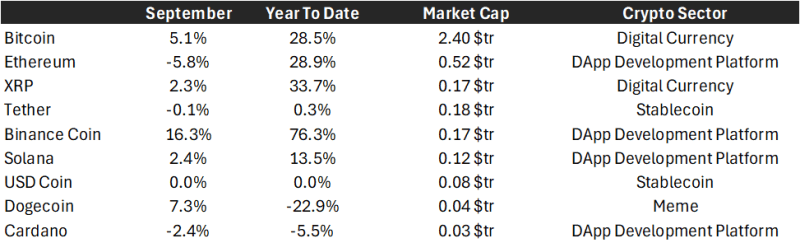

September presented a reversal of the divergent performance seen last month across digital assets. Bitcoin showed strong resilience, once again leading the market as it has done in the past.

At the same time, Ethereum’s recent period of outperformance concluded, aligning with historical patterns of cyclical volatility.

Macroeconomic conditions looked supportive for assets like Bitcoin, and while the Federal Reserve (Fed) delivered a 25–basis–point rate cut, its impact was limited since markets had already priced it in.

In addition, the growing uncertainty in the final week of the month over a potential US government shutdown raised concerns about fiscal stability and global confidence in the dollar. This fed into the broader “dedollarization” narrative – the idea that investors may increasingly seek alternatives to the US dollar – which continues to support the macro case for Bitcoin.

On a micro–level, positive news flow provided a significant tailwind for specific ecosystems. The Binance ecosystem, in particular, benefited from strong fundamental developments, which was directly reflected in the robust performance of its native asset.

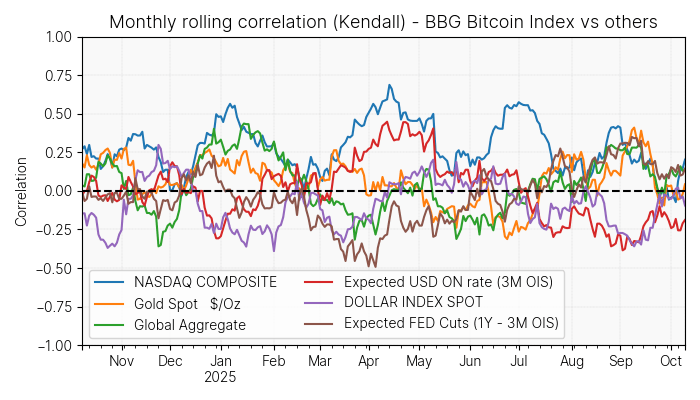

Correlations that matter

In September, Bitcoin exhibited a significant decorrelation from major asset classes, as illustrated in the chart below. A brief spike in its correlation with gold quickly reversed, as the precious metal rallied while Bitcoin’s price stalled. Meanwhile, its relationship with the US dollar moved towards zero from a previously negative correlation, reflecting subdued volatility and a lack of clear direction in foreign exchange markets.

A slight negative correlation with short–term US rate expectations persisted – a noteworthy dynamic, as Bitcoin tends to increase when the rate moves lower.

Ultimately, this broad decorrelation makes sense in a month where micro–level catalysts, rather than macro trends, drove performance. This pattern further supports our view of Bitcoin as a decorrelated asset.

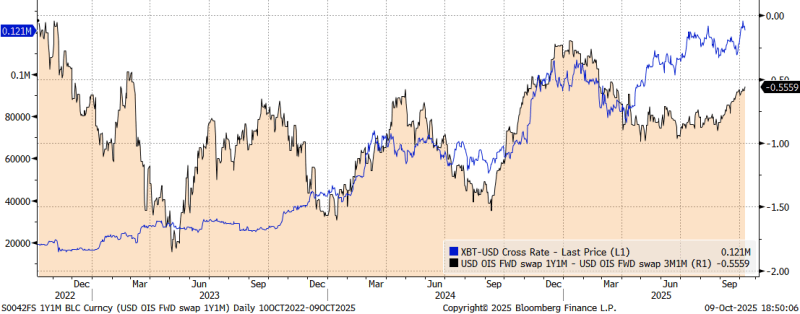

The macro: beware the meme

A common meme in crypto circles depicts Fed Chair Jerome Powell at a money–printing machine, implying that increased dollar printing will automatically boost crypto prices.

The reality, however, is more complex. To explain this, we compared Bitcoin’s price (blue line) with a proxy for the expected path of monetary policy (black line): the spread between two Overnight Index Swaps (OIS), which specifically reflects the market’s expectations for future Fed rate changes.

When the spread rises, it means markets expect tighter monetary policy – either interest rate hikes or fewer rate cuts. When the spread falls, it signals expectations of looser policy – more rate cuts or continued stimulus.

In theory (and in the meme), “money printing” or looser policy should be good for crypto. However, the data tells a different story. Over the past two years, Bitcoin has often rallied when markets were expecting tighter policy, not looser. This is the opposite of what the meme suggests.

Even the most recent rally happened during a period when expectations shifted slightly toward tighter policy, although the latest Fed cut may distort the data slightly. Some might say this is linked to inflation concerns, but the evidence is still inconclusive.

This analysis shows it is still premature to draw firm links between macroeconomic variables and Bitcoin’s price.

Price movements show that regulatory and industry–specific events have had a much stronger impact on digital assets than macroeconomic variables. Some of the key drivers include the approval of US spot Bitcoin ETFs in spring 2024, which allowed mainstream investors to access Bitcoin through traditional investment platforms for the first time; the US election results in November 2024, which shifted expectations around future regulation and economic policy, and the reversal of tariff policies in March 2025, which triggered a broader “risk–on” sentiment across markets.

In this context, new regulatory developments – such as the preview of the GENIUS Act, a proposed US framework for stablecoins – could prove even more important for the digital asset space going forward.

The Micro

At the micro level, several key narratives influenced the market in September and early October. These developments revealed a tug–of–war between different types of investors – such as long–term holders taking profits and institutions buying in – while still pointing to a generally supportive environment for crypto assets.

- On-chain dynamics – a tug-of-war: A primary on–chain theme was the conflict between long–term holders taking profits and institutions accumulating. Significant selling pressure from “whale” wallets, which had distributed approximately 150,000 BTC since late August, finally began to dissipate. Glassnode data confirms this, showing a decline in transfers from “whales” to exchanges, implying selling pressure is easing.

This distribution was also visible among the broader cohort of long–term holders (wallets holding >155 days). Acting as a powerful counterforce, institutional accumulation continued unabated.

The Bitcoin supply held by public companies and ETPs (exchange–traded products that give investors exposure to Bitcoin without holding it directly) steadily climbed, accounting for nearly 12.5% of the total and absorbing liquidity from sellers. - Ecosystem focus – Binance and user activity: Activity within specific ecosystems remained a critical performance driver. For example, the BNB Chain – a blockchain network originally developed by Binance – continued to attract attention after a surge in activity on its decentralised derivatives platforms, where users can trade or hedge without intermediaries.

This highlights a market increasingly focused on ecosystems that can demonstrate tangible user activity and sustainable transaction volumes, rewarding them with capital inflows. - The regulatory horizon – The GENIUS Act: On the regulatory front, the market continued to digest the preview of the GENIUS Act. This proposed framework for stablecoins by the US Treasury is a landmark development. By creating a clearer regulatory pathway, the Act could bolster a foundational component of the digital asset ecosystem, potentially reducing systemic risk and encouraging further institutional adoption.

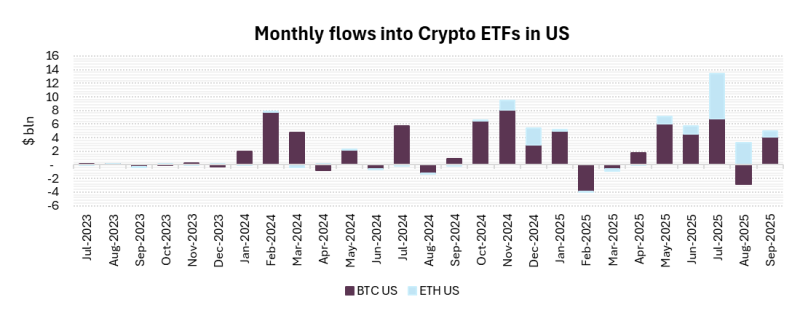

The flows

Investment flows in September mirrored the market’s divergent performance, showing a clear rotation of capital between the two major assets.

After a period of strong demand, inflows into Ethereum–focused products (ETH) returned to more normal levels, as illustrated in the chart below.

Meanwhile, Bitcoin (BTC) investment vehicles rebounded, drawing renewed interest following a weaker performance in August.

Despite this rotation, aggregate capital flows into the digital asset class remained robust. While the pace has become more moderate and sustainable, the overall trend still points to sustained investor demand.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.