We’re reaching that point in the year where many of us take stock – what we’ve achieved, what we’ve learned, successes and failures. On the Asset Allocation Team, we’ve been debating the lessons of 2024 and, perhaps more importantly, whether or not those lessons are applicable to 2025 and beyond.

1. Don’t bet against the US

The chart below shows the performance of equity ETFs for the US, Europe ex-UK and the UK. The message has been pretty clear – US tech has led the way this year and the S&P 500 has trounced global indices.

Of course this isn’t a new lesson. The chart below shows the performance of the same ETFs over the ten years ending December 2023. US outperformance isn’t just a 2024 story.

But it’s not quite as simple as saying US equities against the world. It’s really been large US companies that have set the tone in 2024. The chart below shows the performance over the last couple of years of US large capitalization companies compared to their smaller peers, and Europe equities. US large caps have outperformed. European stocks have generally held their own against smaller US equities over the past couple of years.

2. Valuation isn’t a short-term signal

This is more of a reminder than a lesson, given that it’s a key part of our Strategic Asset Allocation process, which looks at long-term valuations and 10-year expected returns.

The chart below shows the relative valuation (forward Price/Earnings ratio) for the S&P 500 compared to European equities. Over the past ten years, the valuation of US equities has steadily risen compared to Europe, and that continued in 2024. Waiting for those valuations to converge has been painful for many investors.

3. Politics still matters for financial markets

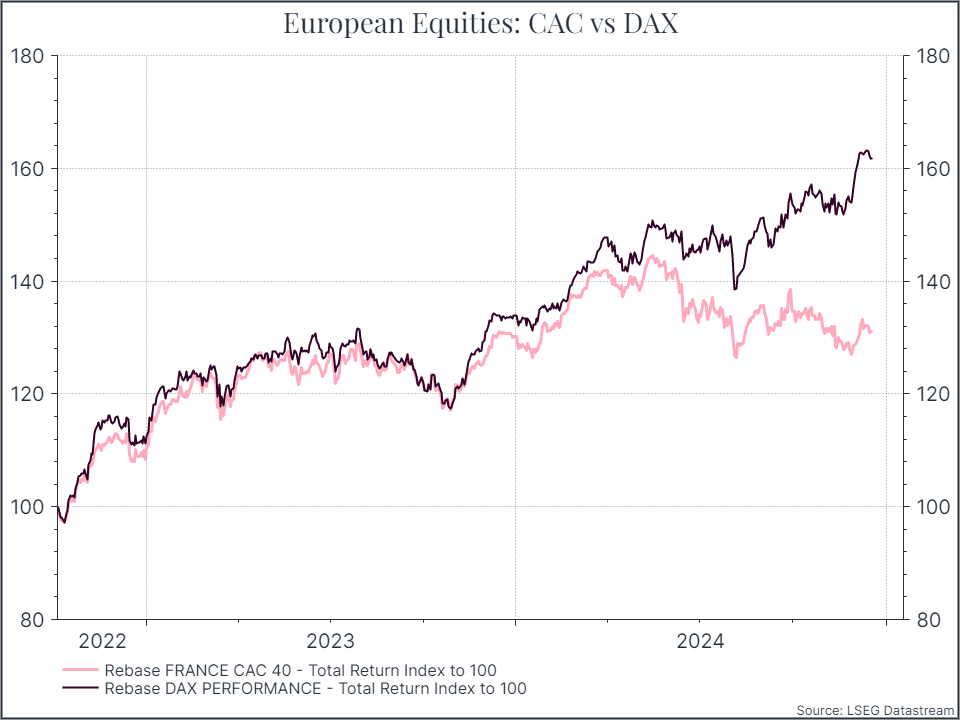

2024 saw more reminders about the role that policy and politics can play in financial markets. The chart below shows the relative performance of German and French equities over the past couple of years. The snap election called by President Macron in mid-2024 prompted French equities to underperform for the remainder of the year.

Bond markets told a similar story. The chart below shows the difference in the yield on German and French government bonds over the past couple of years. The elections impact on the cost of French debt is pretty clear and ongoing.

It was a similar story in the US. The prospect, and then the reality, of a Republican victory explains much of the outperformance of US equities over the second half of 2024.

4. Beware the herd but don’t panic

Sometimes you discover that lots of investors are positioned the same way – and have borrowed to increase their positions. Often you discover that when they all try to exit their positions at the same time. In August, changes in Japans monetary policy helped to prompt a really sharp drop in Japanese equities. That drop had an impact on US markets as well (see chart below).

But as the chart shows, often the best thing for the long-term investor to do is nothing at all. The market volatility was dramatic for a few days, but on this occasion it was relatively short-lived

Those are some of the “lessons” we learned in 2024. But they’re not absolute truths. There is no law that US equities must always outperform or that valuations never matter – probably the reverse. And so, large US companies continue to generate strong growth and robust profits, but their valuations do reflect some of that strength. And while it seems fair to assume politicians and Central Bankers will continue to drive markets in 2025, it’s notable that equity markets have continued largely to look past all the geopolitical uncertainty of 2024. So, with so much uncertainty and so many moving parts, we return to the core tenets of our approach – a long-term horizon, a well-diversified portfolio and focus on managing risks through the ups and downs of financial markets.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.