Now that the dust has settled – at least a little – on the first Labour Budget in fourteen years, we want to take stock of where we are.

But before that, it’s worth pointing out that there’s increasingly a dual focus on Budget announcements. First, there’s the actual Budget. Second, there’s the extensive analysis provided by the independent Office of Budgetary Responsibility (OBR). The OBR was set up in 2010 to provide “independent and authoritative analysis of the UK’s public finances”. But the OBR does work together with government departments during the forecasting process and has access to far more information than an independent private commentator. The OBR’s analysis probably gets as much attention these days as the Budget itself, so we should be paying close attention to both.

Turning to the Budget, there are a few headline points to make. Inevitably, everyone heard slightly different messages from the Prime Minister and the Chancellor. We think we’ve heard basically two things. First, public services are not delivering what the UK public expects – be it healthcare, justice, defence – and those services need more resources. That requires higher taxes. Second, the best way to ensure that public services do deliver over time is for the economy to grow fast enough to provide greater prosperity for all and sufficient resources for public services.

In terms of tax revenues, this chart from the OBR illustrates the point on taxes. Taxes as a percentage of GDP have risen steadily over the past few years and are expected to rise even further – to the highest level in the post-World War II period. The UK is far from the only developed economy showing that type of trajectory and its tax take will still be below that of the European Union average.

The second point is around growth. The general view is that, overall, the UK doesn’t spend enough on investment (including things like infrastructure). Investment as a percentage of GDP is lower than many peers and that’s often seen as a constraint on the potential growth that the economy can achieve. Some of that reflects weak government investment and the Budget made an attempt to address that.

But the chart below shows that the impact overall is expected to be quite muted. This chart shows the OBR’s forecast of how the Budget would impact economic growth. We can see a bit of a jump in the next couple of years – thanks to greater government spending. But as we go further out, the impact becomes more muted and eventually even negative. The point here is that the OBR reckons that the Budget is simply shifting resources from the private sector to the public sector without really increasing the overall pie.

So where does that leave us? It seems tough to argue that public services in the UK are delivering for its citizens. It also seems reasonable to suggest that faster growth is one of the best ways of improving the situation in the long term. But this Budget highlights the challenges – hiking taxes and expecting faster growth seems a bit counter-intuitive. The government will argue, perhaps fairly, that it’ll take time to see the benefits of better public services and increased government investment to feed into the broader economy. But the OBR’s forecasts suggest either that this Budget won’t be sufficient (particularly given the assumption of very low spending growth in the later years of the forecast) or that it’ll take more than five years to start to see the benefit.

What does it mean for portfolios? If you’re lending to the UK government (i.e. buying government bonds), it’s a bit of a mixed bag – as it is for most developed market governments.

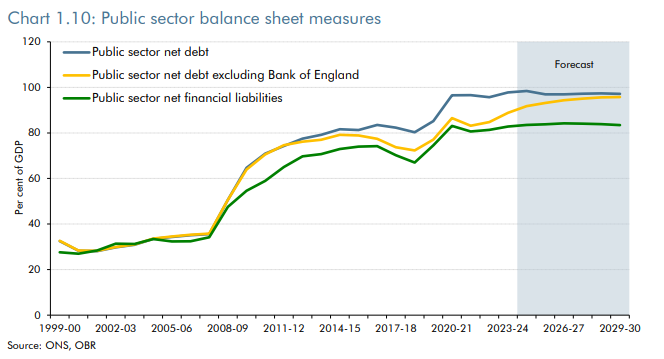

The good news is that the government is focused on fiscal sustainability – mindful of the Truss experience. And the forecasts suggest that government debt to GDP should be stable over the next few years (see chart above). That’s a decent start and we think it helps make the yield on UK government debt look interesting at this point. But the Chancellor is right to emphasise growth as a way to improve overall prosperity and improve its own fiscal metrics. And by that measure, the forecasts suggest that there’s still much more to do.

*As with all investing, financial instruments involve inherent risks, including loss of capital, market fluctuations and liquidity risk. Past performance is no guarantee of future results. It is important to consider your risk tolerance and investment objectives before proceeding.