For anyone looking to put their money to work, the decision between whether to allocate funds to a cash ISA or a stocks and shares ISA is a vital one. These are two of the most popular types of ISAs available, and depending on your personal circumstances, both have their merits.

It pays to be as informed as possible when planning for your secure financial future. Below, we explore the differences, the risks, and the potential returns of each to help you choose the best one for your needs.

Quick Comparison: Cash vs Investment ISAs

Before diving deep into the data, here is the high-level breakdown of why investors choose one over the other:

Top 3 reasons to choose a Cash ISA

- Security: Your capital is generally safe from market fluctuations.

- Short-term goals: Ideal for money needed within the next 1-3 years.

- Predictability: You often know the interest rate in advance.

Top 3 reasons to choose a Stocks and Shares ISA

- Potential for higher returns: Historically outperforms cash over the long term.

- Beating inflation: Gives your wealth a better chance to grow in real terms.

- Compound growth: Returns on your returns can snowball over time.

Who is the winner? Often, it is both. You can hold both types to create a diversified strategy.

Cash ISA vs Stocks and Shares ISA: The Performance Data

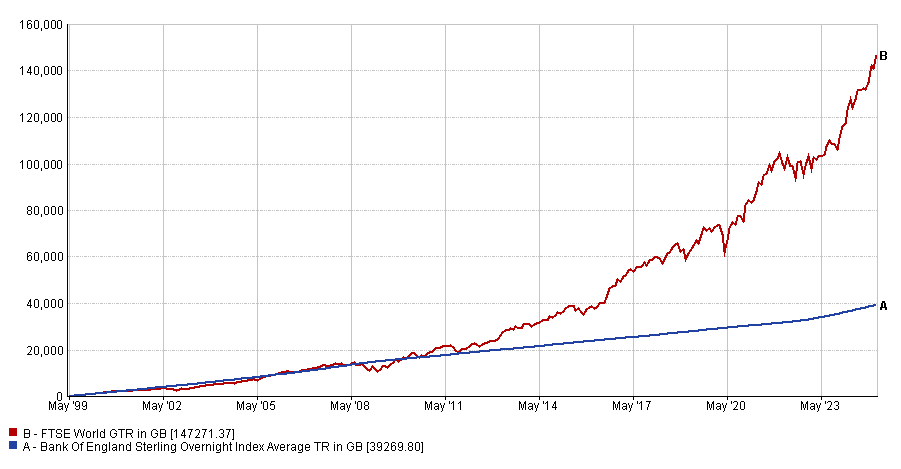

When making this decision, it helps to look at the numbers. Moneyfarm recently analysed the performance of saving versus investing over the last 25 years (from the ISA’s inception in April 1999 to January 2025).

In this simulation, we compared a monthly contribution of £100 into a Cash ISA (using the SONIA interest rate benchmark) versus a Stocks and Shares ISA (using the FTSE All-World index).

The Simulation Results (1999–2025)

- Total Contributed: £31,100

- Cash ISA Value: £39,268.80

- Stocks & Shares ISA Value: £147,271.37

While the Cash ISA provided steady growth, the investment portfolio significantly outperformed it, generating a pot nearly four times larger over the 25-year period. This highlights the power of compound growth in the stock market over long horizons.

Source: Moneyfarm Analysis, Data Source: FE Fund Info.

Note: Past performance is not a reliable indicator of future returns. The value of investments can go down as well as up.

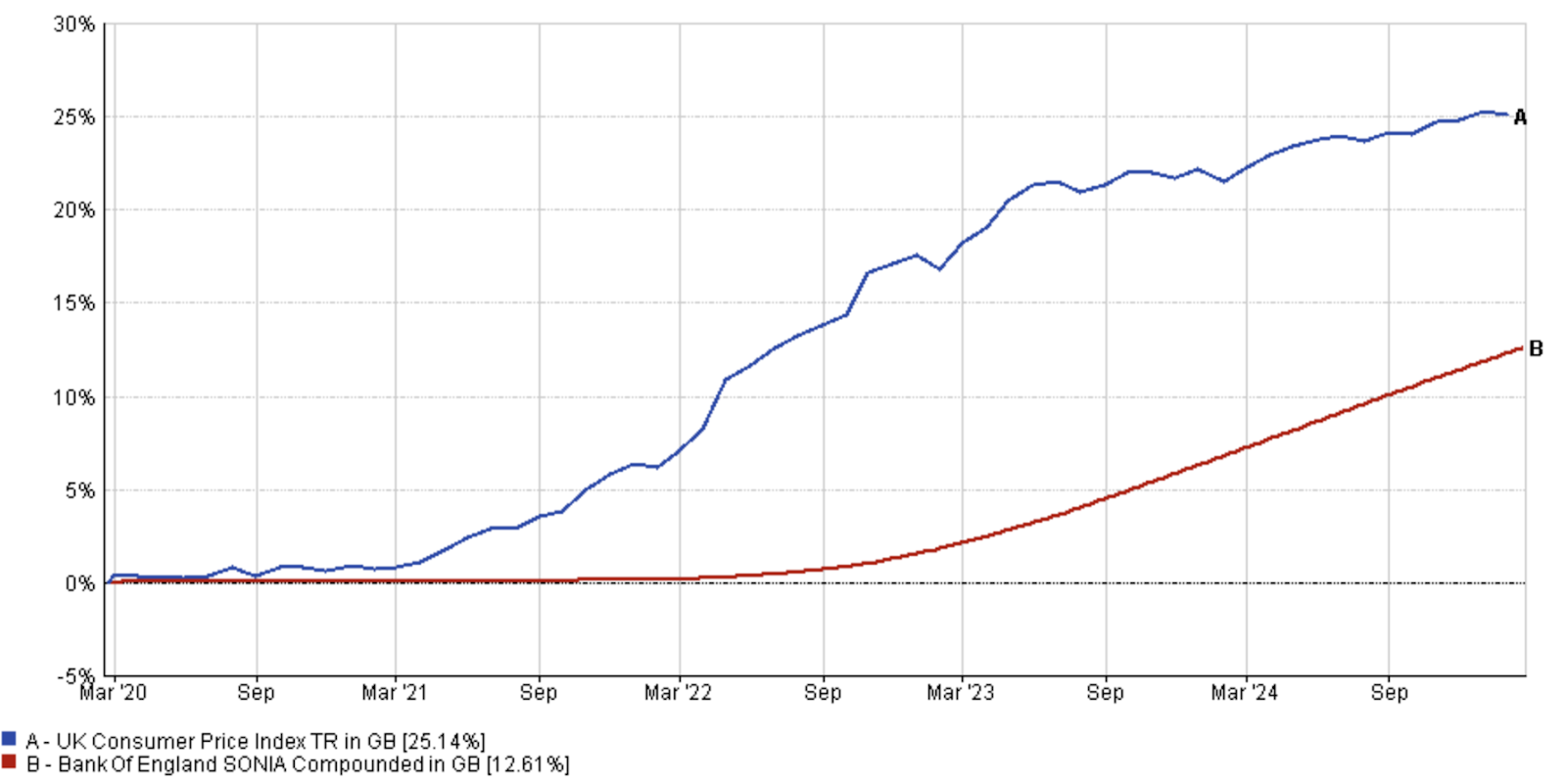

The Impact of Inflation

One critical factor often overlooked is inflation. In the last five years alone (since 2020), the UK Consumer Price Index (CPI) has risen by approximately 25%, whereas cash savings rates (based on SONIA) returned only 12%. This means that money kept solely in cash during high-inflation periods has actually lost “real” purchasing power.

Deep Dive: Cash ISAs

Cash ISAs are, ultimately, predictable. They function like standard savings accounts but with a tax-efficient wrapper. They are traditionally viewed as a safe deposit box to protect savings from market volatility.

Key benefits include:

- Tax-free Status: Interest earned is free from income tax.

- Safety: Up to £85,000 per person per financial institution is protected by the Financial Services Compensation Scheme (FSCS).

- Liquidity: Easy-access Cash ISAs allow you to withdraw funds whenever needed (though fixed-rate bonds may have restrictions).

- Risk-Free Capital: The nominal value of your money does not drop due to stock market movements.

However, the main risk with cash is inflation risk. If the interest rate you earn is lower than the rate of inflation, your money buys less over time.

Deep Dive: Stocks and Shares ISAs

By contrast, a stocks and shares ISA allows you to invest in equities, bonds, and other assets. While this introduces volatility—meaning your account value will fluctuate daily—it offers the potential for significant growth over the medium to long term.

Key benefits include:

- Tax Efficiency: No capital gains tax or dividend tax on returns.

- Better Returns: As shown in the simulation above, equities have historically outperformed cash over long periods (5+ years).

- Diversification: Funds are spread across different companies and regions, minimising the risk associated with a single company failing.

- Long-term Goals: Ideal for retirement planning or saving for a child’s future (such as via a Junior ISA).

(Moneyfarm Analysis, Data Source: FE Fund Info)

Key Differences at a Glance

| Feature | Cash ISA | Stocks & Shares ISA |

|---|---|---|

| Best for | Short-term goals (< 5 years) | Long-term goals (> 5 years) |

| Risk Level | Low (Capital is secure) | Medium to High (Capital fluctuates) |

| Inflation Risk | High (May not beat inflation) | Lower (Better chance to beat inflation) |

| Tax Benefits | Tax-free interest | Tax-free capital gains & dividends |

| Allowance | £20,000 per tax year | £20,000 per tax year |

Combining Both: Why Diversification is Important

You do not have to choose just one. Under current UK rules, you can contribute to multiple types of ISAs in the same tax year, provided you do not exceed the combined £20,000 annual allowance.

A balanced strategy might look like this:

- Short-Term Security: Keep 3–6 months of expenses in a Cash ISA as an emergency fund. This ensures you have liquidity for unexpected bills without having to sell investments at a bad time.

- Long-Term Growth: Invest the remainder of your allowance in a Stocks and Shares ISA to build wealth for the future, beating inflation and benefiting from compound interest.

For example, if you are saving for a holiday next year, cash is the prudent choice. If you are saving for retirement in 20 years, the stock market offers far greater potential.

Should I choose a Cash ISA or a Stocks and Shares ISA?

To make the right choice, consider your timeline and risk tolerance.

- Choose Cash if you need the money soon (within 5 years) or cannot sleep at night worrying about market drops.

- Choose Stocks and Shares if you can leave the money untouched for 5+ years and want to grow your wealth significantly above inflation.

Moneyfarm’s strategy is to combine the right mix of assets with the appropriate level of risk for each individual customer. We update portfolios regularly to ensure customers get the most out of their investments, backed by low fees and dedicated advice.

FAQ

Yes. You can hold both types of accounts simultaneously and pay into both during the same tax year, as long as your total contributions do not exceed the £20,000 allowance.

Historically, they perform well over the long term. For instance, data shows that over the last 25 years, a global equity portfolio would have significantly outperformed a cash savings account. However, performance fluctuates year-on-year.

Yes, if you have mid to long-term financial goals, then stocks and shares ISAs are worth it, especially if you want tax benefits and a higher rate of return.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.