The government is preparing to balance the books in the upcoming Autumn Budget on November 26. It has been widely reported that there is a £30–50 billion black hole in the country’s finances and speculation is mounting about how the Treasury plans to raise this cash.

Part of the difficulty of this year’s Budget stems from the Chancellor’s self-imposed “non-negotiable” fiscal rules. These rules dictate that by the end of the parliamentary term, national debt must be falling as a share of the economy. They also require day-to-day government spending to be balanced, meaning it must be paid for by tax income rather than borrowing.

Where are we now?

The last Budget saw a swathe of tax and spending changes, pitched as a one-off reset for the public finances. However, a challenging period of heightened market volatility, slow growth, high national debt, and an increased cost of government borrowing means that tough decisions are once again on the horizon.

So what are the taxes that are landing on the minister’s desk this time around? The government has promised not to raise the headline rates of National Insurance, income tax or VAT on working people. However, recent comments by Reeves that “the world has changed”, have made this commitment unclear.

The Government has also been very cautious about a wealth tax, reportedly worried that it would push the wealthiest contributors to relocate.

Against this backdrop, one area that is speculated to come under the microscope is pensions.

Navigating pension tax rumours

While these are not from official government sources, the following are ideas floated by think tanks and news outlets regarding potential changes to pension rules and tax.

Restrictions to salary sacrifice options

Some employers allow you to sacrifice a portion of your salary for another benefit – primarily a pension contribution. Because the money is paid directly into your pension, neither the employee nor the employer pays National Insurance Contributions (NICs) on that amount.

If the government were to remove this national insurance relief, it could reduce the incentive to offer such schemes. The Institute for Fiscal Studies (IFS) claims that introducing employer NICs on these contributions at the full rate of 13.8% could raise £17 billion

Capping tax relief

Currently, eligible personal pension contributions receive tax relief as a 20% top-up from the government automatically. Higher and additional rate taxpayers can then claim further relief through their self-assessments to bring their total relief to 40% or 45%. The annual allowance for tax relieved contributions is the lower of your relevant UK earnings (usually your salary) or £60,000, and you may be able to carry forward unused allowance from the previous three years.

There is speculation that the amount of tax relief could be capped at a flat rate, for instance at 30% or even 20%. This would significantly dampen the incentive to higher earners to save into a pension. Doing so could lend to a £15 billion saving, according to the IFS.

Reducing the tax-free cash amount

When you access your defined contribution (DC) pension (from age 55, rising to 57 in 2028), you can currently withdraw 25% of your pot completely tax-free, up to the Lump Sum Allowance (LSA) of £268,275. When the full amount of tax-free cash is taken one go, this is also known as the Pension Commencement Lump Sum (PCLS). It has been rumoured that this key perk could be reduced.

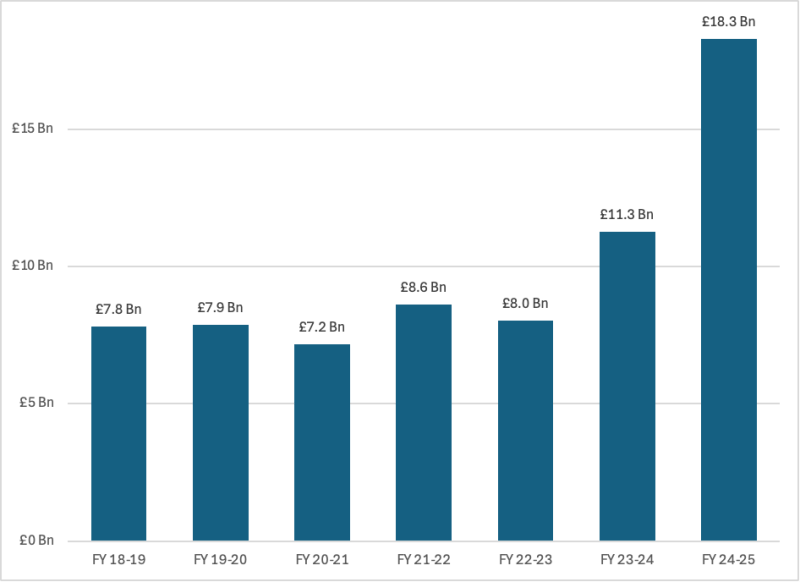

Similar fears ahead of the last budget led to a record number of early pension withdrawals. According to the Financial Conduct Authority (FCA), in the last financial year there was a 63% increase in the taking of tax-free lump sums on the previous year, and more people accessed their pensions for the first time than ever before.

Taking of tax-free lump sums: Total value withdrawn via PCLS

How realistic are pension tax changes?

Official statistics estimate that up to 43% of the population aren’t saving enough for retirement, which presents a significant future burden on the state. The government has been working to improve pension saving and retirement outcomes for the UK’s ageing population, and making pensions less attractive to investors would undermine these efforts.

Any such moves would be highly unpopular with diligent savers, too, who have thought about their long-term retirement plans, and the government would need to consider the political and practical implications very carefully.

It is also difficult to see how major structural changes could come into effect overnight, as they would require a significant overhaul across thousands of providers and HMRC systems. It is more likely that if significant changes like those rumoured were to be announced, they’d be done so well in advance to give the industry and the public time to prepare. This is similar to the Inheritance Tax changes announced in last year’s Budget, which won’t take effect until April 2027. We addressed these concerns ahead of that Budget here.

A case against knee-jerk decisions on tax-free cash

Before making any hasty decisions, it’s important to note that taking tax-free cash early is an irreversible decision. You move funds from a tax-efficient environment (your pension) to one that may not be, potentially missing out on years of valuable, tax-free growth. As Money Helper, the government-backed guidance service, advises, “taking money from your pension is not a decision to rush into”.

If taking tax-free cash now is not part of your long-term financial plan, it’s crucial to consider the potential impact.

Take Stan, who is 55 and has a pension worth £400,000. He assumes his investments will generate 7% annualised growth and plans to use his tax-free cash to help purchase a property/pay off his mortgage in 10 years. Worried by rumours that the 25% tax-free cash element might be reduced, he considers two options: take his PCLS (25% tax-free cash) today and invest the proceeds in a General Investment Account (GIA), or stick to his plan and take his PCLS in 10 years.

For this example, we are assuming that there are no changes to tax-free cash rules in the Budget.

Option 1: Take PCLS today and invest in GIA

Stan takes £100,000 tax-free from his pension, leaving £300,000 invested. The £100,000 is invested in a GIA.

After 10 years, his remaining pension pot is worth: £590,145.

His GIA is worth £196,715.

To buy the property, he sells his GIA.

After paying Capital Gains Tax (CGT), he is left with £174,224.

Option 2: Take PCLS in 10 years

Stan leaves his full pension invested.

To buy the property, he takes his 25% PCLS, giving him £196,715.

After 10 years, his pension is worth £786,861.

Outcome

By sticking to his long-term plan, Stan has £22,492 more to put towards the property, without needing to touch the remaining taxable part of his pension. This simplified example shows how acting on speculation could lead to a less favourable outcome due to factors like losing tax-free growth and incurring CGT if the changes did not take effect.

The case study assumes 7% annualised growth; for the GIA, a 24% Capital Gains Tax rate is applied after using a £3,000 annual exemption, and it does not account for more complex strategies such as CGT harvesting or Bed & ISA.

This is for illustrative purposes only and does not constitute advice.

What else is on the table?

Outside of pensions, there are numerous other rumours that have been swirling. These include potential changes to:

- ISA limits: Lowering the annual Cash ISA allowance to shift focus from saving to investing

- Capital Gains Tax: Increasing rates again from their current levels

- Inheritance Tax: Introducing tighter rules on lifetime gifts

- Property Taxes: Reforms to Council Tax banding, Stamp Duty Land Tax (SDLT), or even introducing CGT on primary residences

- Freezing thresholds: Continuing to freeze income tax and other thresholds to pull more people into higher tax brackets over time through ‘fiscal drag’

It’s important to view this speculation in a wider context. The Chancellor faces the classic challenge of raising revenue without damaging the economy. While higher taxes are needed to address the deficit, they can act as a headwind to investment required for growth.

Cut through the noise

As always, it’s important to remember that these are just rumours and speculation. The media often present such possibilities in ways that can pressure individuals into making hasty financial decisions, potentially undermining sound long-term plans.

Knee-jerk reactions in the short term based on speculation can have unintended consequences later on. The most effective strategy is to stick to your long-term financial plan.

Our team of Wealth Managers is staying up to date on all Budget developments and is available to help you cut through the noise.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.