At Moneyfarm, one of the most common questions we get is whether it’s better to invest or to save. For the avoidance of doubt, this article uses the term ‘save’ to refer to money deposited into savings products or accounts, like cash ISAs.

While both are crucial components of a solid financial strategy, the answer depends largely on your financial goals, risk tolerance, and time horizon. Many of us should likely be using a combination of strategies to meet our various needs. Many of us will have multiple and different goals with varying time-horizons; we might have short-term liabilities like a deposit on a property, whilst also having longer-term goals like saving towards retirement.

ISAs: tax-free returns

Whether you’re looking to save or to invest, doing so through a tax-efficient wrapper like an ISA is a fantastic place to start. The ISA was introduced in April 1999 and allows UK residents to save or to invest via an account ‘wrapper’ which means the account holder is not liable to paying tax on the saving or investment returns.

When you save outside of an ISA, you may be liable to paying income tax on the interest generated over your personal savings allowance (PSA).

When you invest outside of an ISA, you may be liable to paying income tax on interest earned, dividend tax on dividends received, or capital gains tax on profits made.

Using ISAs for saving and investing can therefore improve your net-returns after tax.

For example, someone who earns more than £50,270 will be a 40% rate tax-payer. Interest which they generate on their savings and investments, over and above their personal savings allowance (PSA) of £500, will be taxed at 40%. If they put £20,000 into a one year fixed-term savings account paying 4.5% AER, their deposit will return interest of £900 after one year. If their PSA is £500, then £400 of that return is subject to income tax at 40%. This means they are liable to paying £160 of income tax on that money, meaning their £900 return is actually £740 after tax. In percentage terms, this means that their 4.5% rate is actually a net return of 3.7% after tax. In an ISA, all of that £900 is tax-free, and will stay tax-free in their ISA, ie. you can roll-up the interest earned and begin to compound it within the ISA itself.

The benefits of Cash ISAs

Saving money is all about building a safety net for emergencies and shorter-term goals. It’s a low-risk option where your primary objective is likely to protect your capital, i.e. to avoid a nominal reduction in the value of your funds. Savings accounts and Cash ISAs can offer flexibility and peace of mind in knowing that you’re very unlikely to get out less than you put in, though they typically provide lower returns than investment products over the longer term. For someone who is trying to build an emergency fund, or saving for a large expense within the next few years, saving is a smart choice, particularly whilst rates are quite high relative to recent history.

While savings products are generally seen as low-risk—meaning the nominal value of your funds remains stable, they are not entirely risk-free. One key consideration, often overlooked by savers, is the potential loss of purchasing power due to inflation. If the inflation rate exceeds the net return on those savings, the real value of your money decreases over time. Inflation has become a more relevant factor in recent years, particularly after the multi-decade high levels seen in 2022, which persisted longer than many would like.

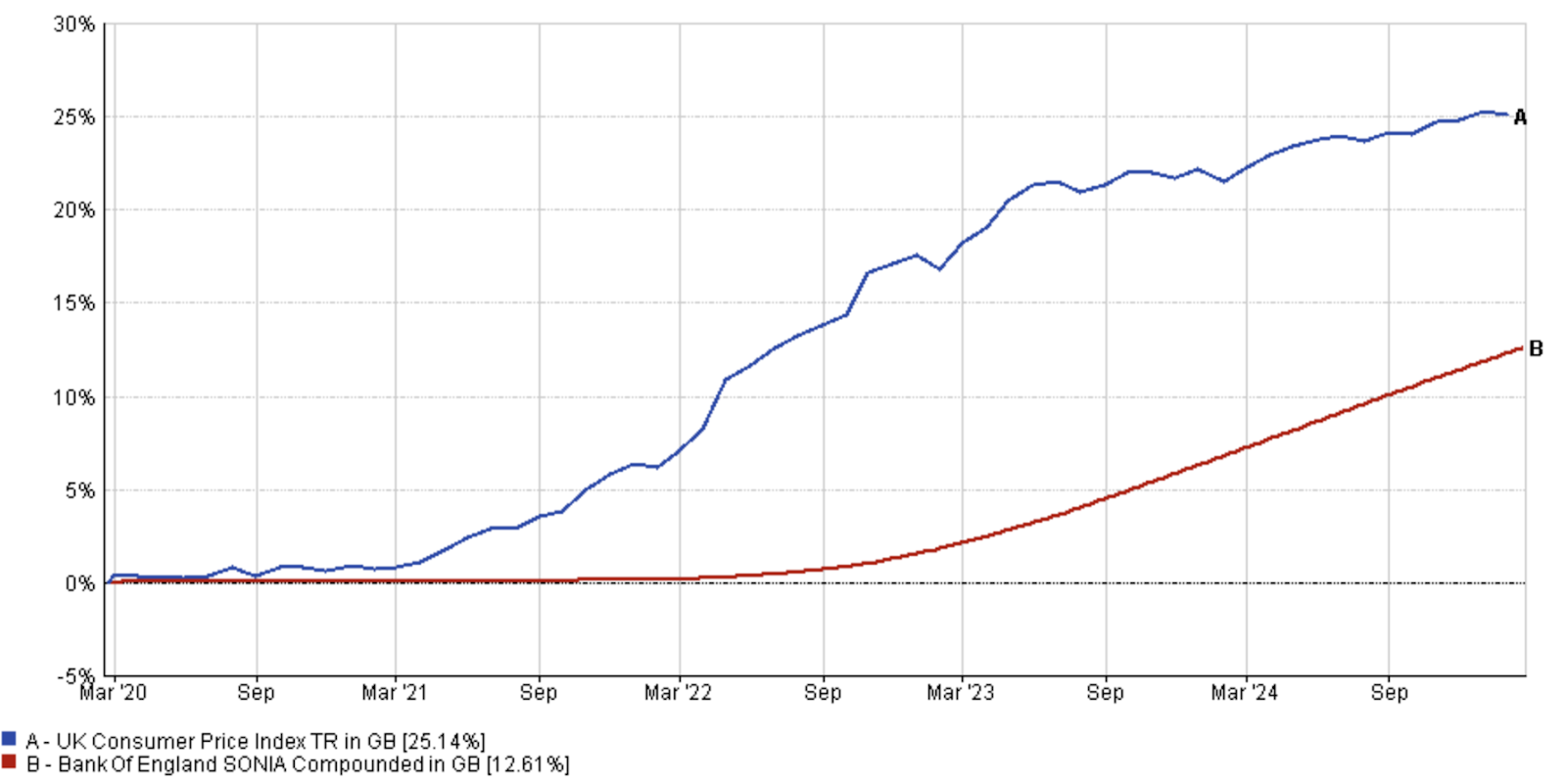

The below chart plots the UK Consumer Price Index (CPI) in blue – which is the primary measure of inflation, against the SONIA (sterling overnight index average) in red – a key measure of interest rates as defined by the inter-bank borrowing rate. Both of these indexes show rolling returns; they account for the compounding effects of time periods over the last five years (since 21/02/2020).

(Moneyfarm Analysis, Data Source: FE Fund Info)

What’s pertinent here is that CPI has increased by some 25% over the last five years, where the compound returns from SONIA have increased by some 12%. SONIA isn’t a perfect measure of the actual savings rates that a retail investor might have obtained, but it does a good job of illustrating that interest rates (and therefore savings rates) have not matched inflation over the last five years. In short, unless your savings and investments have returned more than 25% over the last five years, they have fallen in real-terms value.

Investing: growing your wealth over time

Investing, on the other hand, is designed for growing wealth over a longer time frame. Whether it’s stocks, bonds, real estate, or investment funds that expose you to multiple asset classes, investing generally offers higher returns than savings accounts, but it comes with greater risk. Investing is ideal for those looking to build wealth for retirement and other long-term financial goals.

There are several risks to investors, but the key risk for most is usually volatility, i.e. that the value of your investments will fluctuate both up and down, such that you may get out less than you originally put in. Volatility refers to both upside and downside price fluctuations, so is not innately good or bad; rather, the higher the volatility of an investment, the higher the potential gain or loss could be.

Volatility can be managed with a sound investment strategy and asset allocation; certain asset classes are more volatile than others. The amount of volatility we can afford to stomach is largely determined with our time-horizon; a 30 year-old investor with a multi-decade time horizon on their pension can inherently afford more volatility than someone saving for a house purchase in two-years, for example. Volatility, and in particular, the downside risk of investments falling in value, can also be naturally mitigated over time. Markets go up and down in cycles, but the long-term trend is that global markets increase in value; a well-diversified portfolio of assets is increasingly unlikely to generate negative returns as time goes on. Let me provide an example below.

In financial markets, we often refer to market sentiment as being ‘bullish’ (optimistic) or ‘bearish’ (pessimistic). Let’s define a market which has risen by 20% from its last trough as a ‘bull market’, or a market which has fallen by 20% from its last peak as a ‘bear market’. Historically, on average, bull markets last for 6 years and 10 months, where bear markets last for 1 year and 3 months, according to research from Vanguard Asset Management 2024. This is to say that in general, markets spend more time going up than they do going down. Therefore if you spend long enough in the market, you’re unlikely to see a nominal loss on your investment. Therefore, investing with a longer time horizon is likely to both reduce the risk of losses, whilst also increasing your expected returns through a higher-risk (more volatile) investment strategy.

Savers vs investors: who wins?

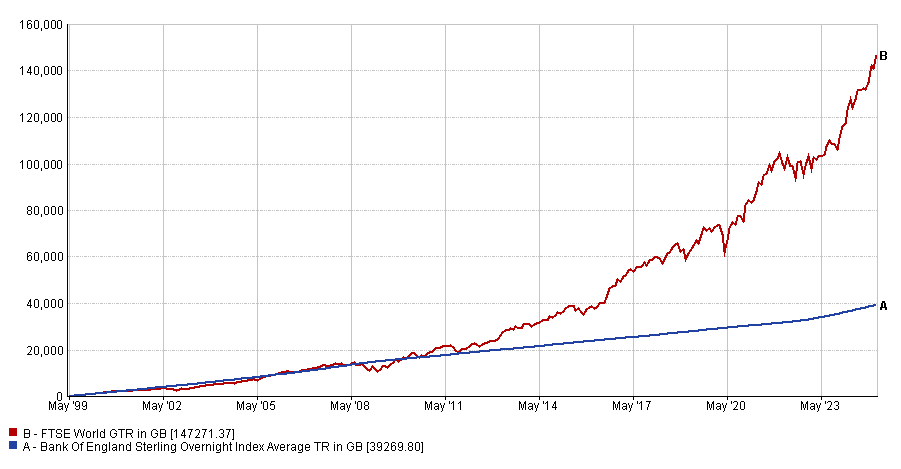

In April 2024, the ISA celebrated its 25th anniversary. I think it’s worth taking a look at the last 25 years of data to compare returns that investors and savers might have achieved in that time.

For the purposes of comparison, let’s assume that you have spent the last 25 years contributing £100 a month to both a Cash ISA and a Stocks and Shares ISA (from the ISA inception on 06/04/1999 until 31/01/2025).

To simulate historical returns in a cash ISA, we will use the SONIA (sterling overnight index average) in blue – a key measure of interest rates as defined by the inter-bank borrowing rate. To simulate historical returns in a Stocks and Shares ISA, we’ll use the FTSE All-World composited index in red – a market index tracking some 4000 global stocks. Both of these indexes show absolute rolling returns; they account for regular contributions plus the compounding effects of time periods over the last 25+ years (since 06/04/1999). In this scenario, you have contributed £100 a month to both of these pots, on the 6th of each month. Therefore, you have made total contributions of £31,100 towards both pots since inception.

Source: Moneyfarm Analysis, Data Source: FE Fund Info.

In the above scenario, total returns in your Cash ISA would be equal to £39,268.80 whereas the equivalent contributions towards a FTSE World index-tracking fund might’ve grown to a value of £147,271.37 in the same time-frame.

The chart also illustrates the benefits of taking a long-term view of your investments; as a spot of historical context, entering the markets in 1999 would’ve resulted in a tumultuous start to your investment journey, right as the infamous ‘dot-com’ bubble was beginning to burst, and equity markets crashed. Markets began to recover within a couple of years, only to eventually crash again in the even more infamous global financial crisis (GFC) of 2007/08. With two major market crashes accounted for, global equity markets broadly generated returns in-line with interest rates for the first 10 years of this chart roughly, and it isn’t until the post-GFC era of the 2010s, characterised by low interest rates, until market returns begin to meaningfully diverge from returns obtainable in the savings markets. Two and a half decades later, the power of remaining invested and making regular contributions manifests itself in compounded returns in the equity markets, the likes of which would have provided you with far greater capital growth than you would’ve obtained in savings products.

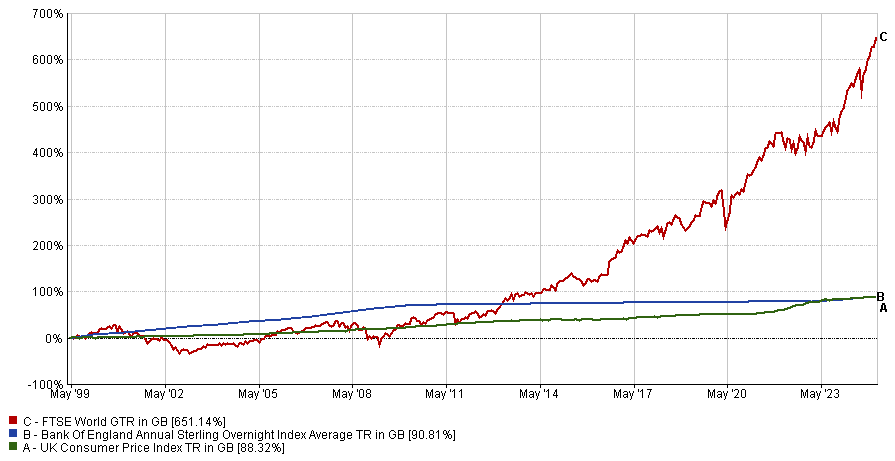

I think it’s also worth viewing this chart in the context of inflation too. Let’s plot the two same indexes against each other again, and this time include a third index: the Consumer Price Index (CPI), the preferred indicator of inflation. Given the CPI is not an investible index, let’s not account for any contributions, and instead look at absolute returns in % terms.

Source: Moneyfarm Analysis, Data Source: FE Fund Info.

I find this a particularly pertinent image. In absolute terms, the FTSE World (global equity) index has grown by 651.14% over the last 25 years; the SONIA (interest rates) index by 90.81%, and the CPI (inflation) by 88.32%. In other words, over the past 25 years, savings rates have just about beaten inflation. By contrast, If you’d invested in global equities, you would have outperformed inflation by roughly 7.4 times. It’s also worth noting that as seen on the chart around 2022, your real-returns in savings (ie. returns over and above inflation, plotted in blue) is quickly eaten away by a year or two of abnormally high inflation levels. To me, this highlights the importance of considering inflation when deciding how to allocate your money over the long term.

The bottom line: striking a balance between both

Rather than choosing one over the other, the optimal strategy likely involves a combination of both saving and investments. As a general rule of thumb, it’s prudent to have between 3-6 months of regular expenses saved in a liquid, low risk savings account so that you have some financial windfall in the event of any financial setbacks like job loss, or an unexpected expense. If you have meaningful liabilities or expenses planned for the shorter term (1-3 years), it may also be prudent to keep these funds saved in lower risk products like savings accounts, to minimise the risk of financial loss. Remember, your financial situation is unique, and there’s no one-size-fits-all answer. For many, the prevailing interest rates available will also make an impact on your strategy; if interest rates are high, there is more incentive to save, and vice versa. Assess your goals, risk tolerance, and time horizon to determine the best balance for you.

Beyond that, it’s clear that if part of your financial goal is to save for the long term, and indeed to focus on capital growth and/or beat inflation, you’ll want to have investments too. As we’ve observed above, savings are not without risk; the risk of not beating inflation is a very real probability, particularly when inflation is relatively high. This is precisely why your workplace pension schemes are invested for you, and do not just sit generating interest; over the very long term (potentially decades), investing in global markets is one of the best ways for individuals to grow their wealth, and therefore reduces the risk of your wealth being eaten away by inflation over time.

At Moneyfarm, we now have products to help you meet your various goals. Our new Cash ISA is perfect for those with shorter-term goals, looking for flexibility and liquidity, whilst generating income on their money.

For those with greater risk appetite or long-term financial goals, Moneyfarm manages a whole variety of diversified portfolios, at different risk levels, to help meet your various goals. Best of all, almost all of these products are eligible to be held in a variety of wrappers, whether that’s a Stocks and Shares ISA, a Junior ISA, a self-invested personal pension (SIPP), or a General Investment Account, or a combination thereof.

As always, if you wish to discuss any one of our products or services, please book an appointment with our friendly investment consultant team.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.