Headline inflation hovers close to the 2% target in many developed economies, and that has prompted central banks to start lowering interest rates. But the outlook for inflation remains quite uncertain and could prove to be an important driver for policymakers and markets as we head into 2025.

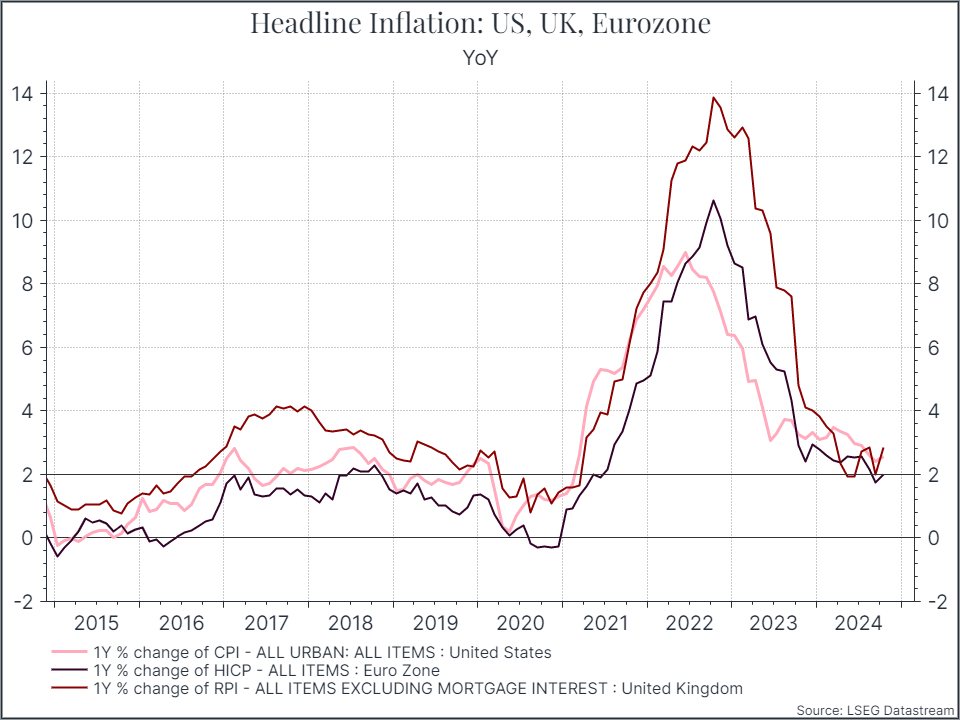

The chart below tells an optimistic story, showing headline year-on-year inflation for the UK, the US and the EU close to target.

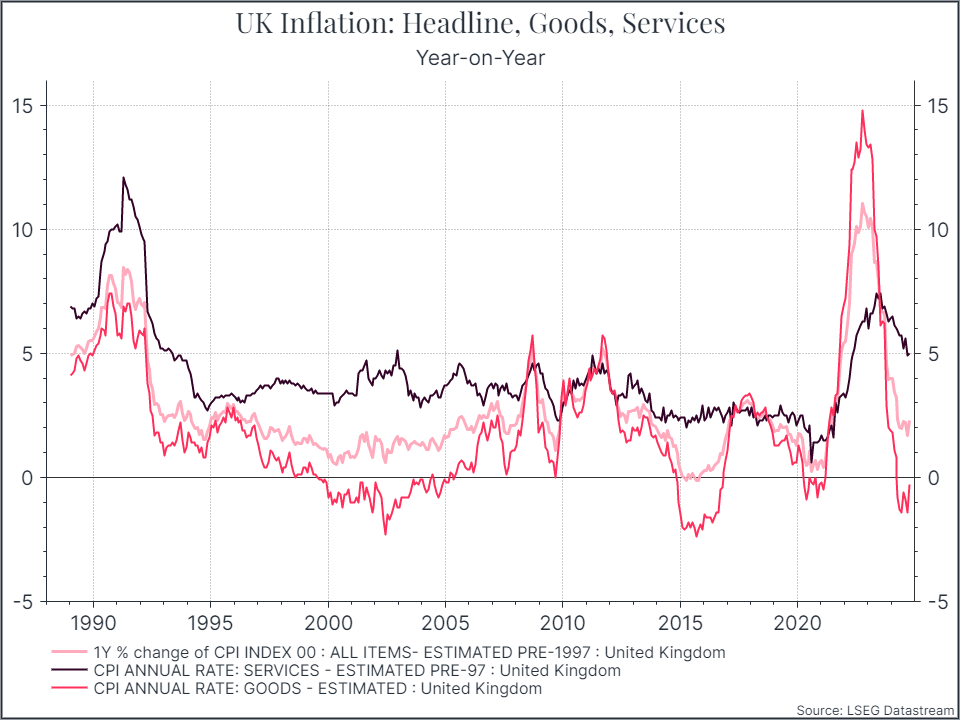

If we dig into the composition of inflation a bit more, we can see that it’s slowing goods inflation that has been behind most of the improvement. The chart below shows year-on-year inflation for headline inflation, along with goods and services, for the UK. Services inflation has slowed, but remains elevated versus history.

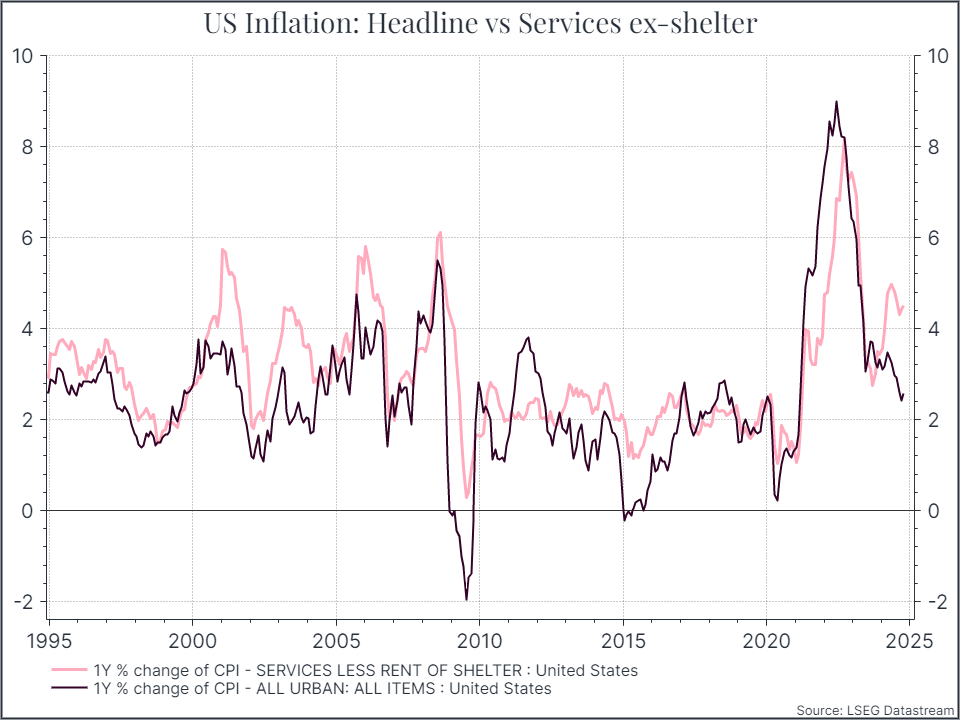

We can see a similar picture in the US, where annual services inflation (excluding shelter) has actually accelerated over the past few months.

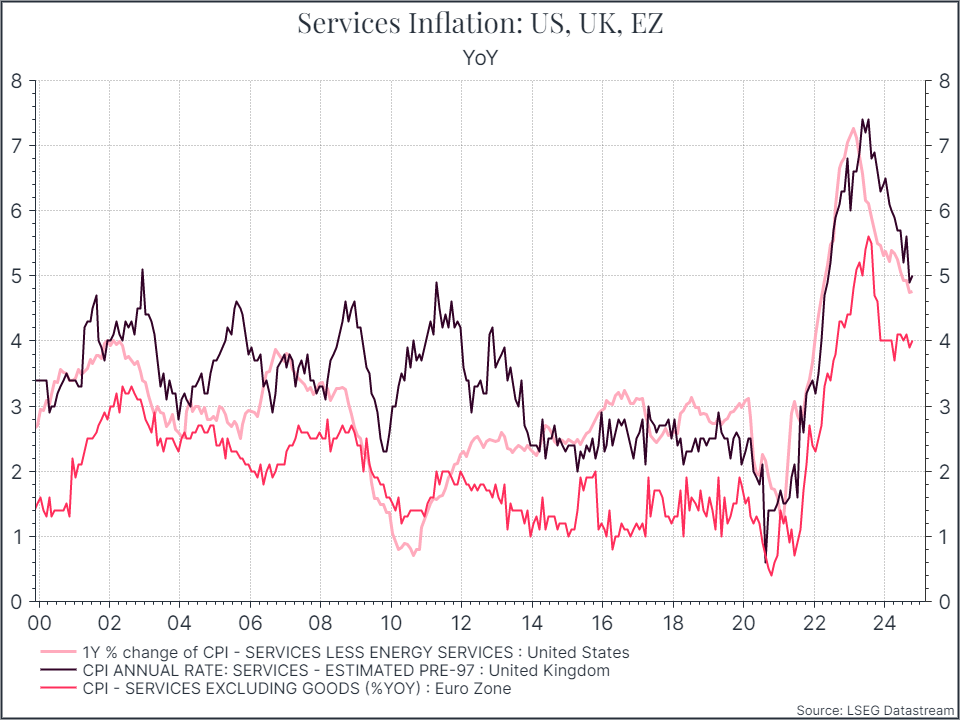

Services inflation in the UK, US and EU (see chart below) remains elevated and it’s likely something that will be a focus for policymakers in the coming months.

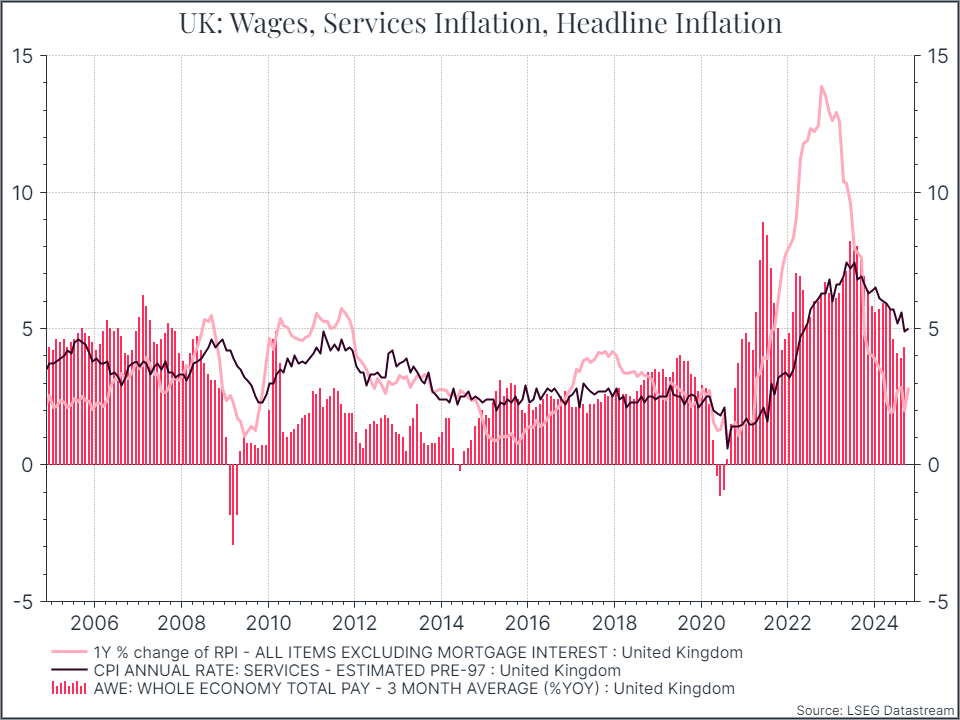

Services inflation is quite closely linked to the labour market. The chart below shows UK wage growth compared to services and headline inflation. We can see that wage growth and services inflation have stayed high when compared to headline inflation. Even if labour markets in the US and the UK are slowing, they remain fairly tight, with low levels of unemployment and labour shortages in certain sectors. Wage growth remains higher than Central Bankers would probably like.

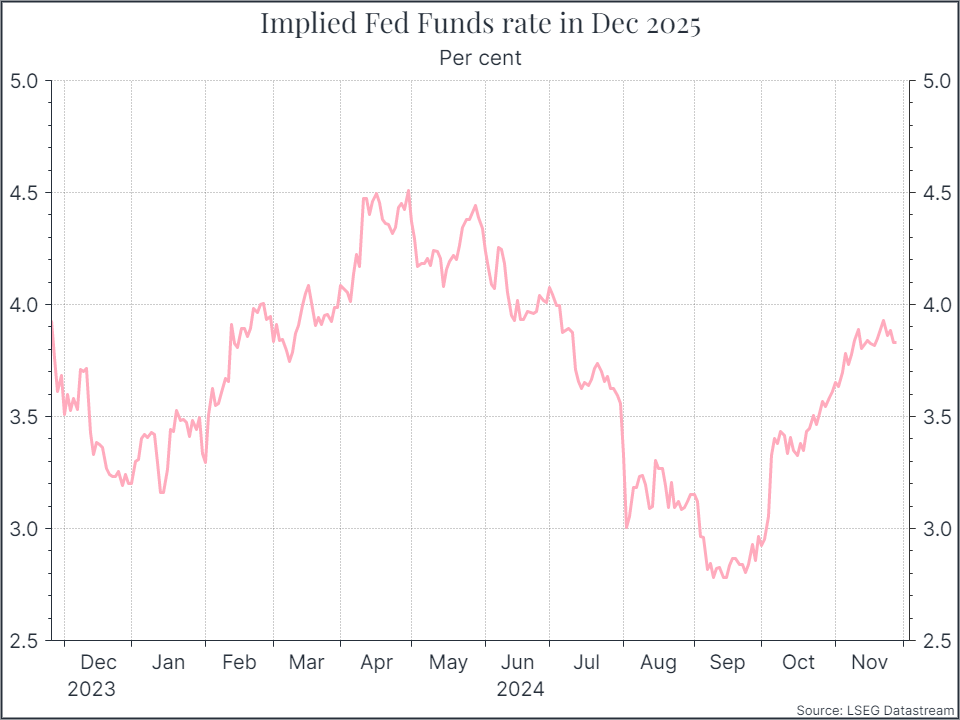

Elevated services inflation has implications for monetary policy. In the minutes of its latest meeting, for instance, the US central bankers stressed a gradual approach to lowering interest rates, reflecting uncertainty over the inflation outlook. And investors have significantly recalibrated their expectations for policy rates in the US. The chart below shows one market-based forecast of the US policy rate at the end of 2025. Expectations for the December 2025 Fed funds rate have shifted quite sharply over the past couple of months, as US macro data has remained resilient. Now, financial markets are pricing in only two or three rate cuts in 2025 – far fewer than was expected a couple of months ago.

We think all that reflects concerns that inflation could accelerate fairly quickly in the wake of lower policy rates. Services inflation remains elevated and we think that higher tariffs around the world could translate into higher prices for imported goods. To some extent, investors have begun to price in that scenario – at least based on expectations for fewer rate cuts – but it still leaves us a bit wary of adding to long duration bonds. We might be living with higher interest rates for some time to come.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.