Government bond yields in the UK have been rising over the past few weeks and we wanted to dig into this a bit more.

We’d argue there are a couple of important drivers behind these movements. First, the impact of inflation and Central Bank interest rate policy. Second, the outlook for fiscal policy and government borrowing. As you’d guess, these drivers aren’t independent and interact with each other.

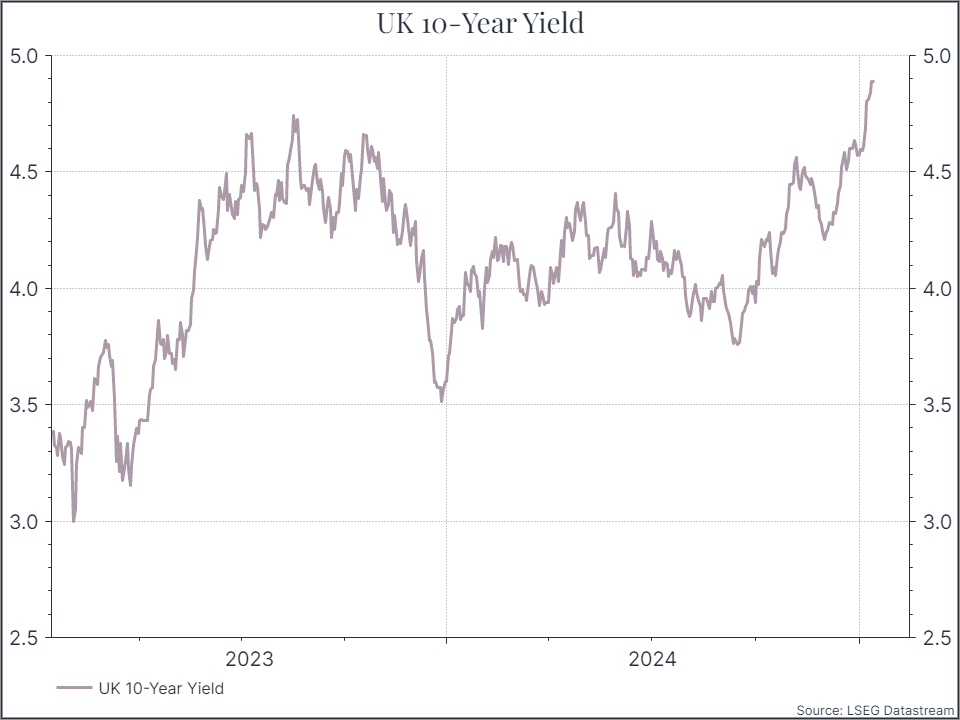

First, let’s look at how government bond yields have behaved over the past few weeks. The chart below shows the UK 10-year yield, which has moved from below 4% in September 2024 to close to 5% in mid-January 2025. That’s a fairly sharp move, but not unprecedented.

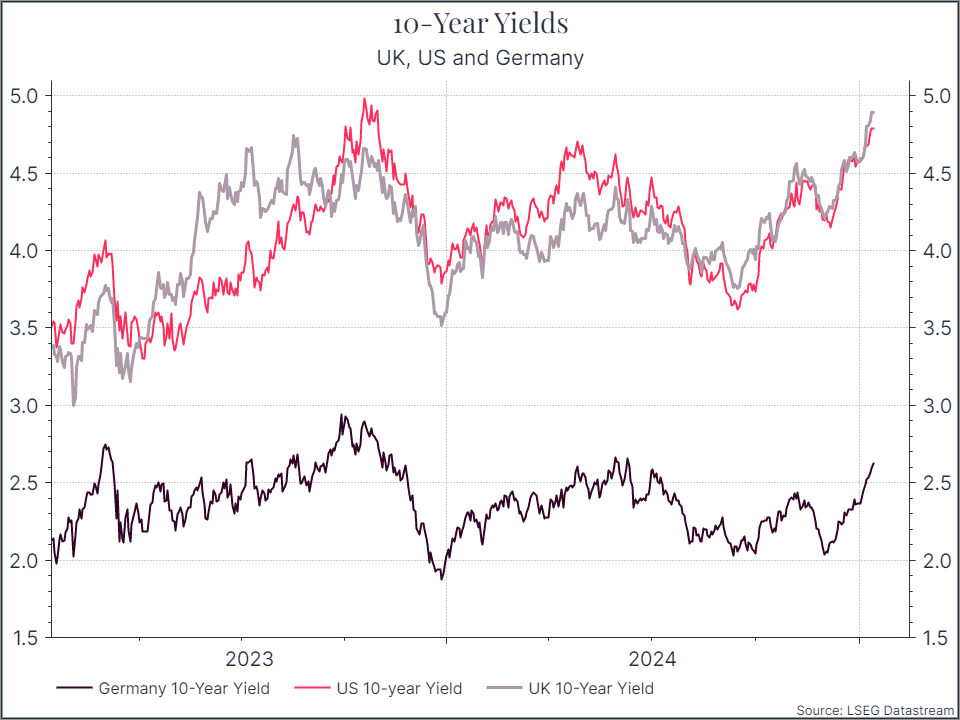

It’s also worth highlighting that this move is not unique to the UK. The chart below compares the US, the UK and German 10-year yields. All three have seen yields rise over the past few weeks.

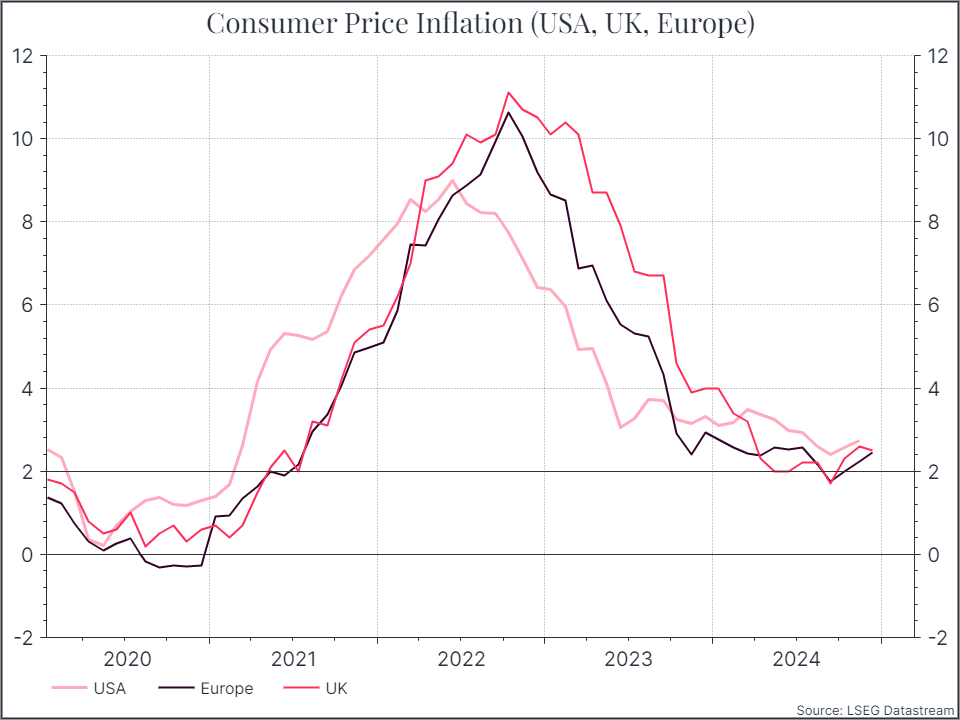

Let’s turn to inflation. We’ve seen annual inflation fall steadily since the recent peak in late 2022, and that has prompted the US Federal Reserve, the Bank of England and the ECB to lower their policy rates. Inflation has come close to the 2% target that the Bank of England usually focuses on (see chart below), but over the past couple of months it has stopped decelerating.

With lower policy rates, still-decent wage growth and a relatively low unemployment rate, some investors are concerned that inflation could re-accelerate over the coming quarters. In that context, the equation becomes simpler: lower inflation means lower yields and vice versa. That’s what we saw after the better-than-expected inflation figures in the UK last Wednesday.

The second part is around the fiscal accounts. A high tax burden, rising debt to GDP and anemic growth are a tricky combination. And a higher cost of debt will exacerbate that, eating into the fiscal headroom that the Chancellor had left in her last budget.

Digging into the details a bit, we can see in the chart below that public sector borrowing is running a bit less than 5% of GDP at present.

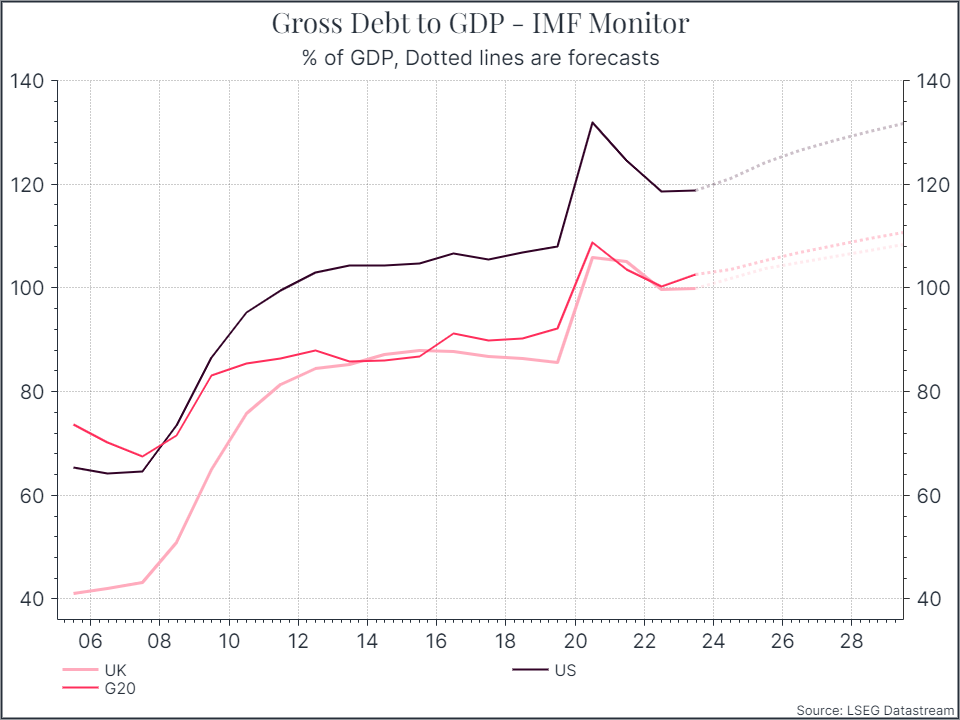

That gap has helped to increase debt to GDP over time for the UK and, according to the International Monetary Fund (IMF), it’s expected to continue. Again, this isn’t great news, but it’s also not specific to the UK. The chart below shows similar figures for the US and the G20 overall.

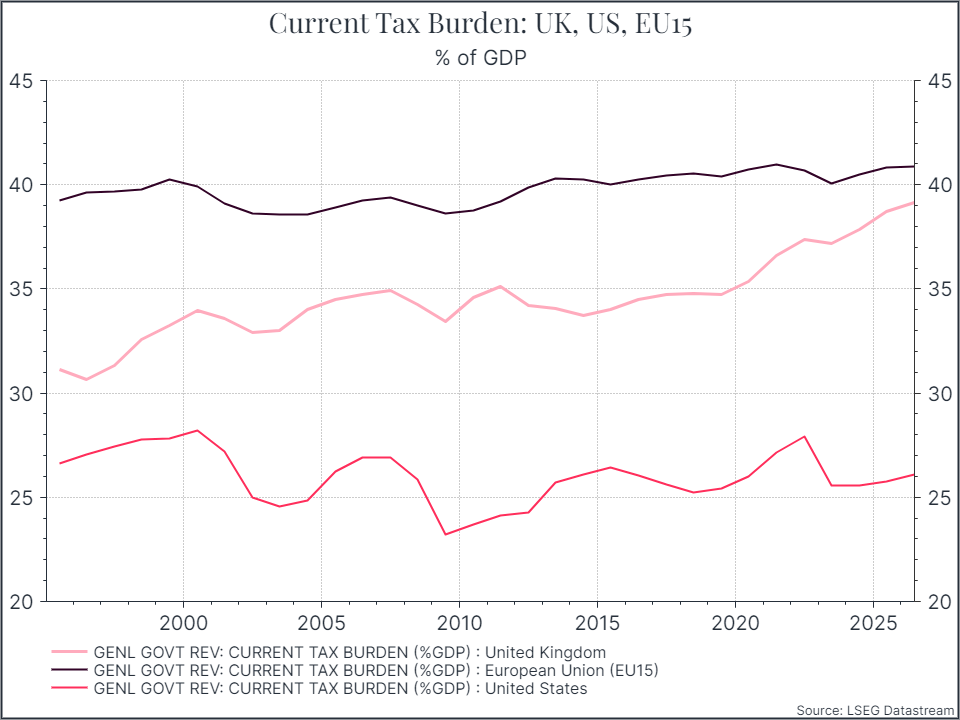

When we look at estimates for the overall tax burden, the UK does show a different path to some of its peers. The chart below shows taxes as a percentage of GDP for the US, the UK and the EU15. We can see that the UK has seen its tax burden increase far faster than the other two regions over the past thirty years.

And this explains the Chancellors focus on growth. There’s probably not that much room to squeeze more out of the UK tax payer. The ideal option is to make the pie bigger for everyone but, as we’ve noted before, UK growth has been pretty anaemic – certainly compared to the US (see chart below).

So where does this get us? We know that the UK government has a tough hand to play, and it’s not alone. At the same time, it seems that bond investors collectively are ready to demand a higher return to lend to the UK, and other markets. We think that reflects concerns on inflation re-accelerating in the short term and questions about how much government debt will rise in the longer term.

From a portfolio perspective, we’ve seen longer-dated bonds decline in value over the past few weeks.

While we acknowledge the challenges that governments face in many developed markets, we do think that the yields we’re currently seeing largely reflect those concerns and look interesting from a long-term perspective.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.