Richard Flax, Chief Investment Officer, Moneyfarm

Pessimism usually sounds clever. There are all the risks, the problems, the unforeseen dangers to foresee. All the reasons why it can’t be done and won’t happen. But sounding pessimistic (and wise) about financial markets is relatively easy. Perhaps the more interesting question is why 2019 could do better than people think.

Understanding the uncertain backdrop

Looking for opportunities in 2019 doesn’t mean disregarding the uncertain backdrop. There are important dynamics at play that our portfolio managers are monitoring daily. These are:

- Global growth – More specifically weakness in Europe and China, and indications of weaker sentiment in the US

- Trade disputes – Trade tariffs are on the rise, which doesn’t historically bode well for global growth, or exporters

- Domestic politics – There’s the US government shutdown, Brexit, conflict between the Italian government and the EU, tensions within France, and the continuing rise of populism

- Geopolitics – Think US-Russia, US-China, US-NATO, Intra-EU disagreements, populism and social unrest

- Policy mix – There’s an significant bias towards tighter monetary policy and deteriorating fiscal policy – notably in the US

- Unrealistic expectations – Earnings expectations are being revised down

Opportunities in financial markets

In the optimist’s world, expectations are everything. Financial markets are adaptive and forward-looking – at least to some extent – and the list above is hardly unknown.

Most of these issues, by definition, must be reflected in financial asset prices at least to some extent. That matters because you don’t need to solve them for financial asset prices to go up (at least in the short-term). Over a twelve-month time frame, you may only need to see signs of improvement to get a positive response from financial markets.

If that’s the case, let’s consider where we could see improvements, rather than solutions.

- Growth stabilises

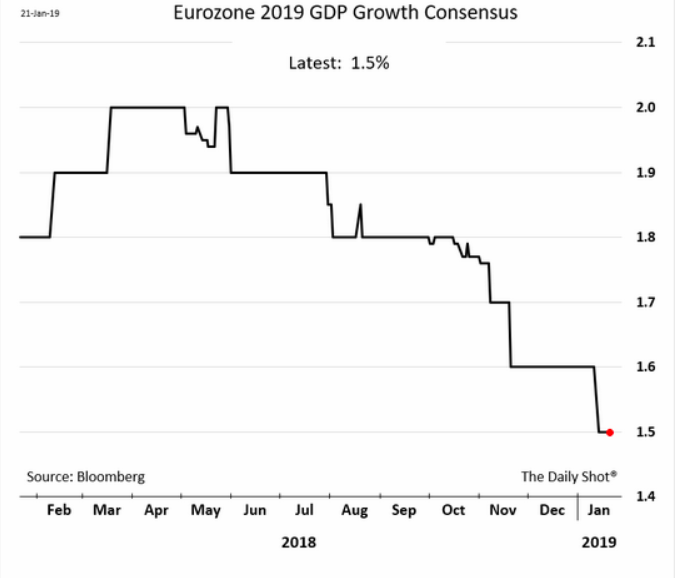

This logic applies to earnings and GDP growth. Expectations have been coming down steadily. For sake of completeness, here’s a chart reflecting expected GDP growth and expected earnings.

Given the direction of travel – the optimist would argue that you don’t need to see a recovery, you just need to see expectations stabilise. That in itself could be enough to pro mpt a recovery.

mpt a recovery.

- Politics

Another broad headline. This is a thorny one, partly because getting deep into discussions about social contracts isn’t always helpful for thinking about expected returns (but it is sometimes!).

If we think about trade, for instance, it’s an issue that has been rumbling along for two years and has begun to impact reported GDP growth. At this point, we’d argue that progress (and it will never be a complete solution) would improve expectations for risky assets.

And with economies slowing, in China and elsewhere, the pressure is increasing to try to re-accelerate growth.

Similarly, in domestic politics, you probably should believe that at some point the US shutdown will end (or at least be fully in the price), there’ll be some conclusion on Brexit – for better or worse. At least these uncertainties will become marginally clearer, which will likely be taken well by markets after navigating the unknown.

- Policy mix

Here we’ve already seen the impact of potential changes. The commentary from the US Fed on further rate hikes – hawkish in December, dovish in January – has already moved markets.

With expectations for growth and inflation falling, Central Banks can probably stay more supportive than had been expected six months ago.

Where does that leave us?

It’s not a rosy picture, but it’s certainly not bad. It’s really all about growth. If we see expectations stabilise for growth and earnings – and they should eventually – and get some clarity on politics, that could be enough to generate some decent returns, especially given the de-rating of equity valuations.

These aren’t heroic assumptions to make, but they are not guaranteed either.

Sadly, it’s tough to see progress on some issues in the short-term. The likely state of the US budget deficit is going to require tougher decisions than “does that wall come in steel or concrete”.

And it’s also tough to believe that any trade deal, no matter how beautiful, will deal easily with the great power politics of China and the US.

But, for the next twelve months at least, a bit of stability around growth expectations and some sort of political relief could be enough to boost risky assets.

We will soon be communicating our Strategic Investment Outlook for the next 10 years. If you have any questions about how your portfolio is prepared for Brexit, please book a call with your Investment Consultant, who will be happy to talk it through or conduct a free review of the investments you hold outside of Moneyfarm.