The Bank of England left its policy rate unchanged this week, a widely expected move given that inflation remains some way above target (3.4% year on year vs the Bank’s 2% target). That won’t be much comfort to borrowers, however.

Policymakers continued to highlight that risks to inflation remain “two-sided” – meaning it could come in either higher or lower than they would like – while also noting significant geopolitical uncertainty. At the same time, the voting patterns from the members of the rate-setting committee indicated a tilt towards lower rates in the future. In May, two members voted to hike rates, two voted to cut, and five voted for no change. In June, six voted for no change while three voted to cut. With weaker macro data coming through, rate cuts in the coming months seem likely.

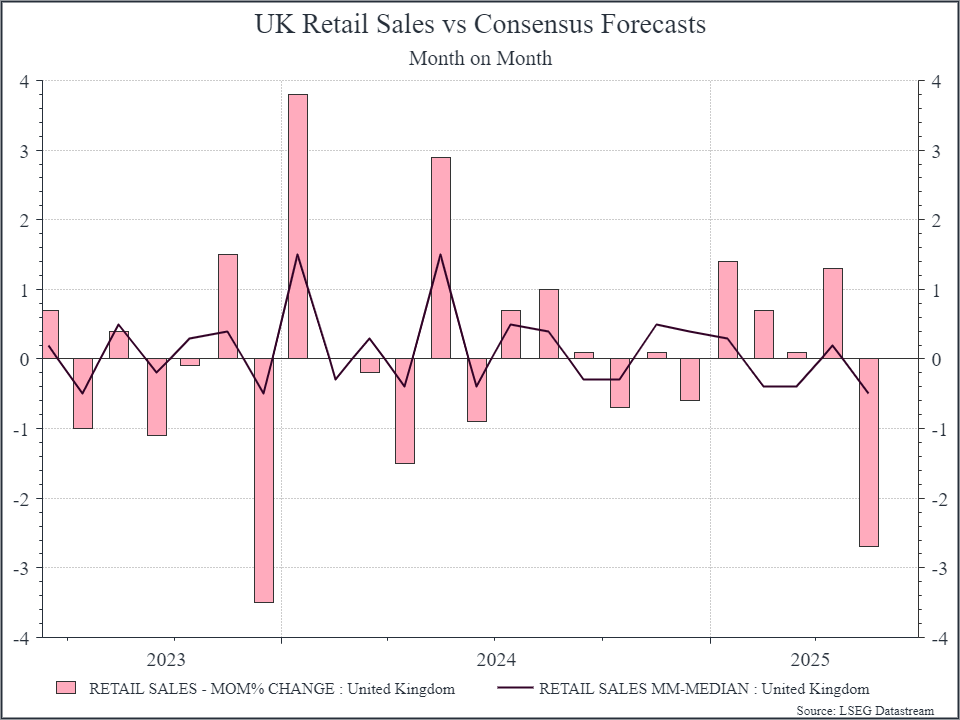

There probably isn’t going to be much prospect of a summer respite for UK policymakers. UK retail sales for May were well below expectations, down 2.7% month on month, as you can see in the chart below. Government borrowing for May also came in slightly worse than expected, at around £17.7 billion. After a slight contraction in the economy in April, these data suggest we could see more of the same in May.

All this leaves the Chancellor with a set of difficult decisions ahead of the Autumn budget statement. We’d expect to see taxes increase in some way, but precisely how is less clear.

It’s clearly difficult to assess how higher taxes might change the behaviour of higher-income tax payers. It’s too soon to tell, but there are news reports around a potential roll-back of some parts of the new inheritance regime. That might just be wishful thinking for some, but it does suggest that the impact of those changes on the wealthiest and most mobile of UK tax payers has been greater than the government had anticipated.

What does it mean for portfolios? The challenges that the UK faces are quite well understood. We’d argue they are at least partly reflected in starting valuations, and we continue to maintain positions in UK equities and UK government debt.

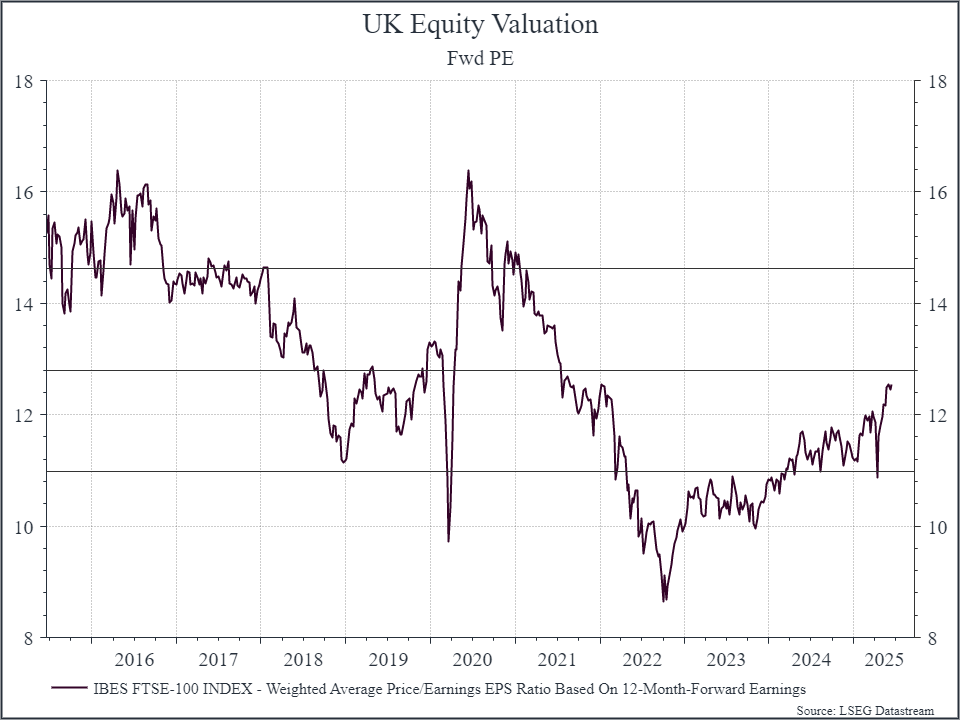

Amid the generally negative tone, it’s notable that UK equity valuations have generally drifted higher from the lows of the Truss mini-budget in 2022. The chart below shows the forward price earnings ratio of the FTSE 100 over time. Valuations are only a little below their ten-year average – at least on this metric.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.