices. These objectives should be achieved while taking into account the financial risks associated with ESG integration techniques.

Since 2020, we have observed significant developments in the ETF landscape, particularly in corporate bond markets and within the regulatory framework. These new regulations have improved the understanding of greenwashing and strengthened our framework.

In recent years, our focus has evolved to adapt to market dynamics: the goal is to manage tracking error and enhance exposure to sustainable investments without compromising the portfolios’ sustainability profile.

Our investment process relies on continuous monitoring of available strategies. We analyse methodologies, track performance, and take corrective action when necessary. We use data from leading providers such as MSCI and Bloomberg and maintain ongoing dialogue with ETF issuers. This allows us to select instruments with strong sustainability metrics while also demonstrating greater financial stability.

Our investment team continuously monitors portfolios to understand how performance is evolving, identify the main contributors and detractors, and assess the effectiveness of tactical and strategic decisions. This analysis is crucial in a context where different ESG methodologies can lead to widely divergent outcomes due to the idiosyncratic risks associated with each approach and exclusion policy.

It’s important to actively monitor ETFs and step in when their financial or sustainability performance begins to diverge from expectations.

A look at our portfolio performance

The performance of our portfolios is constantly analysed in both absolute and relative terms, benchmarked against traditional markets and similar ESG funds.

Over the past three years, our ESG portfolios have delivered solid absolute returns, with annual gains ranging from 4.22% for the lowest-risk portfolio to 10.80% for the highest-risk one.

| Portfolio | P1 | P2 | P3 | P4 | P5 | P6 |

| Annual Performance | 4.22% | 5.46% | 6.01% | 7.36% | 8.99% | 10.80% |

From a relative perspective, we compare our performance with ESG funds aligned with our investment policy. Since the definition of ESG is currently very broad, it is not always easy to assess how a fund’s sustainability profile – such as its exposure to fossil fuels or ESG rating – affects its results. For this reason, we set clear criteria to ensure funds are genuinely comparable to our own, allowing us to smooth out differences and focus purely on performance.

To identify a strict subset of ESG peers, we consider only multi-asset funds with a clearly stated ESG policy, excluding those exposed to social controversies such as violations of the United Nations Global Compact. We also include only funds that meet specific improvement thresholds in terms of MSCI ESG ratings, fossil fuel revenues, and carbon intensity.

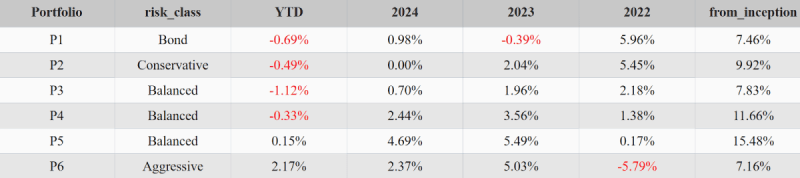

The table below shows the performance of Moneyfarm’s ESG portfolios compared with the median of this group of strict ESG peers, as of 1 October 2025 (net of management fees of the underlying instruments and gross of Moneyfarm commissions). The 100% equity portfolio is not shown because it does not have the same historical data as the other portfolios.

Relative performance since inception (31 October 2021) has been overall positive. The portfolios – particularly those with higher risk levels – have more than recovered the ground lost in 2022, when our stringent fossil-fuel exclusion strategy was penalised by market conditions.

Long-term investing has always been about patience, balance, and confidence in one’s strategy. Embracing ESG builds on the same foundation: it’s an acknowledgment that responsible practices and sound governance are key drivers of enduring value.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.