Retirement planning is no longer something that can be left to chance. With the State Pension age steadily increasing and growing speculation that the triple lock (the government policy that increases the State Pension by the highest of three figures: average earnings growth, inflation, or 2.5%) may be scaled back in future budgets, building your own financial independence has never been more important.

The reality is that relying solely on the State Pension leaves you exposed to government decisions about when you retire, how much you receive, and how comfortably you can live. To have genuine freedom and control, you need to have your own provisions in place: pensions, savings, and investments that work together to create the retirement lifestyle you want.

Whether you’re ten years away or already nearing retirement, this is the time to take stock of where you stand, define what you want your future to look like, and make sure your financial plans can support it.

Here’s what to focus on as you approach your golden years.

1. Understand your provisions: taking stock of what you have

Before you can shape a plan for your future, you need a clear picture of your present. That starts with understanding what provisions you already have in place.

Begin by gathering information about all your pension arrangements, both private and workplace schemes. Over a long career, it’s common to accumulate several small pots with past employers. While each one contributes to your retirement, having them scattered can make it difficult to see the bigger picture. Consolidating these pensions into a single, well-managed plan, such as a Self-Invested Personal Pension (SIPP), can make your finances easier to manage, reduce fees, and give you more control over how your money is invested.

Once you’ve gathered everything, review how each pot is performing and how it’s invested. Are your current holdings suitable for your goals and timeframe? Someone who is 50 years old, and planning to retire at 55 will likely want a more cautious approach to preserve their savings, while someone planning to retire at 65 with a 15-year horizon may prefer a higher exposure to equities for potential growth. Aligning your investments to your retirement timeline is one of the most important, and often overlooked, steps in retirement planning.

But your retirement provisions don’t end with pensions. Individual Savings Accounts (ISAs), investment portfolios, and cash savings also play a key role in creating flexibility and income options. They can be particularly valuable for bridging the gap between early retirement and the pension access age (which will rise to 57 in 2028).

For example, someone planning to retire at 55 may rely on ISA funds or savings to cover two years before their pension becomes available. Similarly, those aiming to retire at 65 will need to plan for the three-year period before the State Pension begins at 68. These personal provisions make it possible to retire on your own terms, rather than waiting for government thresholds to align.

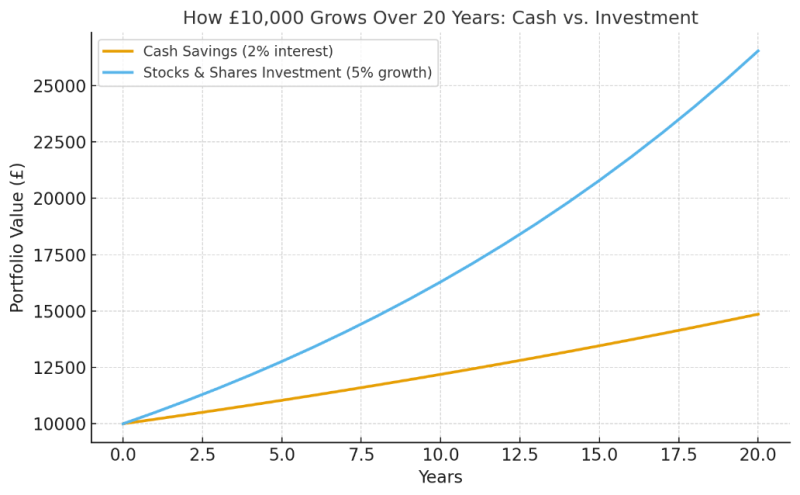

Finally, it’s crucial to recognise the impact of inflation. Keeping large sums in cash over long periods can seriously erode value, especially in a high-inflation environment. While it’s sensible to hold some cash for emergencies, long-term retirement savings are generally better positioned in a diversified portfolio of investments designed to outpace inflation over time.

2. Define your retirement goals: what does a good retirement look like for you?

Once you have a clear view of your financial base, the next step is to define what you’re actually working toward.

Retirement means different things to different people. For some, it’s the freedom to travel or spend more time with family. For others, it’s a chance to volunteer, start a business, or simply slow down and enjoy life at a comfortable pace. Whatever your vision, your financial plan should support it.

Start by thinking about when you’d like to retire and what your ideal lifestyle will cost. Consider your ongoing expenses, e.g. housing, travel, leisure, and healthcare, as well as any one-off goals, like helping children onto the property ladder or moving home. The clearer your vision, the more accurate your planning will be.

Once you’ve outlined your objectives, use retirement forecasting tools or guidance services to project whether your current provisions will be enough to meet them. At Moneyfarm, our Guidance+ service helps clients understand exactly how their existing pensions and investments align with their goals. By analysing your income needs, expected growth, and time horizon, it provides a realistic projection, highlighting whether you’re on track or if changes are needed to close any gaps.

This is where planning becomes empowering. You move from guessing about your financial future to having a clear, data-driven picture of what’s possible and what actions will get you there.

3. Bridge any gaps: strengthening your provisions

If your projections reveal a shortfall between your current savings and your target retirement income, the good news is that there are plenty of ways to address it. Even small adjustments made now can have a meaningful impact later.

You might choose to increase your pension or ISA contributions, even modestly. Thanks to compounding (the process of earning returns on both the initial and the accumulated interest over time), extra savings made in the years leading up to retirement can significantly boost your eventual pot. Alternatively, you may want to review your investment mix, ensuring your portfolio still reflects your goals and tolerance for risk.

Clearing debts, especially mortgages or personal loans, can also strengthen your financial position, freeing up more income when you retire. And in some cases, you may decide to delay retirement slightly or phase it gradually, working part-time before fully stepping away from employment. This not only extends your earning years but shortens the period your pension and savings need to cover, a powerful combination for improving long-term sustainability.

Every individual’s solution is different, but the principle is the same: identify the gap early, and take proactive, measured steps to close it.

4. Keep your plan under review: adapting as life and legislation change

Retirement planning isn’t something you set and forget. It’s a dynamic process that should evolve as your life, finances, and government rules change.

Markets fluctuate, tax rules are revised, and personal priorities shift. That’s why it’s important to review your plan at least once a year, checking whether your goals are still the same, your investments remain appropriate, and your provisions continue to perform as expected.

Regular reviews also allow you to stay ahead of potential changes, such as adjustments to the State Pension age or tax thresholds. Being proactive keeps you in control, ready to adapt, rather than forced to react.

5. Think beyond finances: building a life that’s meaningful

It’s easy to focus purely on numbers, but a fulfilling retirement is about much more than money. Financial independence is the foundation, but what it enables, time, freedom, choice is what truly defines your golden years.

Consider how your retirement plans support your wellbeing, sense of purpose, and quality of life. Are you budgeting for activities that bring joy and fulfilment? Have you thought about future healthcare costs or long-term care? Planning for these realities helps ensure your financial freedom translates into real-life security and happiness.

When your provisions and goals are aligned, you can look forward to retirement not with uncertainty, but with confidence, knowing you’ve built a future that reflects what matters most to you.

The bottom line

As you approach retirement, your focus should shift from simply saving to shaping your future. Understanding your existing provisions, setting clear goals, bridging any shortfalls, and reviewing your strategy regularly ensures you remain in control, regardless of policy changes or market movements.

At Moneyfarm, we help investors turn retirement ambitions into actionable plans. Through services like Guidance+, we offer the clarity, insight, and confidence you need to approach your golden years on your own terms, secure, prepared, and ready to enjoy the life you’ve worked so hard to build.

Please remember that when investing, your capital is at risk. The value of your portfolio with Moneyfarm can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. The views expressed here should not be taken as a recommendation, advice or forecast. If you are unsure investing is the right choice for you, please seek financial advice.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.